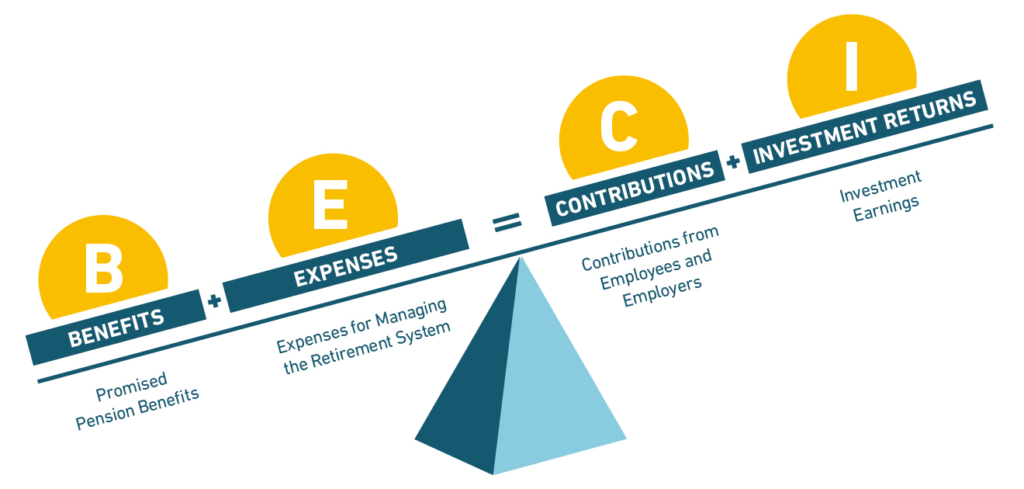

Pension plans are designed to collect contributions from active workers, invest that money to produce a return, and use those combined contributions and investment returns to pay promised benefits.

This design means that when a pension plan is working as it should, the fund will hold assets equal to the estimated value of the benefits it has promised to pay. When it does not work as it should, it creates unfunded pension liabilities, or pension debt.

What are Unfunded Liabilities for Pension Plans?

Unlike Social Security, which uses money from today’s workers to pay today’s retirees and does not invest assets, pension funds should receive money today that can be invested to achieve the total needed to pay retirement benefits in the future.

When the value of assets falls below the value of benefits promised, a pension fund has unfunded liabilities. To understand this concept, it’s important to distinguish between liabilities and unfunded liabilities:

- The liability is the promise to pay benefits; it is a formal financial term that indicates both a moral and legal obligation to pay a promised retirement benefit. The pension plan and the government that created the pension plan are obligated to pay the benefits they have promised, thus those promises are liabilities.

- When a pension fund has a shortfall in assets, there is an unfunded liability.

For example, if a pension fund has promised $1 billion in benefits to current retirees and working teachers, it should have $1 billion in assets. If that pension fund only has $900 million in assets, it has a $100 million shortfall.

This is kind of like the pension funding formula becoming imbalanced, as illustrated in the image above.

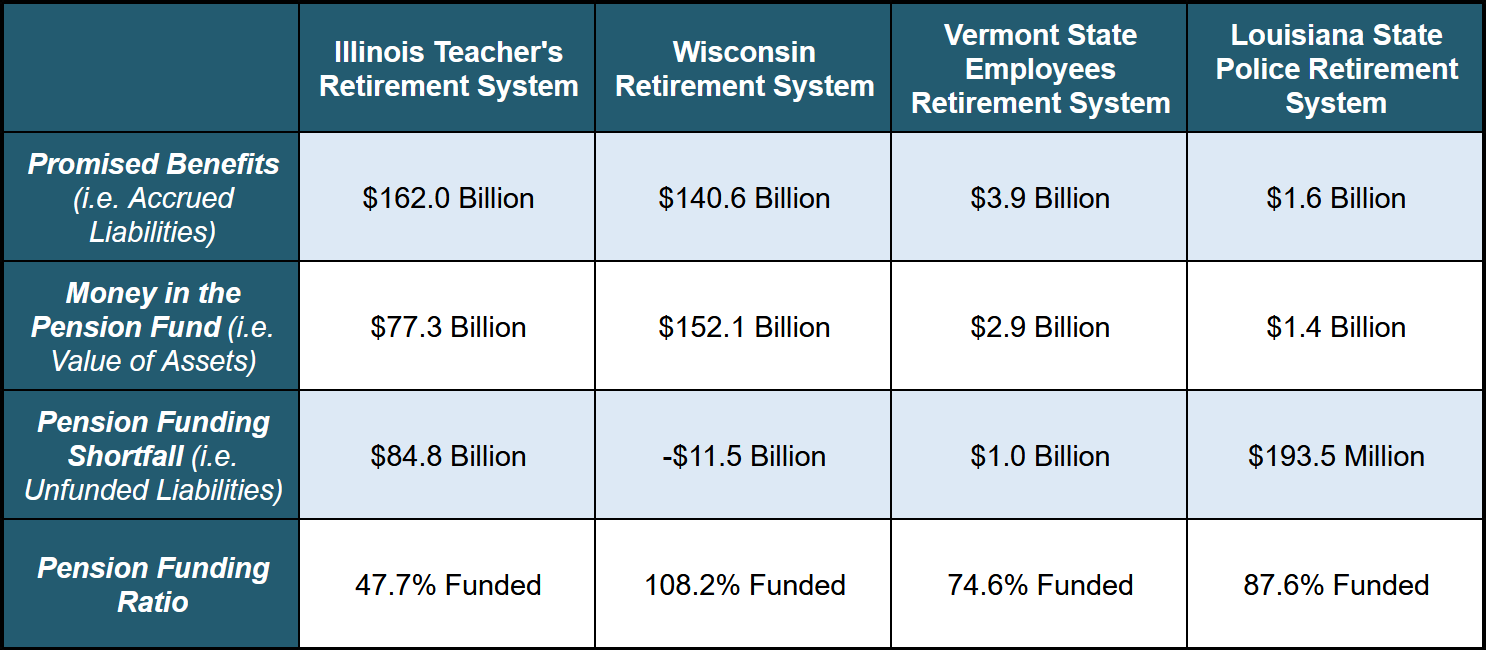

Examples of Unfunded Liabilities

Below are some real examples of unfunded liability levels for state pension funds.

This shortfall in pension funding — the unfunded liabilities — is money that is owed to the pension fund by the relevant state or local government. Employers make “amortization” payments into the pension fund that are regular, additional contributions made until there is no more funding shortfall. This is similar to making mortgage payments that pay off debt on a house. Thus, sometimes, people call unfunded liabilities “pension debt.”

To find out what the unfunded liability is for pension funds in your state and learn more about what unfunded liabilities mean for state pension plans, check out this article.

This article is part of Equable’s Pension Basics series. To learn more about how your pension works, check out the other articles in the series:

1. How Pension Benefits Are Calculated

2. Vesting

3. The Pension Funding Formula

5. Normal Cost

6. Unfunded Liabilities (aka Pension Debt)

7. Actuarially Determined Contributions

11. Pension Myths & Facts: The Assumed Rate of Return Does Not Determine the Value of Benefits

12. Pension Myths & Facts: The Funded Status of Pension Plans Does Not Depend on More Public Employees