Equable Institute has issued Retirement Security Policy Scorecards for Oklahoma House Bill 3313 (HB3313).

The proposed bill would impact the retirement benefits of Oklahoma PERS Hazardous and Oklahoma PERS Non-Hazardous members as follows:

- Modify the Pathfinder defined contribution plan by enhancing benefits effective November 1, 2026

- Increase mandatory employee contributions by 0.5%, from 4.5% to 5.0%

- Increase required employer contributions by 1.0%, from 6.0% to 7.0%

- Allow members to vest in their benefit immediately

- Change the default benefit payout to a lifetime income annuity

Equable Institute’s Assessment of Oklahoma House Bill 3313

Equable’s assessment finds that the changes to the Pathfinder defined contribution plan proposed in HB3313 would offer moderately better retirement benefits than those currently available to Oklahoma PERS Hazardous and Non-Hazardous members.

The proposed changes to the existing Pathfinder defined contribution plan, offered to new hires for Oklahoma PERS since 2015, increases the required employee contributions by 0.5%, increases required employer contributions by 1.0%, removes the vesting requirements for the employer contributions to members’ individual retirement accounts, clarifies and formalizes the set of investment options offered to participants, and establishes a lifetime income annuity as the default distribution option.

According to the assessment, HB3313 would provide moderately more valuable benefits for each of the following different groups of workers.

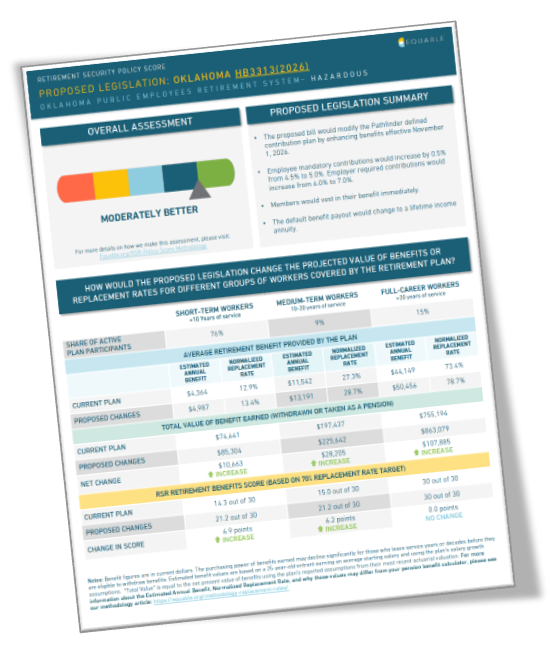

OK PERS Hazardous

- Full-career workers (those with more than 20 years of service): These employees, who make up 15% of active plan participants in Oklahoma PERS, would see their lifetime benefits increase by more than $107,000.

- Medium-term workers (those with 10-20 years of service): These employees account for 9% of active plan participants and would see their lifetime benefits grow by over $28,000.

- Short-term workers (those with less than 10 years of service): These employees make up the vast majority (76%) of active plan participants and would see their lifetime benefits jump by over $10,000.

For more details, view our Equable Retirement Security Policy Scorecard (Hazardous):

DOWNLOAD THE OK PERS – HAZARDOUS SCORECARD

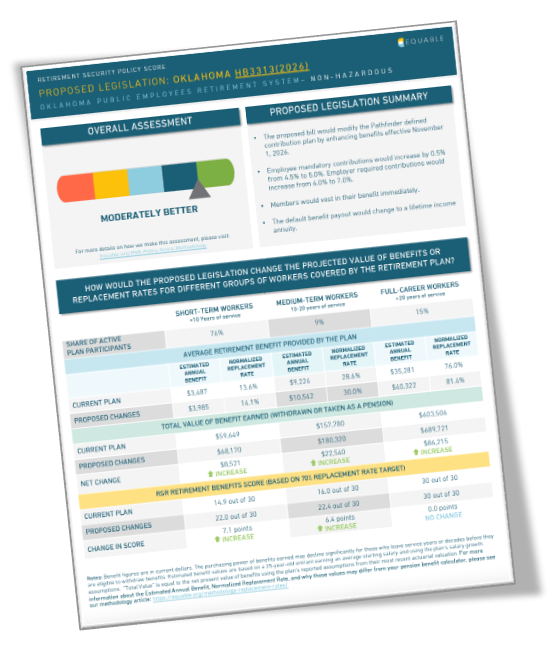

OK PERS Non-Hazardous

- Full-career workers: These employees would see their lifetime benefits increase by more than $86,000.

- Medium-term workers: These employees would see their lifetime benefits grow by over $22,000.

- Short-term workers: These employees would see their lifetime benefits jump by over $8,000.

For more details, view our Equable Retirement Security Policy Scorecard (Non-Hazardous):

DOWNLOAD THE OK PERS – NON-HAZARDOUS SCORECARD

Equable Institute’s Analysis of Oklahoma House Bill 3313

Like all retirement reforms, the changes proposed in HB3313 offer a series of trade-offs that should be taken into consideration.

Positive Elements

-

The increase in required contributions for both employers and employees will increase the total amount of funds being set aside for retirement, increasing account balances and putting plan members on a more secure path to retirement.

-

Members under the proposed changes would immediately vest in employer contributions to their Pathfinder accounts, meaning that all contributions to their retirement accounts are portable should they want or need to leave OK PERS covered employment.

-

Under the proposed bill, the OK PERS Board of Trustees is required to offer a formal set of investment options for members, including both predetermined portfolio options and diversified investment choices. This will increase flexibility and optionality for those members that seek to direct their retirement investments while also maintaining a set of solid defaults for those that do not wish to be involved in the specifics of how their retirements are invested.

-

The default benefit distribution would change to a lifetime income annuity, but members would still have the option to elect for a lump sum payout. This change to the benefit payout would provide members with a guaranteed income option that also removes the worries that they will outlive their savings. By retaining the option for members to take other types of benefit distribution, it ensures that all members can receive their benefits in the way that is best for them.

Negative Elements

- Increasing member and employer contributions comes with a cost. For members, the 0.5% increase might not be that much, but it does mean more of their paychecks will go to costs outside of their control.

- Immediate vesting, while a best practice for defined contribution plans, removes one more barrier from a member deciding to leave their position and the plan. While the more generous benefits are a net positive, by removing all barriers to a member’s benefits, the incentives to stay are slightly lessened.

- By offering multiple choice options, namely the investment options and lifetime income annuity benefit distribution, members may be presented with too many complex financial decisions. This places a larger burden on the plan to ensure default options are those that will best serve their members. There is also an increased need for financial education for members to make informed decisions regarding their available options.