Guaranteed lifetime income is the big promise that comes with having a pension plan.

But how much can you expect to actually receive? Uniquely, states calculate post-retirement income via a pension formula.

What is the Formula to Calculate a Pension?

The formal name for a pension plan is a final average salary defined benefit plan. In that context, the thing being “defined” in a defined benefit pension plan is the formula that’s used to determine your future retirement income.

The pension formula is based on your working years — both how long you serve and what you earn.

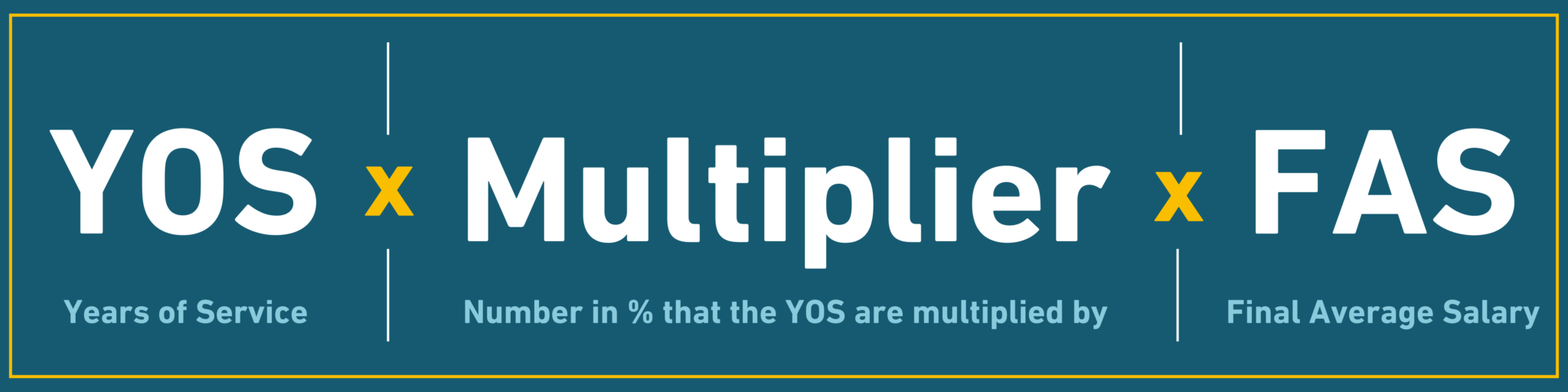

As illustrated above, there are three key concepts that are important for calculating the value of your pension.

- Years of Service (YOS): This is how many qualifying years you’ve worked for your employer within the pension plan.

- Multiplier: This is a percentage number that states have predetermined in statutes and can vary by state and hire date. You multiply this percentage against your years of service to create larger pension benefit values. Other names used for the multiplier are accrual rate or crediting rate, but they mean the same thing.

- Final Average Salary (FAS): This is the compensation that your pension is based on. For most state and local pension plans, the final average salary is based on the last three or five years of work. Some states use the three or five highest years of salary. This is also known as final average compensation, final average pay, or even highest average salary.

Pension plans calculate years of service and what determines final average pay using different rules. Those rules can make a big difference in how much a pension is worth.

Notably, the contributions paid by pension plan members do not factor into the value or their pension. The money contributed by employers and pension plan members matters for building up assets that can pay promised benefits, but the benefit amount paid is only based on the pension formula.

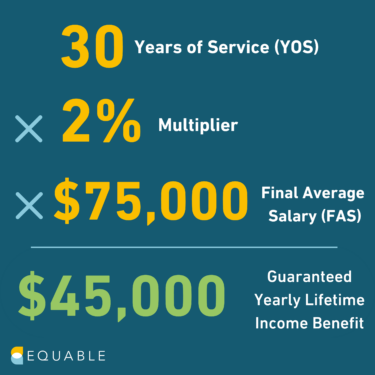

Example: Calculating Your Pension Benefit

To calculate your pension benefit, multiply your years of service the multiplier in the formula. The product is known as your “replacement rate,” or the percentage of your final average salary you receive in retirement. The higher the multiplier, the larger the benefit.

Then, multiple this specific number by your final average salary. The product of this equation is the amount you’ll ultimately receive as a guaranteed yearly lifetime income benefit when you retire.

In the example above, an equation with 30 years of service, a 2% multiplier, and a $75,000 final average salary produces a $45,000 guaranteed yearly lifetime income benefit.

In this example, the result of 30 years of service is a pension that is worth 60% of the final average salary (30 years ✕ 2% multiplier = 60% replacement rate).

Calculate Your Pension

Below is a pension calculator that can help to estimate the value of your future pension, taking into account various factors and scenarios.

There are hundreds of public pension plans, and we are gradually adding to the list of those in this calculator. If you do not see your pension plan listed here, please contact us, and we’ll be sure to add it quickly and send you notes estimating your pension.

This article was originally published September 28, 2022.