A defined benefit plan, commonly called a pension, is a retirement plan for public employees by state and local governments. These plans provide guaranteed retirement income, the amount of which is typically based on one’s final average salary.

There are a lot of misunderstandings about defined benefit plans, perhaps because they are now less common among private-sector employees. In this article, we’ll explain a few different kinds of defined benefit plans and compare their pros and cons.

What is a Defined Benefit Plan?

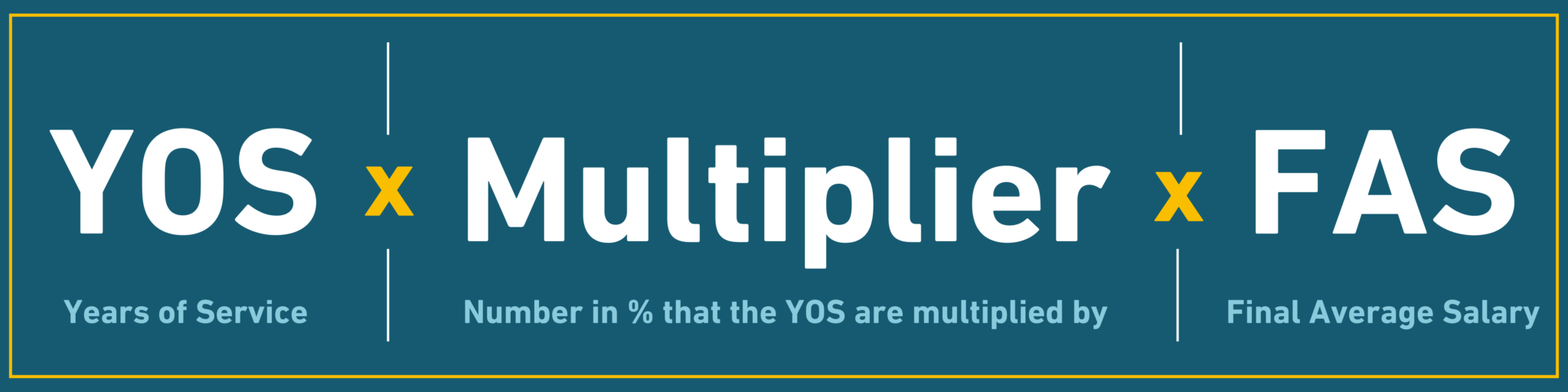

The thing being “defined” in a defined benefit pension plan is the formula used to determine one’s future retirement income.

That formula has three components:

- Years of Service (YOS): This is how many qualifying years an employee has worked for their employer within the pension plan.

- Multiplier: This number is predetermined in state statutes and can vary by state and hire date.

- Final Average Salary (FAS): In most states, this is the average salary an employee earns in the last three or five years of work, though some states use the three or five highest years of salary. Either way, it is a reference to the compensation amount that one’s pension is based on.

The multiplier is used to determine the percentage of one’s final average salary received as a retirement benefit. Years of service are multiplied using this specific number. That amount becomes a percentage of the final average salary. And the result equals the amount that’s ultimately received as a benefit in retirement.

The higher the multiplier, the larger the benefit. Multipliers are sometimes known by other terms, such as “accrual rate” or “crediting rate,” but they mean the same thing.

Notably, the formula doesn’t account for the amount of money saved or even what is contributed into the pension fund. The money contributed by employers and pension plan members matters for building up assets that can pay promised benefits, but the benefit amount paid is only based on the pension formula.

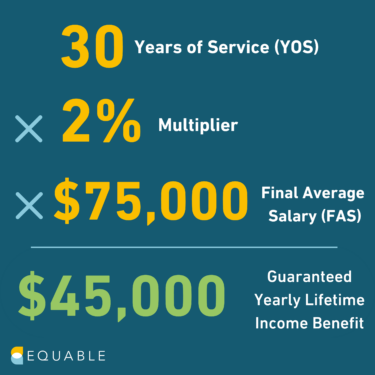

Example: Defined Benefit Plan

A typical multiplier for defined benefit plans is 2%. So, if you work 30 years and your final average salary is $75,000, then your pension benefit is worth 60% of your final average salary.

This is known as your “replacement rate,” or the percentage of FAS that you’ll receive annually in retirement.

In this example, that figure is $45,000, which is your guaranteed lifetime annual income.

What is a Guaranteed Return Plan?

Public defined benefit plans usually are set up as final average salary pensions. However, another kind of defined benefit plan is called a guaranteed return plan (sometimes called a “cash balance” plan).

The thing being defined in a guaranteed return plan is a minimum investment return on contributed assets.

Members of retirement plans and employers both make contributions into guaranteed return plans. The retirement system that collects the money manages the assets and invests on behalf of all employees enrolled in the plan. Members receive at least a certain amount of investment return — such as 4% — plus they can share in the upside returns above this minimum guaranteed rate.

These retirement plans are most common in Kansas, Kentucky, and Texas.

Example: Guaranteed Return Plan

In a typical example, employees contribute into a guaranteed return plan account and are promised 4% minimum returns, plus three-quarters (75%) of any returns above that minimum. So, if a retirement system earns 8% returns in a given period of time, members of the plan get 7% returns (4% + 75% of the additional 4%) on their money, and 1% is set aside to help ensure guarantees in the future are paid when investment returns are low.

When an individual retires, all of the money they have accumulated in their guaranteed return plan account can be converted into an “annuity,” which pays out a lifetime stream of income, just like a pension.

The Pros and Cons of Defined Benefit Plans

Compared to other types of retirement benefits, such as defined contribution plans, hybrid plans, and guaranteed return plans, defined benefit plans come with several main pros and cons.

Pros

- Can provide adequate retirement income security if an employee spends a full career with one employer (or within one retirement system)

- Can support retention goals once employees pass 20 or 25 years of service

- No direct employee investment risk

Cons

- May not provide adequate retirement income security if an employee leaves before 15 to 25 years of service (depending on the plan)

- Limited funding and budgetary predictability

- Very limited portability, as plan designs are for full-career employees

- Underfunding could result in increased employee contributions, lower pay levels, reduced COLAs