Public Pension Funding

Find research, news, and analysis on how retirement systems are funded, the challenges they face, and the policies shaping their sustainability.

The long-term health of public retirement systems depends on sound funding policy.

Decades of persistent underfunding have compounded into serious structural challenges. State and local pension systems now carry more than $1 trillion in unfunded liabilities, and governments are paying record-high contributions just to keep pace. This has far reaching impacts for both public workers and the communities they serve.

Featured Research

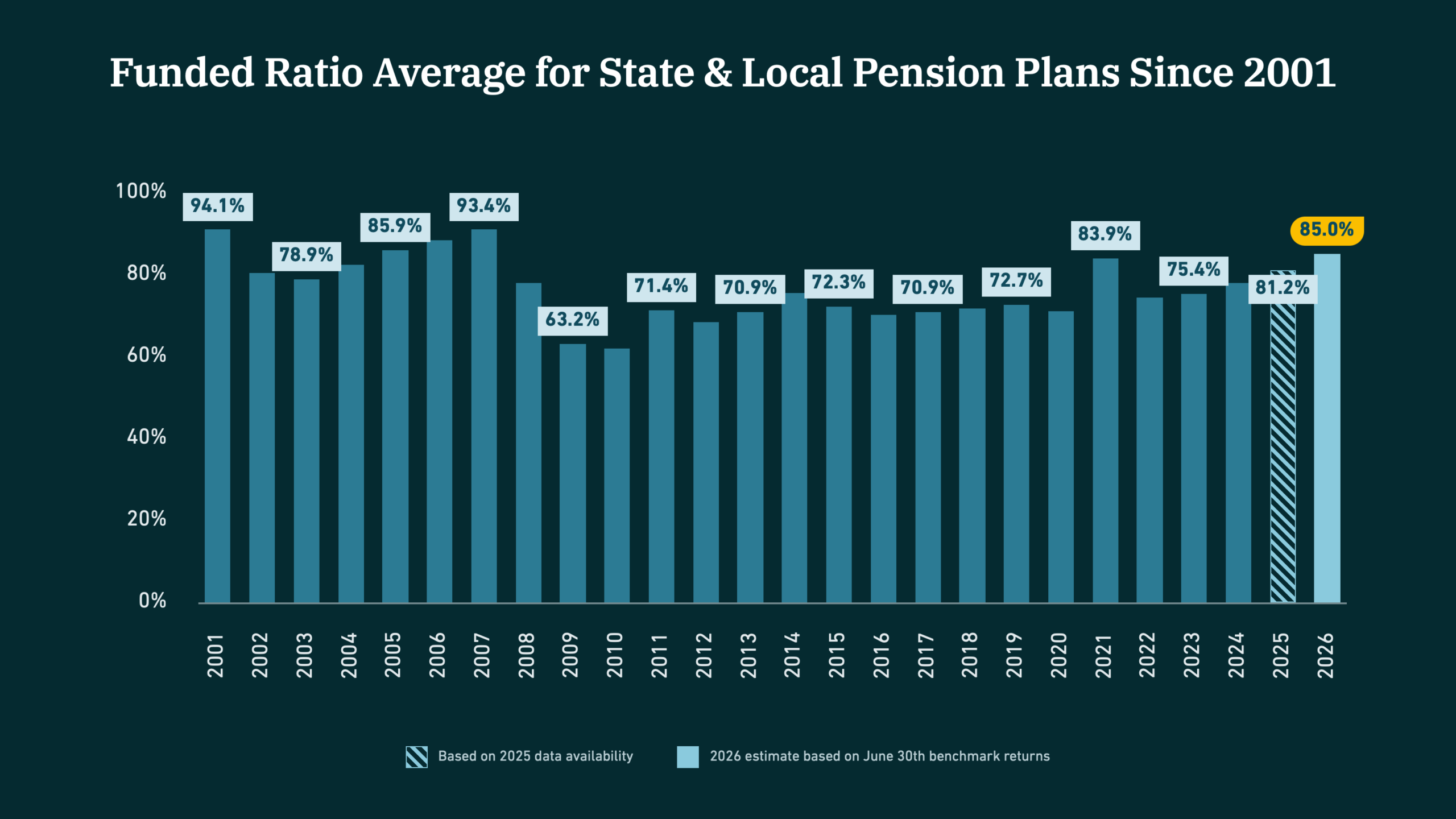

State of Pensions 2026

The national funded ratio average reached 85.0% in 2026, up from 81.2% in 2025. This marks the fourth straight year of improvement.

Featured Resources on Funding

Research, data, analysis, and educational resources on public retirement system funding.

Pension Funding FAQs

Answers to common questions about public pension funding and funding policy

The main measure of how well a pension is funded is called the funded ratio, which is calculated by dividing a plan’s assets by its liabilities. Equable projects that the overall funded ratio for public pensions reached 85.0% in 2026. To find the funded ratio and other metrics of fiscal health for your specific pension plan, use our Financial Resilience Report tool.

Unfunded liabilities, also called pension debt, accrue when the value of a pension fund’s assets falls below the value of benefits promised. Total unfunded liabilities for U.S. public pensions have mostly been at or above $1 trillion since the financial crisis of 2008-09 and currently stand at an estimated $1.13 trillion as of 2026. As unfunded liabilities increase, public employees may be required to contribute more from each paycheck (reducing take-home pay), a state may have less money for salary increases, or cost-of-living adjustments may be reduced. You can see how much pension debt your plan carries by searching our Financial Resilience Report tool.

The exact way a pension plan is funded depends on which state it’s being offered in. Typically, though, pensions are funded with contributions from public employees and government employers. This money is then invested in various asset classes, such as stocks and bonds, with the expectation that it will earn returns in the future. The combination of contributions and investment returns pays for a pension’s promised benefits.

With a few exceptions, unfunded liabilities are paid for by public employers or states via amortization (debt) payments. Employee contributions to pensions are typically only used to pay for the employee portion of normal cost.