Have you ever wondered how pension contributions work?

If you’re a public employee, you make monthly contributions from your paycheck. If you’re a taxpayer, the government employers you support make periodic or annual contributions, too.

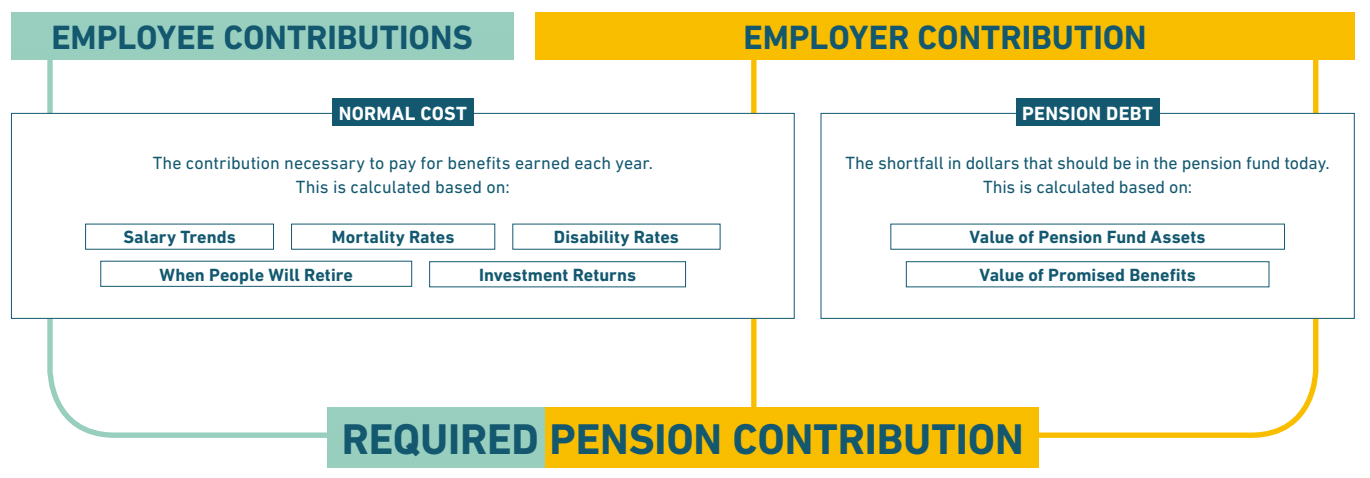

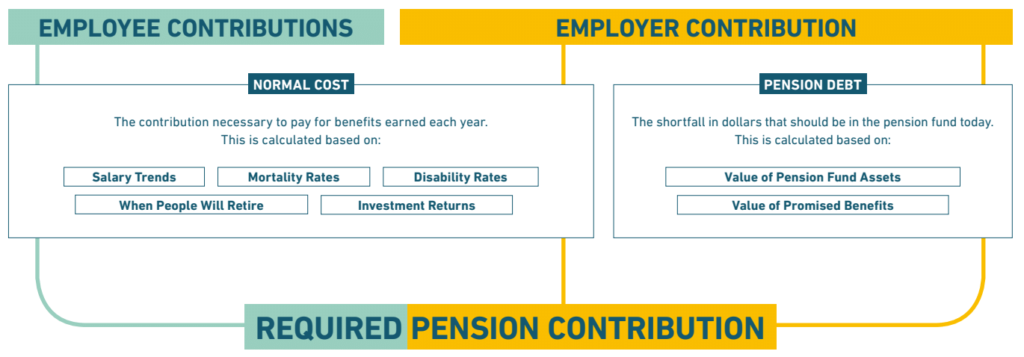

Paying for Benefits Earned This Year: Normal Cost

To make sure a pension plan has enough money to pay out promised benefits, actuaries estimate the total value of pensions that have been earned and make educated guesses about how long people will work, what their salaries will be, how long they will live, and other factors. Then, they use an assumption about how much contributions into a pension fund will earn when they are invested.

Based on this information, actuaries recommend an amount that should be paid into the pension fund for benefits that have been earned this year. This contribution is known as normal cost. In this way, pension plans are not like Social Security, which uses active worker contributions to pay retiree benefits. Instead, pension plans fund benefits in advance with normal cost and investment returns, as depicted in the graphic below.

Backfilling Pension Funding Shortfalls: Pension Debt Payments

Pension plans are designed to collect contributions from active workers, invest that money to produce a return, and use the combined assets to pay promised benefits. If the pension design is working, assets will be equal to the estimated value of benefits promised.

When the value of assets drops below the value of benefits promised, that shortfall in funding status is called an unfunded liability. This shortfall is money that is owed to the pension fund by the relevant state or local government. Employers make pension debt payments into the fund, kind of like a mortgage payment, until the value of assets and promised benefits are equal.

Dividing Up the Contributions

Employee pension contributions are first applied to the normal cost. They are almost always less than the normal cost (otherwise the pension wouldn’t be much of a benefit). The remaining normal cost is paid by employer contributions. Any remaining employer contributions are put towards paying off pension debt.

As the infographic above shows, employee and employer contributions flow down to the total required contributions through normal cost, which is created using a range of actuarial assumptions. Pension debt payments are covered by employer contributions.[1] The combined total of employee and employer contributions should equal the actuarially determined contribution rate. Some states do not always pay this rate, which undermines pension fund sustainability.

Notes

- There are a few exceptions to the rule that employers pay all of the unfunded liability payments, such as Arizona’s retirement systems and the teacher pension plans in Michigan and Ohio. Generally, these are rare instances.