State of Pensions 2021: National Pension Funding Trends

U.S. public pension funding in 2021 experienced strong investment returns in the most recent fiscal year, but the funded ratio for most statewide retirements plans are only back to 2008 levels, a new Equable Institute report on national pension funding trends shows. In this post, we will look at the core reasons behind why pension funds are struggling to get back to pre-Great Recession numbers.

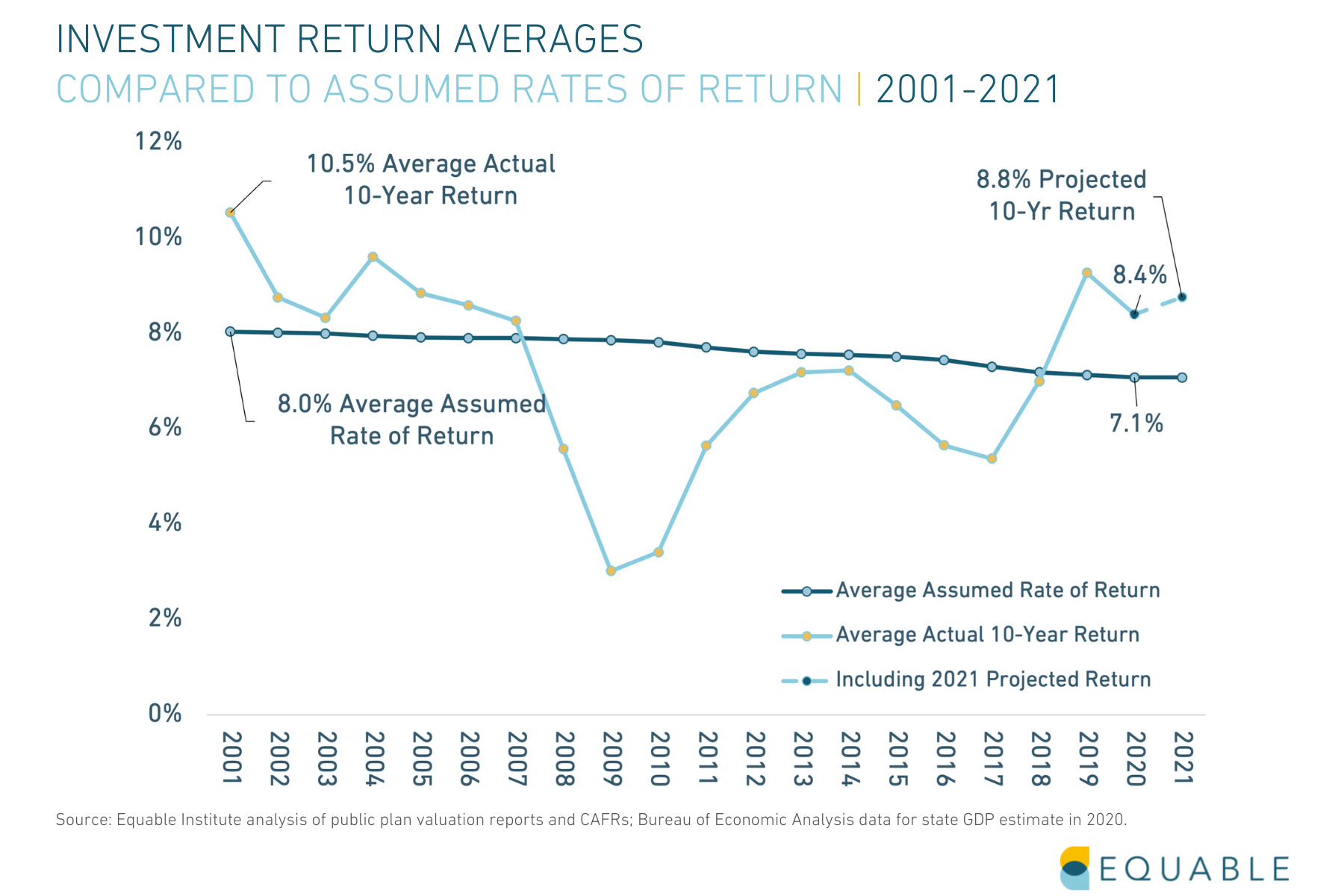

A few strong years over the past decade have helped improve the 10-year average, but for much of the 20th century average returns have been less than assumed — in part because while interest rates fell sharply assumed returns declined only gradually.

As a result, pension fund assets grew less than expected, which was a key reason for the growth in unfunded liabilities up until 2021’s massive year of investment performance.

State of Pensions 2021: Public Pension Debt is Dropping.

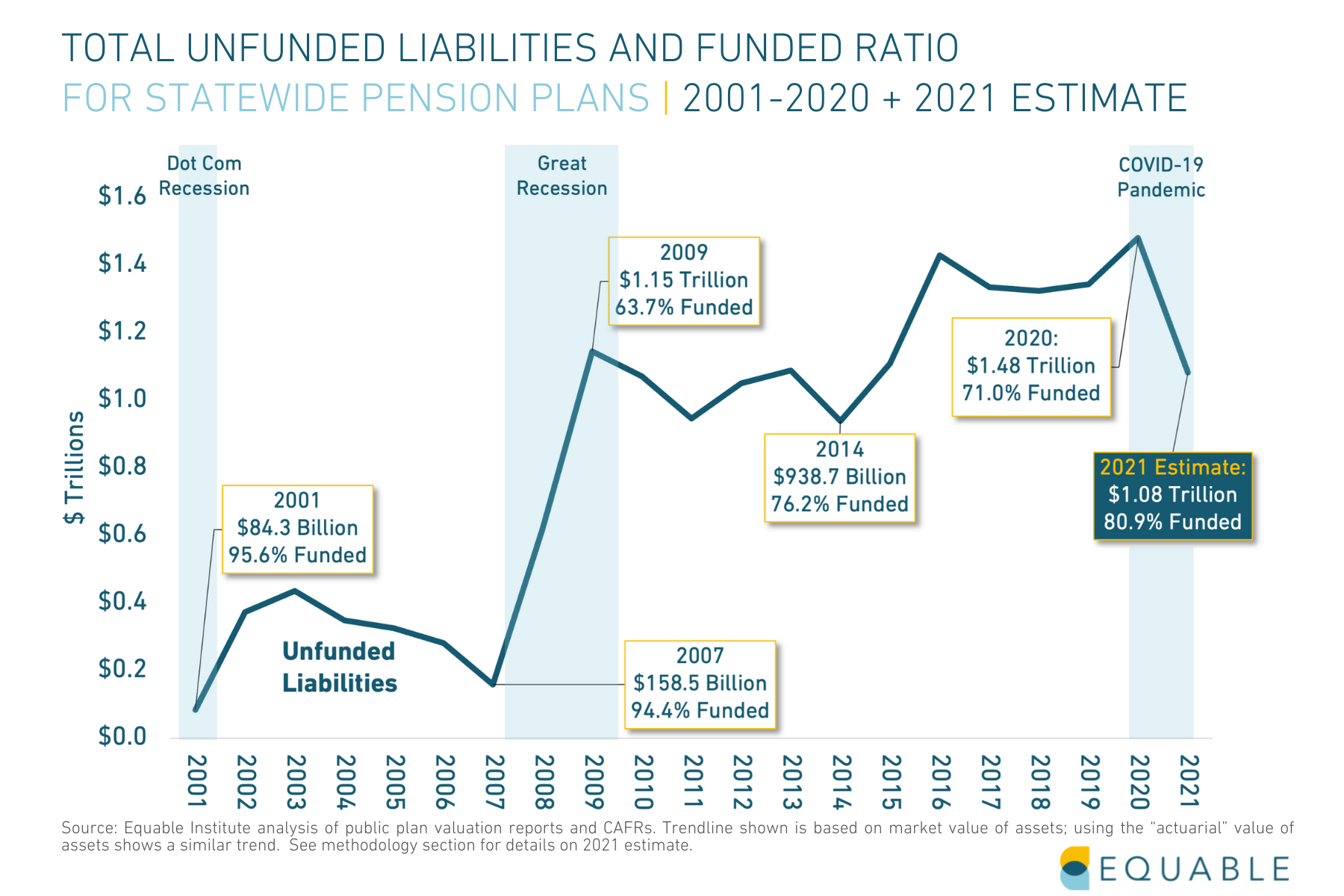

What is the public pension funding gap in 2021?

The national pension funding shortfall (or pension debt) for statewide retirement systems was $1.48 trillion at the end of 2020, per Equable Institute’s State of Pensions 2020 report.

The funding shortfall — formally called unfunded liabilities — is the gap between money held by pension funds and the value of all future benefits it has promised to pay. This is also sometimes called pension debt.

The shortfall was, in part, caused by investment volatility set off by the Covid-19 pandemic. But in the past year investments have been strong, and we think 2021’s those returns will shrink the funding shortfall to $1.08 trillion.

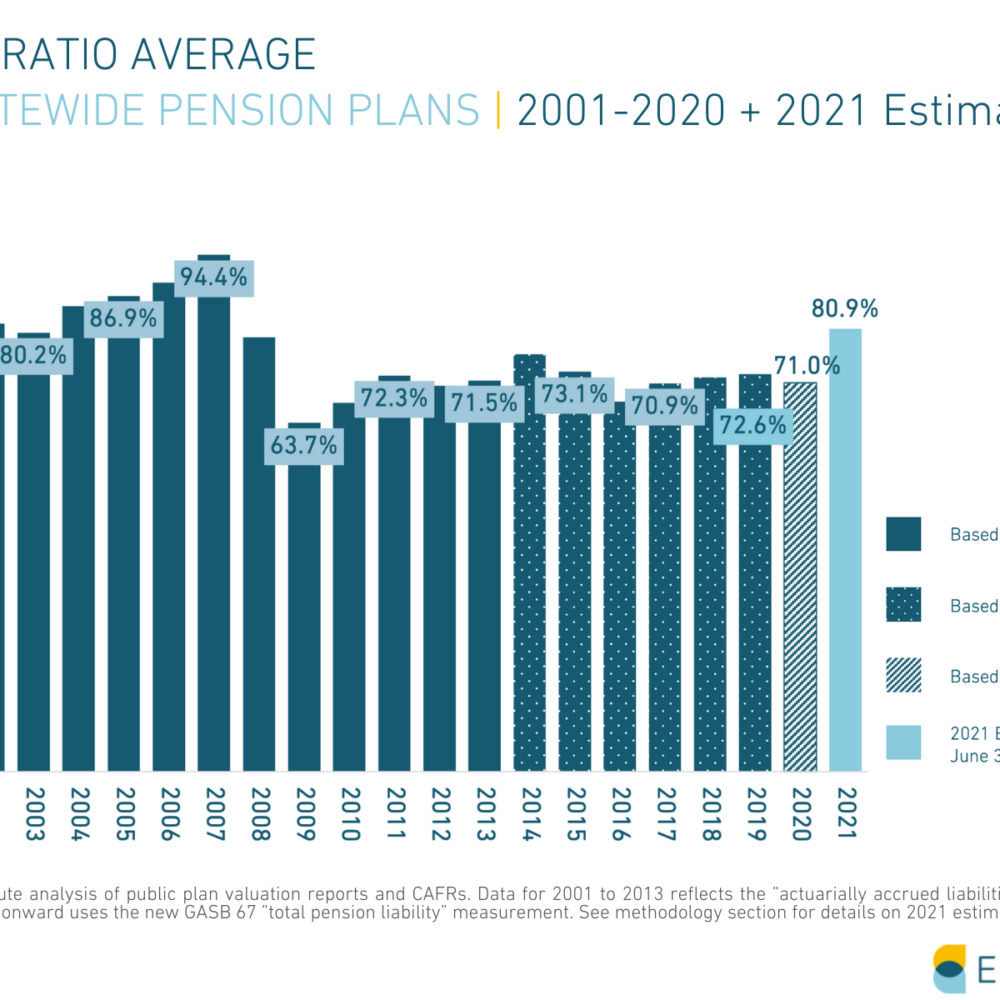

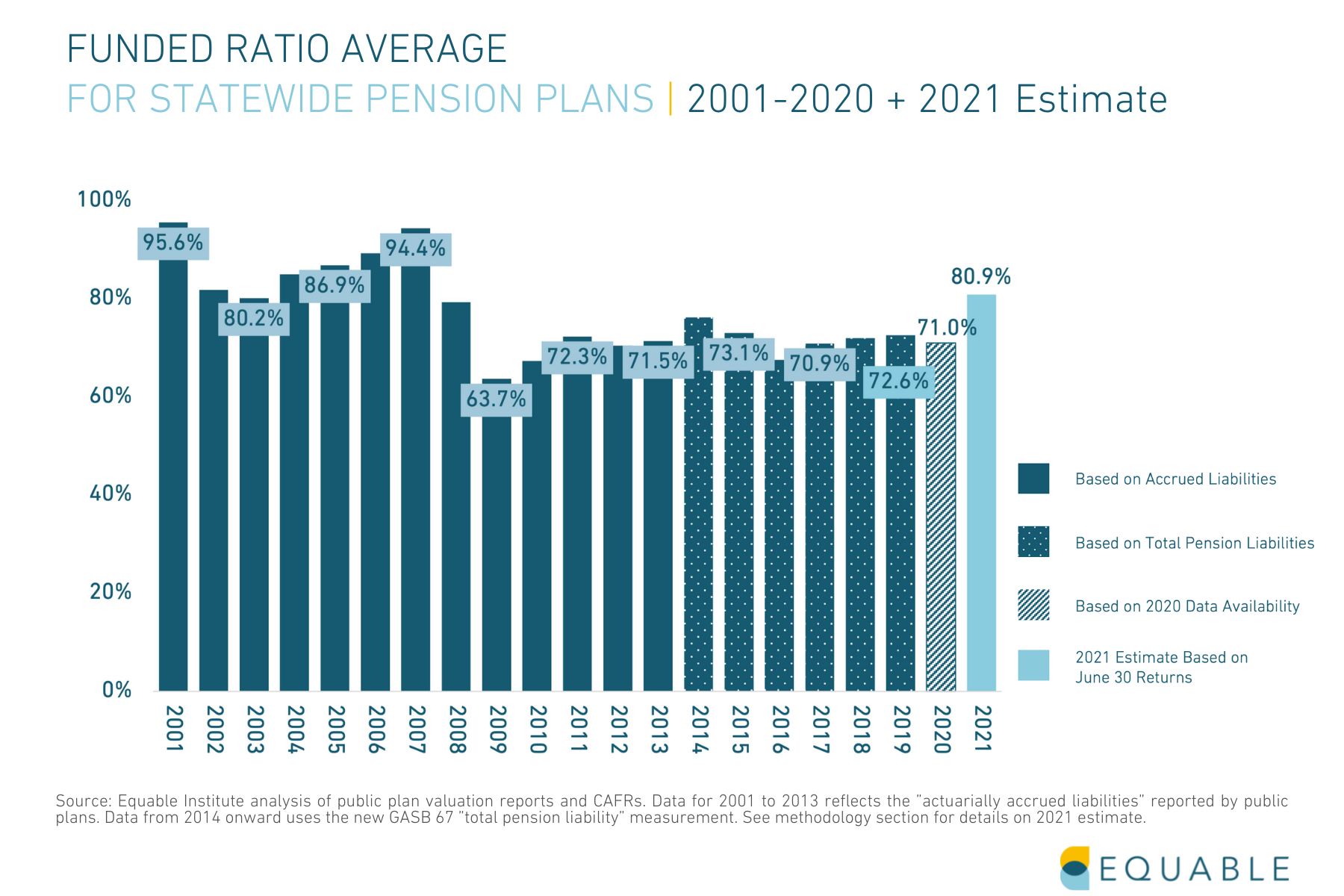

On average, this means American public pensions plans are currently holding 80.9% of assets required to pay future retirees their pension benefits. This is positive, but still much lower than the funded ratios in 2007 or 2008.

By contrast, in 2007 before the Great Recession, statewide retirement systems in the U.S. had 93.8% of the money promised to current and future public retirees. Losses because of the Financial Crisis of 2008 knocked this funded ratio down to 80%.

So while pension funds have been able to recoup the losses experienced during the Covid-19 pandemic, they have still not recovered from the 2008 recession. And capital market forecasts are warning future returns are likely to be muted, perhaps in part because the double-digit returns this year have pulled forward investment returns from future years.

This means the increase in funded ratios will not be long-lasting, especially if states don’t cut their assumed rate of returns.

Why the Assumed Rate of Return Matters

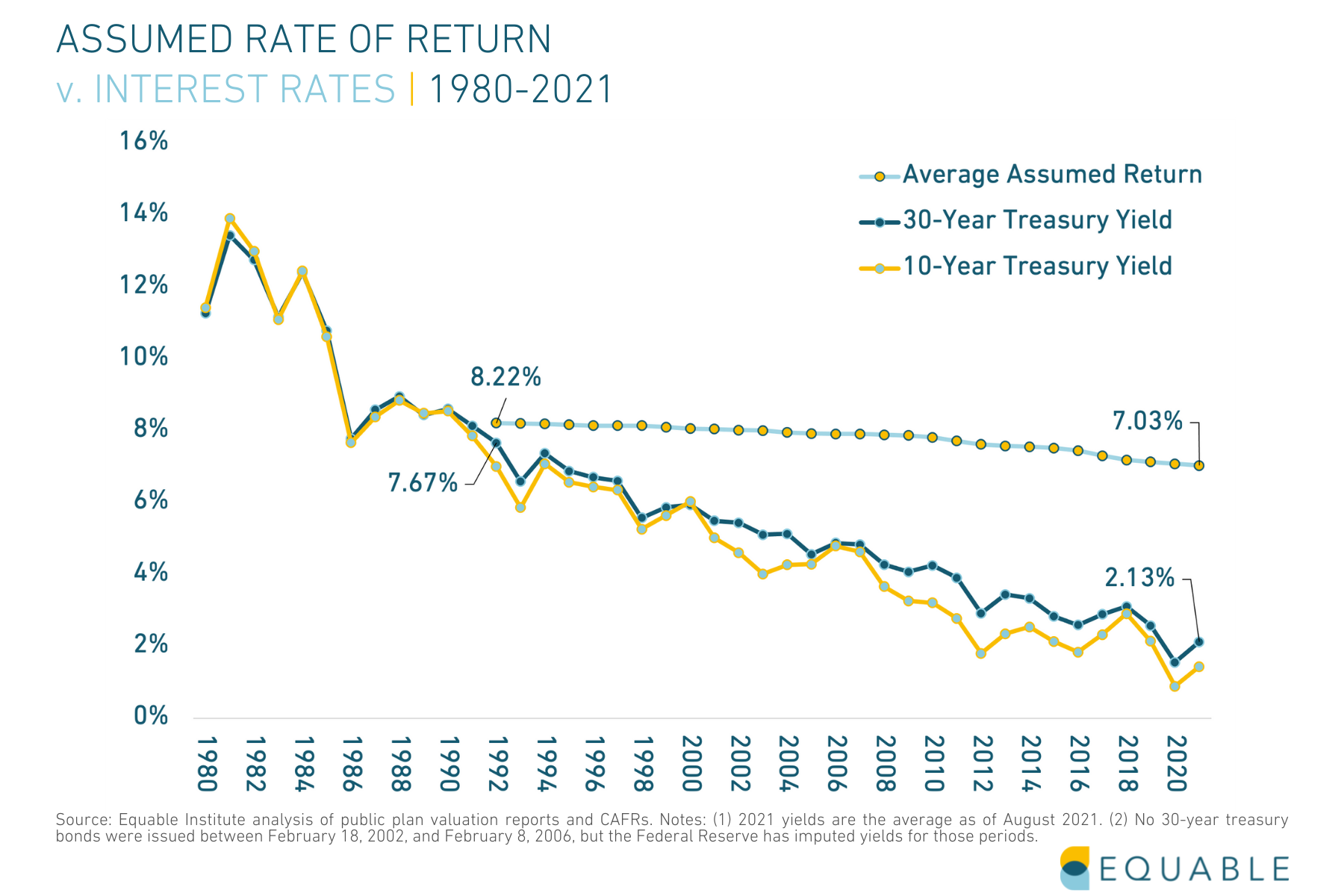

Public pension systems use an assumed rate of return to calculate what dollars will be needed to cover pension benefits due to future retirees. When there is a large gap between (a) the actual returns pension funds receive from their investments, and (b) the rate that they assume they will earn, then (c) pension funding shortfalls grow.

For several years, a significant gap between projected earnings and fiscal reality has existed for public pension plans in many states. Still, the assumed rates of return used by many statewide retirement systems have remained significantly higher than actual investment earnings. A handful of states have meaningfully reduced their assumed rates of return in response to economic shifts, with the average assumed rate of return at 7.03% in 2021—down from 8.05 in 2001.

Interest rates are considered an indicator of future market performance. Declining interest rates indicate that investments will likely see slower investment return gains in the future. This is important because it means that historic performance is not a good indicator of future performance. Many pension funds report that they have had strong investment returns over the past 30 or 40 years — and this is true. But unfortunately those numbers do not actually mean very much for the future. They include investment returns from the 1980s or 1990s, which were very different economic times.

While interest rates over the past two decades have rapidly declined, pension fund assumed rates of return have not kept pace. Meaning many funds are either over-estimating what their investments will earn or they are making a lot of high risk, high reward investments to try and hit their optimistic targets.

The chart below shows the recent trend in assumed rates of return in tandem with interest rates. They have not kept pace with each other. Today, the average assumed rate of return for statewide pension funds is 7.2%. If assumed returns had kept pace with declining interest rates since 2001, the average assumed rate of return in 2019 would have been around 4.9%.

The often highly optimistic assumed rate of return used by most pension funds to make financial decisions may be increasingly hard to achieve if America’s path to economic recovery remains uncertain.

How does national pension funding debt affect public workers?

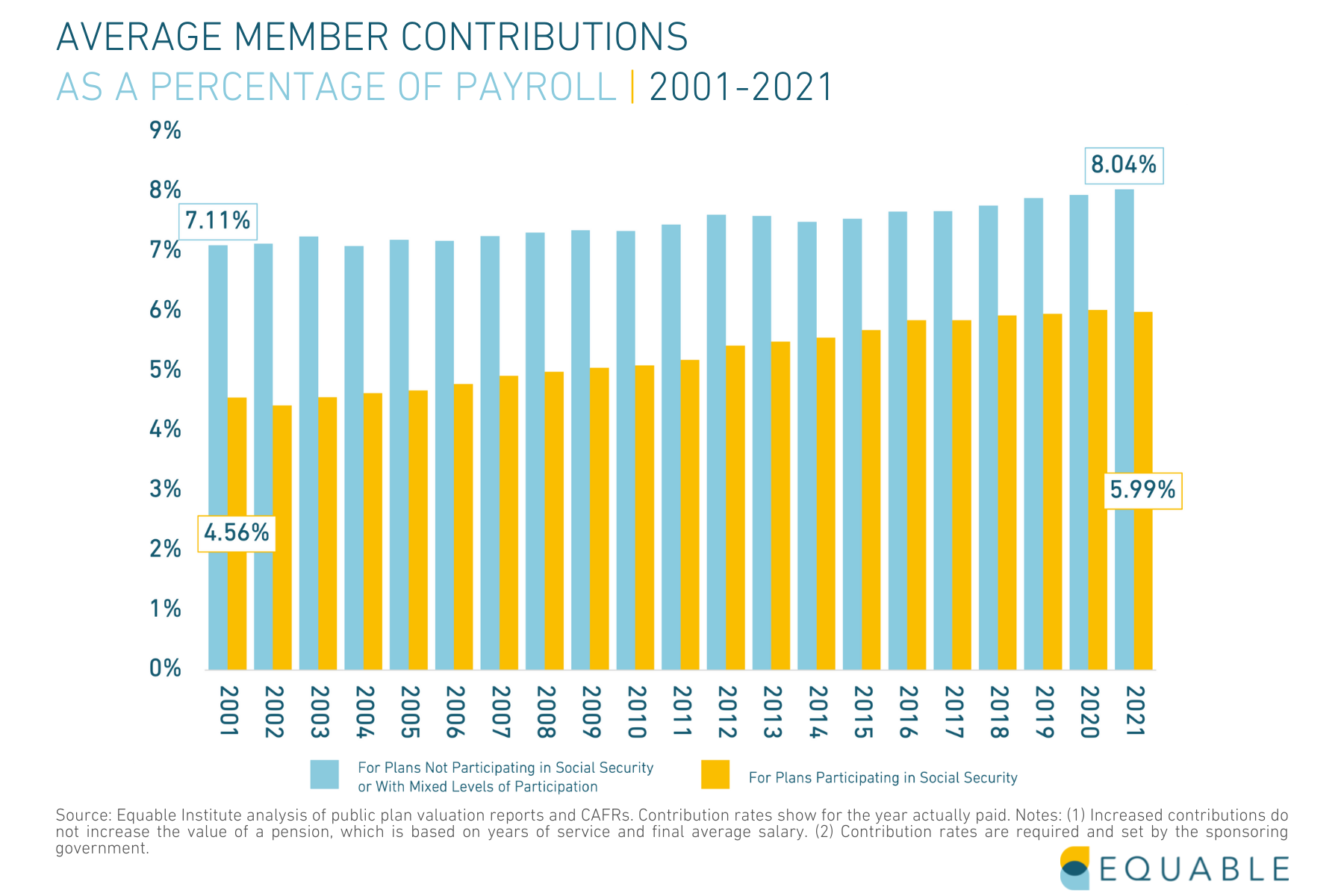

The pension debt carried by governments is costly to pay down and creates pressure on the public budget. It may cause an increase in required pension contributions for public employees or benefit reduction like the elimination of cost-of-living (COLA) adjustments for retirees. Higher employee contribution rates means less money in public workers’ paychecks—and in recent years, the first number has been growing while the latter shrinks.

Public sector workers who are also enrolled in Social Security paid 143 basis points more (a 31.4% increase) during the 2021 fiscal year than they did during the 2001 fiscal year and 20.0% more than they did in 2008 before the financial crisis.

Those who do not participate in Social Security will pay 13.1% more than in 2001 and 9.8% more than in 2008.

In times of economic hardship, higher contribution rates may also result in higher property taxes, delayed raises, cuts in school funding, and a reduction in essential services like public sanitation.

State of Pensions 2021: Public Pension Plans Are Diversifying their Assets

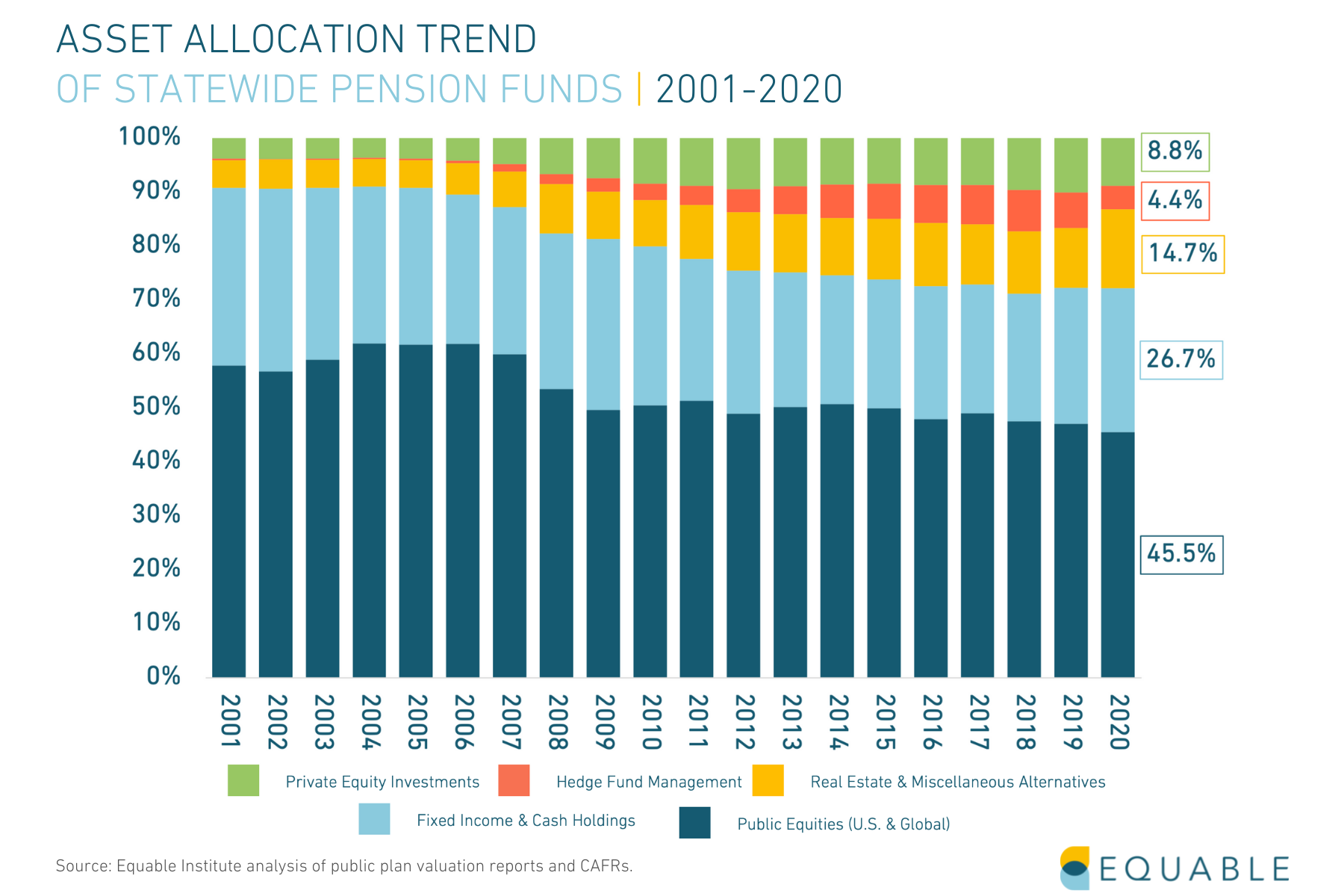

To try and make up for the lower projected returns on stocks and bonds, states will likely continue to utilize alternative investments like hedge funds and private equity strategies to chase higher returns.

Since 2001, pension funds have placed a higher percentage of their assets into hedge funds, real estate, and private equities, investment categories known for volatility in times of economic uncertainty.

Ultimately, as state pension funds are in competition with each other on these deal and market strategies statistically speaking there are going to be plans that lose out on this work. Unless state pension funding in 2021 has particularly better success than the market, it is likely that the net average result across all plans will be relatively modest performance at best and at worst performance below passive equity investment strategies.

Some of the alternative investments that state pension funds have adopted might produce higher returns and might help hedge against sharp downturns in the stock market. But they also carry much higher risks that are only justifiable if the objective is to try and earn an unreasonably high assumed rate of return target.

The State of Pensions 2021: Most Public Pension Systems Are Still Financially Fragile or Distressed

What does public pension underfunding mean for states?

Despite the most recent fiscal year’s strong investment returns, it’s unlikely those earnings will do much to cut the number of plans that are financially fragile or distressed—which right now stands at 49% of all statewide plans. Fragile status generally means a retirement plan is between 60% and 90% funded and, while they’re not at immediate risk of insolvency, they will be building up unfunded liabilities that will gradually become a strain on budgets and government revenues. One or two asset shocks could send the plan into a downward spiral.

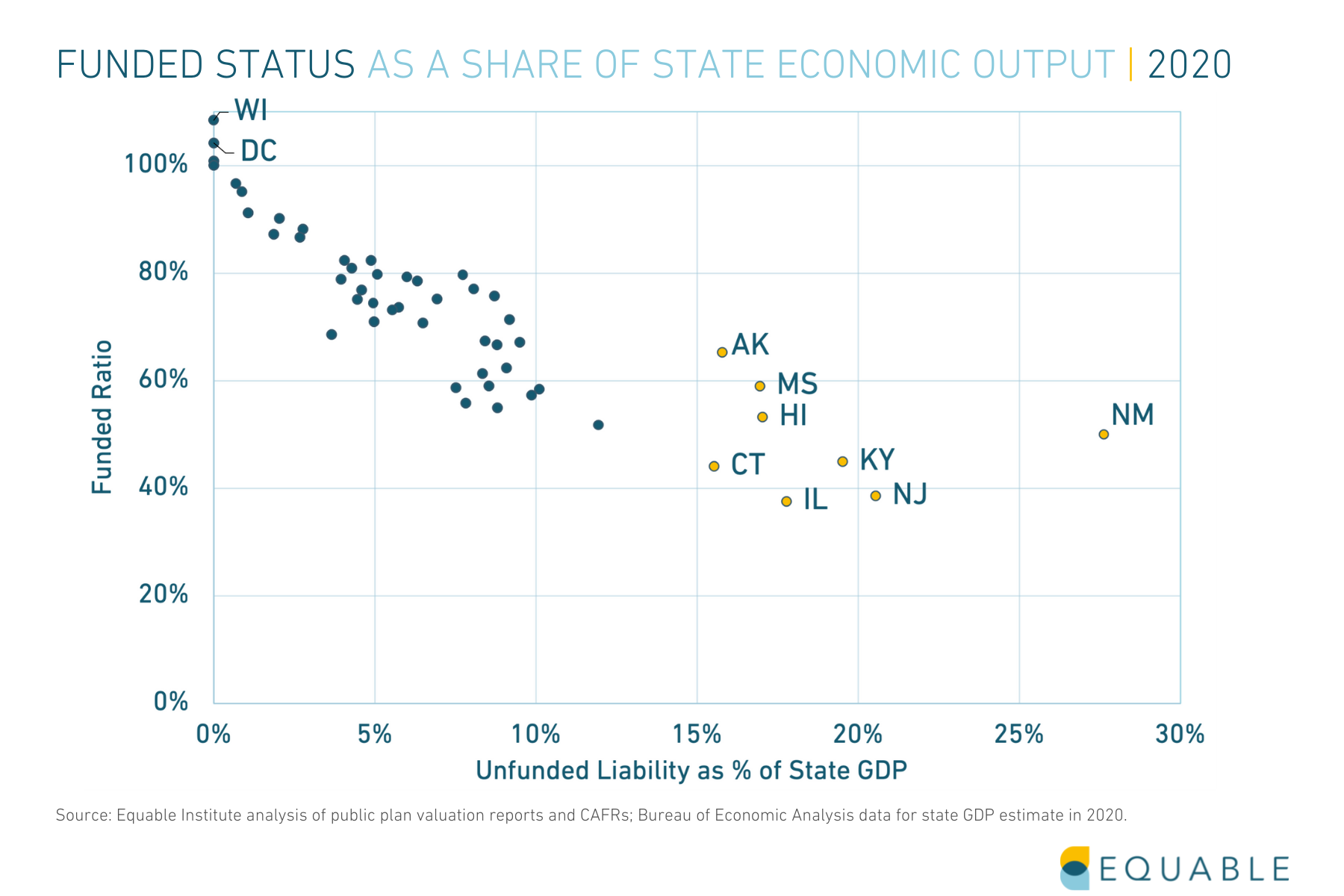

The funded ratio and pension funding shortfall are not the sole indicators of the health of a pension plan. Understanding the size of unfunded liabilities relative to the size of a state’s economy gives a sense of what scale of resources will be needed from a local tax base to improve funded status.

Prior to the pandemic, unfunded liabilities already accounted for a large share of states’ GPDs. We said the pandemic would lead to higher unfunded liability to GDP ratios because of increasing funding shortfalls and economic contraction. Federal stimulus dollars provided by the American Rescue Plan is likely to mitigate much of the expected GDP decline, but the funded ratio dynamics are still at play.

Today, only 26% of all statewide pension plans are considered economically resilient, according to the Equable Institute report, which means holding assets that cover 90% or more of promised public employee pension benefits for at least a few consistent years.

How will underfunded public pension funds cover promised benefits for workers?

There are three strategies that states might take in seeking to ensure they can pay promised benefits to workers: increase contributions into their pension funds, pursue higher investment returns, or reduce the value of benefits.

Cutting benefits is unconstitutional in nearly every state, but in certain places benefits have been reduced by cutting back on the inflation adjustment of pension checks.

Pursuing higher investment returns has been the primary strategy of the past decade. While a few state pension funding 2021 plans were able to recover and some years produced good returns, overall investment returns have not been high enough for everyone to recover. States will continue using this strategy, but it has high risks. And if it doesn’t succeed that leaves only the other two strategies.

The other key strategy is increasing contributions. Usually, when unfunded pension liabilities rise steadily over the years, employer contributions experience an uptick along with required employee paycheck deductions. Just throwing more money into state pension funds doesn’t always help, though, if the underlying reasons that the funding shortfall is growing in the first place are not addressed. That means pension debt and employee contributions may rise unabated until a change in policy mandates a reversal of problematic practices. Even a boon in investment returns has historically offered no guarantee that state and local governments will make debt payments in a timely fashion.

Click Here to Read the Full State of Pensions 2021 Report External Link