Public Pension Transparency

Find research, data, news, and analysis on the laws, policies, and initiatives driving greater transparency and oversight across public pension funds.

Accountability and sound governance are essential to maintaining public trust in retirement systems.

Public pension funds hold a profound responsibility: managing the retirement security of millions of public workers while stewarding significant public resources. Transparency and sound governance are essential to ensuring these systems operate in the best interests of their beneficiaries, and that policymakers, employees, and the public have the information they need to hold them accountable. Without clear reporting standards, accessible data, and strong oversight frameworks, it becomes difficult to assess whether funds are being managed prudently or whether benefits will be there when workers need them. The laws, policies, and practices governing pension fund transparency have direct implications for public trust, fiscal accountability, and the long-term health of these critical institutions.

Equable Insights

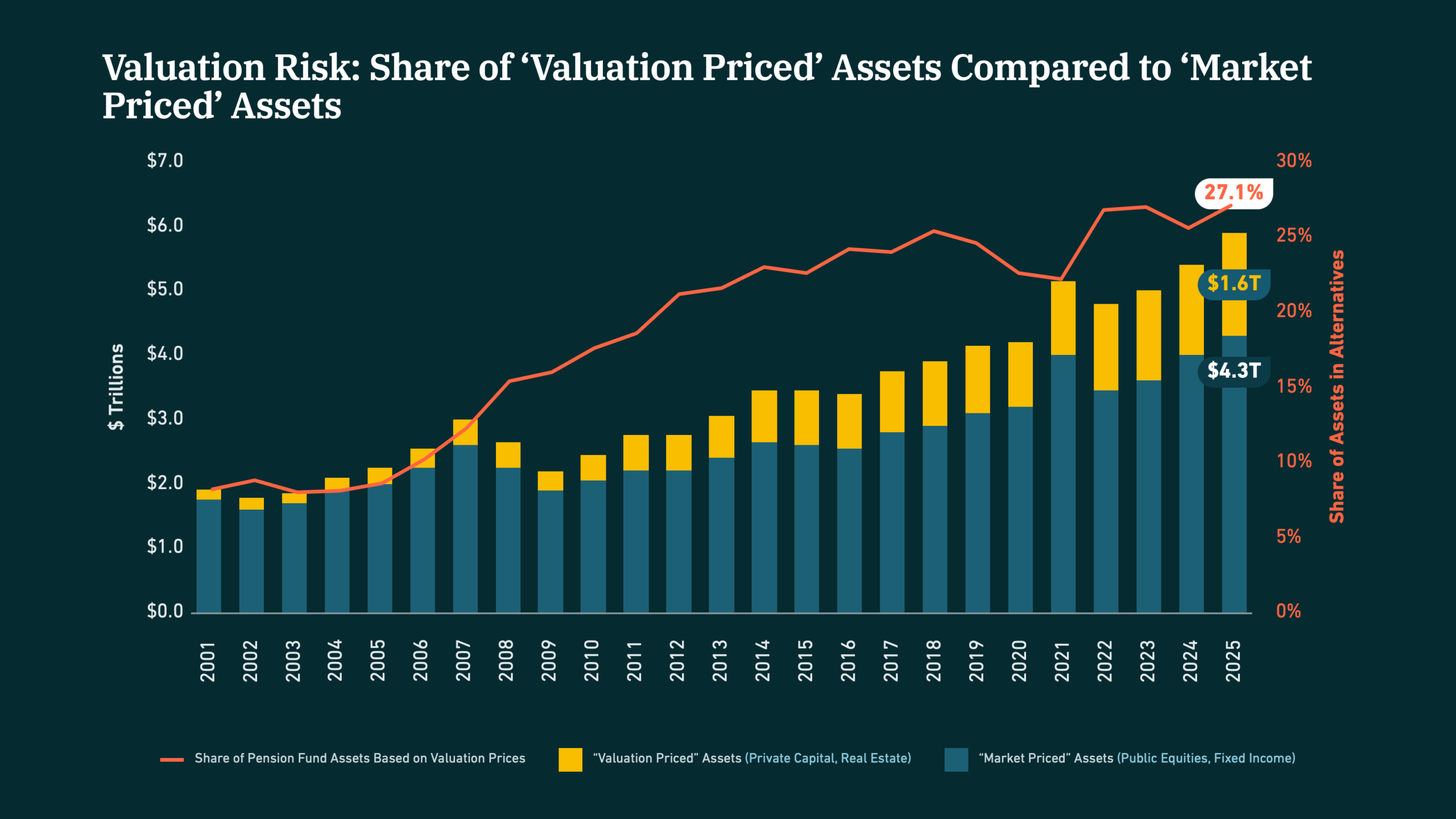

Valuation Risk

“Valuation Risk” is the risk to pension funds that the value of their assets as reported to them is inaccurate (e.g., understating or overstating the actual value) because the asset pricing method used is based on valuation models, as opposed to market-based prices.

If asset values are overstated today, then that means reported funding levels are overstated. This in turn can lead to lower than appropriate contribution rates, which will mean larger unfunded liabilities in the future than if assets were more accurately priced.

The share of pension fund assets exposed to “valuation risk” has tripled since the Global Financial Crisis.

Featured Resources

Research, data, analysis, and educational resources on public retirement system transparency and governance.

Public Pension Transparency FAQs

Answers to common questions about public pension transparency.

In most states, pension funds are managed by a board of trustees representing stakeholders, including teachers, retirees, the legislature, the treasurer’s office, and the governor. Some states also have independent members that represent the financial community or taxpayers, while others have an auditor, comptroller, or other oversight official on the pension board. Pension boards are fiduciaries, which means they are required to make decisions that are in the best interests of plan members.

Pension plan assets are invested in a wide range of asset classes, such as stocks, bonds, real estate, private capital, hedge funds, and/or alternatives. To see the investment mix for your pension plan, check out our interactive Financial Resilience Report tool. Select your state, system, and plan to see details about how plan assets are allocated.

Every state protects public pensions to some degree. They are typically protected by state constitutional provisions or statutes enacted by the state legislature, which ensure that any benefits earned by public workers cannot be reduced or eliminated retroactively. For details about your state’s specific pension laws, we’ve compiled a series of infographics that map states’ pension governance.