Resource

Executive Director’s Report | Survival Isn’t Success: The Persistent Fragility of Public Pension Systems

Author/s: Anthony Randazzo

Source: Equable Original

- Benefits

- Funding

- Investment Policy

- Transparency

Tags:

The Fragility of Public Pension Systems

In April 2025, financial markets experienced a sudden and sharp decline, triggered by the Trump administration’s aggressive tariff proposals. For public pension funds, it was another jarring market shock that wiped out hundreds of billions in asset values and threatened an already fragile system. Within a month, markets had rebounded as the White House rolled back the majority of its most destabilizing global economic policies, and public employee retirement dollars returned to their pre-”Liberation Day” levels.

Like the Covid market crash of 2020 and multiple volatility shocks since then, state and local pension funds survived—but they haven’t thrived.

The need to recover losses from April meant missed opportunities for growth. More importantly, the episode revealed how much public plans rely on political events breaking in their favor to produce better returns. State and local pension fund assets aren’t resilient as much they have been fortunate.

Persistent Fragility, Not Resilience

As losses mounted in April, most public pension asset managers urged patience. Their argument was that pension funds are long-term investors with the time and ability to ride out short-term market shifts. As long as insolvency isn’t a near-term risk, concerns about investment returns shouldn’t be overblown.

There’s something to be said for this argument. Pension funds are long-term investors, and attempts to time the market during large swings often lead to worse performance. However, this focus on short-term investment performance misses how contribution rates can increase in the near-term even if investments improve in the long run. The bar for success isn’t just avoiding insolvency.

As it turned out, the Trump administration backed off its most aggressive tariff threats (at least temporarily). However, if investment losses had continued and deepened, they would have led to higher contribution rates regardless of any near-term solvency concerns.

Resilience would mean financial stability—not simply survival. A truly resilient pension plan would be fully funded consistently over time, have stable costs with contributions going toward funding benefits rather than paying off pension debt, and maintain reliable accounting that avoids overstating asset values or understating what’s owed.

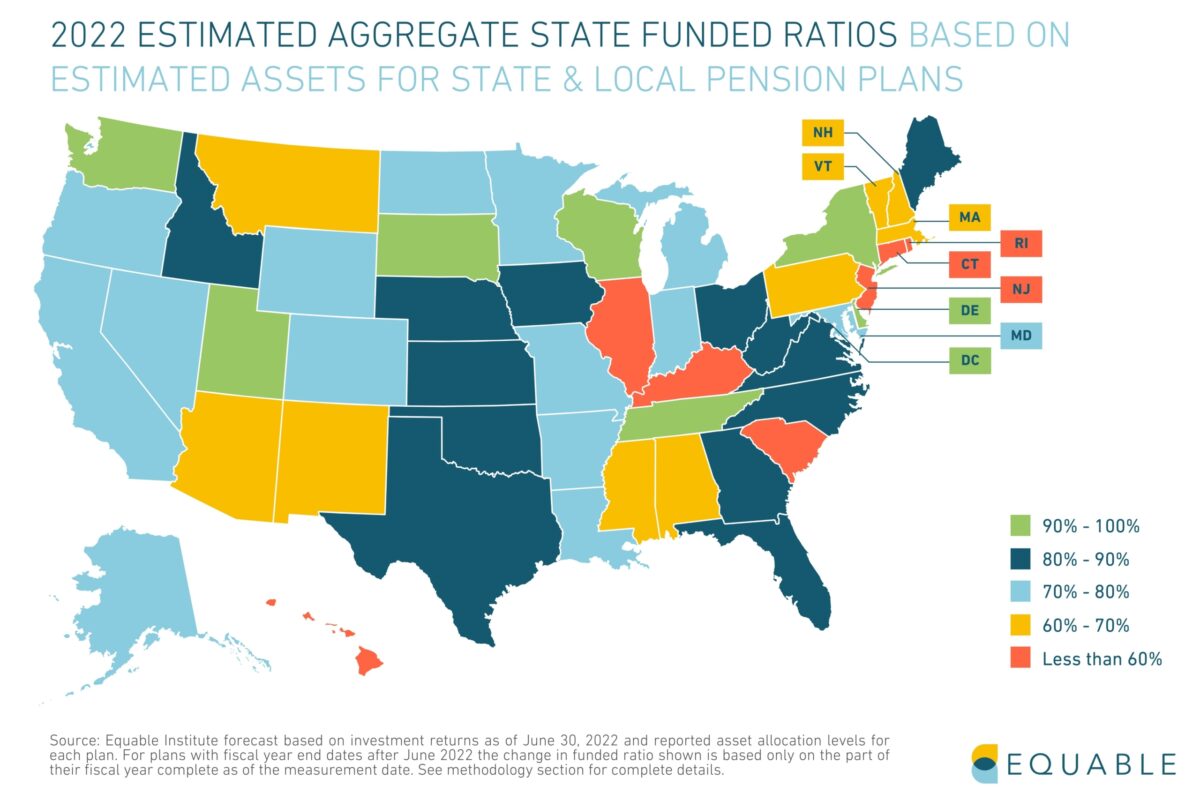

In contrast, state and local pension plans have struggled for decades to regain full funding after the shocks of the early 2000s. Recent investment volatility hasn’t helped. While markets did recover April losses, we estimate that the average 2025 investment return for state and local plans will be 5.41%— well short of the average 6.87% assumed rate of return.

Fortunately for plan funded status, another year of record high contributions has been enough to balance out the underperformance and nudge up the national average funded ratio from 78.3% to 81.4% and shave total unfunded liabilities down from $1.51 trillion to $1.35 trillion.

These numbers are slight improvements from the previous year, but still not back to the most recent high in 2021, which itself wasn’t particularly impressive at just 83% funded. Moreover, the primary reason for any improvement at all is the high contributions flowing into state pension funds from government employers.

Today’s public pension systems aren’t getting meaningfully worse, but they also aren’t getting meaningfully better. Many public plans are caught in what amounts to pension debt paralysis: large, growing liabilities that leave little room for error or genuine recovery.

Asset Strategy Vulnerabilities

Among the primary drivers of public plan fragility is the inflexibility of today’s investment strategies and a lack of tools to counter market downturns. It would not have been unreasonable in January or February of this year to shift assets at least partially into cash given the promises of global tariffs from the incoming Trump administration. However, in reviewing public plan disclosures, there were no major funds that took this approach.

While most plans did not—and could not—adjust their asset allocations in real time, the sudden policy-driven volatility exposed how tightly correlated pension portfolios remain to global economic shocks. For years, asset managers have emphasized diversification across public equities, private equity, private credit, real estate, and commodities. But in practice, these asset classes remain highly synchronized during major global dislocations. Even large private capital investments offer only small protection and often carry their own risks.

The correlation problem is made worse by valuation risk on privately held assets. Private equity and real assets may be significantly overvalued in current portfolio reports. Many private equity and private credit holdings are not marked-to-market with the same frequency or transparency as public stocks, creating the possibility that current funding reports may paint an overly optimistic picture. Should these valuations ultimately adjust downward, funding gaps could widen substantially beyond what current numbers suggest.

Rising Benefit Costs

Beyond investment fragility, the cost of delivering pension benefits is rising in ways that further strain these systems. Over the last five years, normal costs—the value of benefits earned each year—have grown significantly faster than they did in the two prior decades. Inflation-driven cost-of-living adjustments adopted after 2021, along with benefit improvements in states like Illinois, have pushed normal costs materially higher.

This trend adds to the financial stress on plans, requiring higher contributions from employers and employees even when investment returns meet expectations. Each year that plans remain underfunded, the unpaid balance grows not from new benefit promises, but from the compounding effect of failing to fully pay down existing debt. Even when markets cooperate and contributions are steady, many plans continue to see their unfunded liabilities grow simply because the underlying debt is not being fully addressed.

Eroding Fiscal Flexibility

The financial cushion that states enjoyed in recent years is now disappearing, creating additional pressure on already strained pension systems. Pandemic-era federal aid, strong tax revenues, and temporary surpluses are giving way to slower revenue growth and increasing spending pressures. States could also face higher education and health care costs due to changes in the federal government’s approach to the Department of Education and Medicaid, not to mention increased spending related to administering changes in education block grants and Medicaid work requirements.

Pension contributions—already among the largest recurring obligations in many state budgets—may become harder to sustain at current growth rates. Future market downturns could force hard choices between cutting services, raising taxes, or underfunding pension contributions—all scenarios that worsen long-term fragility. This shrinking financial space means that public pension systems are increasingly dependent on favorable outside conditions rather than their own financial strength.

The Survival Trap

Public pension systems today remain precariously balanced, continuing to survive periodic market shocks not because they are inherently strong, but because their survival increasingly depends on short-term market recoveries, budget flexibility, and political decisions outside their control. Each market dip may be survived, but at the cost of further locking in structural weaknesses: payment schedules are extended, employer contributions rise, and budget pressures deepen.

The April market drop is already fading from headlines, but the larger story remains: public pensions are fragile. They are surviving, but they are not thriving. A truly resilient public pension system would not constantly rely on lucky market rebounds or one-time budget surpluses. It would consistently maintain full funding, control long-term cost growth, and minimize exposure to concentrated risks.

Instead, too many state and local plans remain one shock away from deeper instability. Survival should not be mistaken for resilience, and the next shock—whenever it comes—will again test how thin that survival margin has become.