Missouri

Missouri Pensions

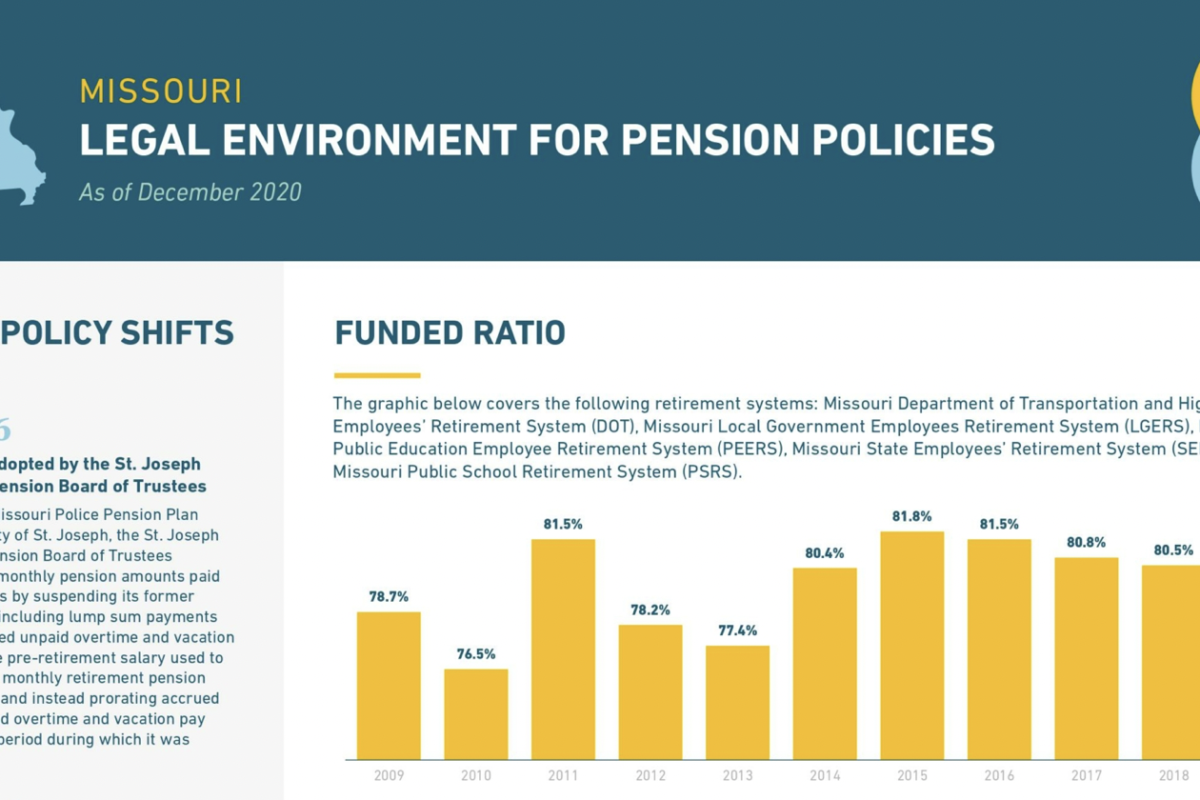

The state of pensions in Missouri is Fragile

News and Resources Specific to Your State

Signature Reports

Flagship research products, updated regularly to track public retirement systems and their impact on workers and communities.

State of Pensions

State of Pensions is Equable Institute’s annual report on the status of statewide public pension systems, put into a historic context.

Retirement Security Report

The Retirement Security Report (RSR) is a comprehensive, interactive assessment of the quality of benefits being offered to public sector workers nationwide.

Hidden Education Funding Cuts

Hidden Education Funding Cuts analyzes state and local K-12 education spending relative to growing teacher pension debt.

Info for

Public Workers

We can help you understand your retirement benefits, the policies that shape them, and the news that matters to you.

Journalists

Our data, research, and expert voices are here to support your reporting on public retirement systems and the people they serve.

Advocates

We provide research, data, and expert support to inform and strengthen your advocacy.

Policymakers

Rigorous, nonpartisan research and technical assistance to support informed decision-making on public retirement policy.

Explore by topic

Benefits

Explore research, data, news, and analysis on the retirement benefits that serve millions of public employees across the country.

Funding

Dive into research, data, news, and analysis on how public retirement systems are financed, managed, and sustained over the long term.

Investment Policy

Discover research, data, news, and analysis on the investment strategies and policies that shape public retirement system portfolios.

Governance

Access research, data, news, and analysis on efforts to improve public pension fund transparency, governance, and accountability

Stay Up to Date

Sign up for our newsletter to get the latest news in public retirement straight to your inbox.