State of Pensions is Equable Institute’s annual trends report on the health and performance of public pension funds. Here are some common questions and answers about the state of pensions.

Do the this year’s poor investment returns mean pension funds are falling apart?

No. Just as last year’s strong investment returns on their own were not sufficient to stabilize state and local pension funds, neither are this year’s negative returns going to lead to a wave of bankruptcies. The real threat from the poor returns this year is to contribution rates that will be required from school districts, local governments, and public employees themselves. Low returns mean higher unfunded liabilities, and higher unfunded liabilities mean more required contributions to pay down funding shortfalls. And higher contribution requirements mean more taxpayer resources going to pay for pension debt instead of improving education resource equity, building roads, supporting public housing, addressing climate change, or any number of public goods and services.

What were the positive trends for public pensions over the past decade?

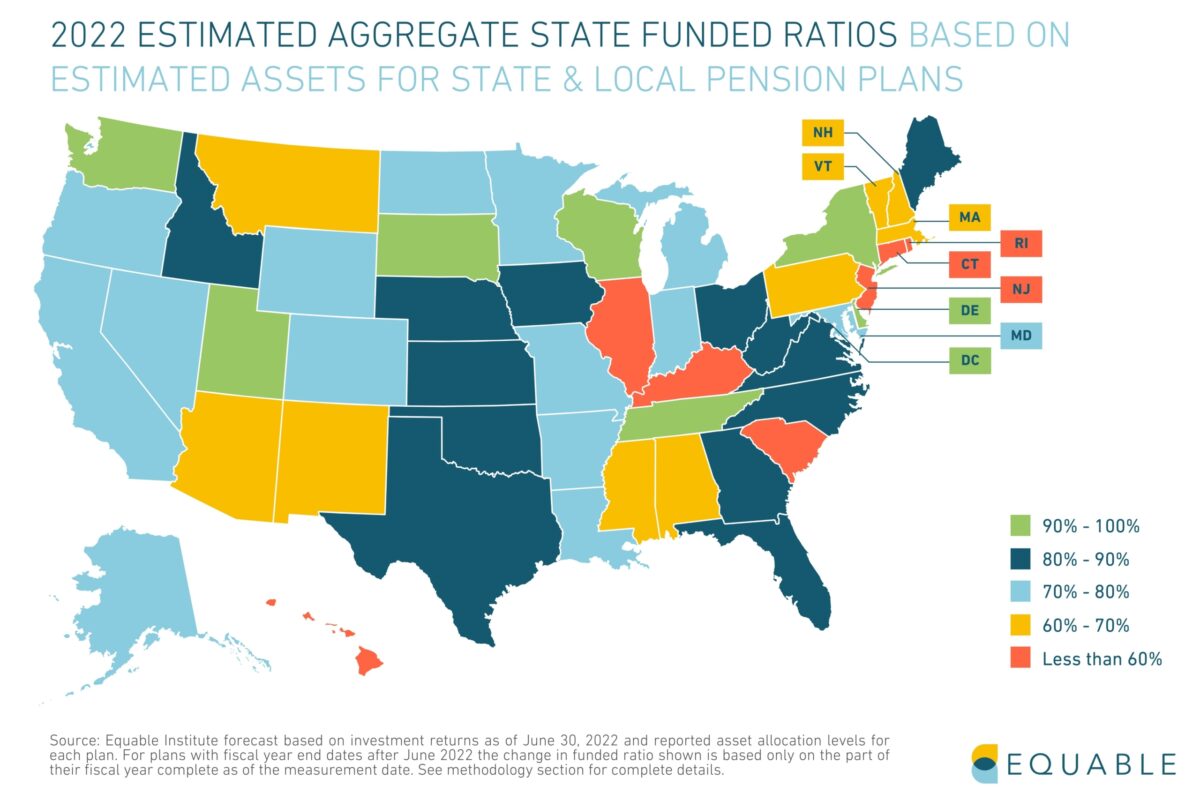

State and local retirement systems are have improved their funded status on average over the past decade, even if the change is small. In 2013, the average funded ratio was around 70%, and in 2019 (before the pandemic), the average was just under 73%. We estimate that even with negative investment returns that the average funded ratio for state and local governments will only decline to 77.9% — which reflects steady, if modest improvement.

State and local governments also paid 99% of their required contributions in 2021, higher than any year since 2001 and a marked improvement from the lower levels of payment following the Great Recession.

What has been the most damaging trend for public pensions over the past decade?

The average assumed rate of return is now 6.9%, which is below 7% for the first time in history — but even this reduction is not fast enough. In the years following the Great Recession, states took only small steps to reduce the amount they were expecting from investments, which meant they didn’t increase their total contributions into pension funds fast enough. Eventually states did make meaningful steps to lower their investment assumptions, but not before unfunded liabilities increased.

Did the Russian invasion of Ukraine hurt pension funds?

In any event, the primary effect of the Russian-Ukraine war has been to put downward pressure on financial markets generally. There was at least $5.7 billion in direct investments from state and local pension funds in Russian or Belarusian assets — almost all of which is worthless right now. But this represents less than 1% of the $5 trillion in assets managed by public pension funds, so it is not a significant harm. The greater harm has been the indirect effects of the war such as food and energy price inflation, and overall stock market decline.

How does inflation influence public pension benefits?

There are two important effects of inflation, one that influences pension plan members and the other that hurts the investment managers. The first effect is that inflation erodes the purchasing power of pension benefit, unless there is a sufficient “cost-of-living adjustment” or COLA. Some public worker pension funds offer COLAs to adjust benefits while others do not.

The second effect is that inflation can put pressure on the people who invest money. Public pension funds already have “negative cash flow” — that is, there are more benefit payments going out the door than contributions coming in the door. This has been going on for some time, but it will get worse because benefit payments are going to be increasing before contribution rates can increase. It usually takes two to three years for a state to adjust its contribution rates, but COLAs will lead to larger pension checks being paid out starting this year. In the meantime, inflation has created negative pressure on investment returns which has reduced the value of assets in pension funds. The net effect is that the people managing pension fund money are having to pay out increasing amounts while at the same time the value of the money they are managing is declining.

Could states and cities just hire more people to fix these problems?

Adding new people to a struggling pension fund is not going to be the magic solution. Those new people would bring additional contributions, but they would also mean additional promised benefits.

Are pension benefits themselves the problem?

No. As states like South Dakota, Wisconsin, New York, and Tennessee have all demonstrated, it is possible to manage a public retirement system well, minimize risks, and keep costs stable. The problem for the rest of the country is political apathy toward unfunded liabilities, and the subsequent challenges that pension debt creates.

Is the trend toward more investment risk a bad thing?

For most states, the additional investment risks they have taken on over the past decade should be a concern. Sometimes shifting assets into a higher risk category — like private equity — can help diversify a pension fund’s assets, and avoid the risk of being too concentrated in one type of investment. But most pension funds doing that are only making the move to try and hit an unreasonably high assumed rate of return. So they are taking on the risk that they underperform, which would lead to unfunded liabilities.

Why does the data in “State of Pensions” start in 2001?

The vast majority of state governments have only made data publicly available starting from 2001, and we think it is important for the data in our study to reflect what states have reported for themselves. It also so happens that 2001 is the strongest year on record historically for public pension funded status, so that provides a good benchmark for states to aim at getting back to.