Report

STRS Ohio Needs More Money.

We need to ensure the Ohio State Teachers Retirement System has adequate funding that doesn’t come at the cost of classroom resources, student needs, or retirement security for teachers.

Previous reforms to STRS Ohio have failed to adequately address persistent underfunding that threatens the income security of retired teachers and the budget stability of school districts.

The math is clear: more needs to be done.

STRS Ohio recently asked state legislators to increase pension contribution rates that flow into their system for teacher retirement benefits. The need for more money is unambiguous when assessing the fiscal condition of STRS.

Additional contributions today are necessary both to avoid even higher costs in the future if pension debt isn’t paid off and to ensure retired teacher benefits are inflation protected.

Unfortunately, this will require more resources in the near-term to avoid higher costs in the long-term. And it is really important that the policy for how those costs are distributed doesn’t reduce resources for kids.

Traditionally, school districts pay all of these “employer” contributions for teacher retirement pensions.

However, if retirement costs for school districts increase without some offsetting revenue, this would effectively be an education funding cut. The increased pension costs for districts expand projected budget deficits, lead to cuts in K-12 services, and could even mean fewer teachers.

Mouse over the map to see just how much budget deficits could grow if necessary Ohio STRS contribution increases are passed down to school districts.

The Challenges Facing STRS OH

The challenges facing STRS Ohio have developed over the course of the last couple of decades and threaten the quality of Ohio's K-12 public school system and retirement benefits for teachers. To begin to understand how to address these problems, it's important to ask three primary questions:

Why Does STRS Need More Money?

Previous reform efforts that cut COLAs for retired educators and increased contributions from school districts did not adequately address STRS' $30 billion shortfall. More needs to be done.

What is the Additional Money For?

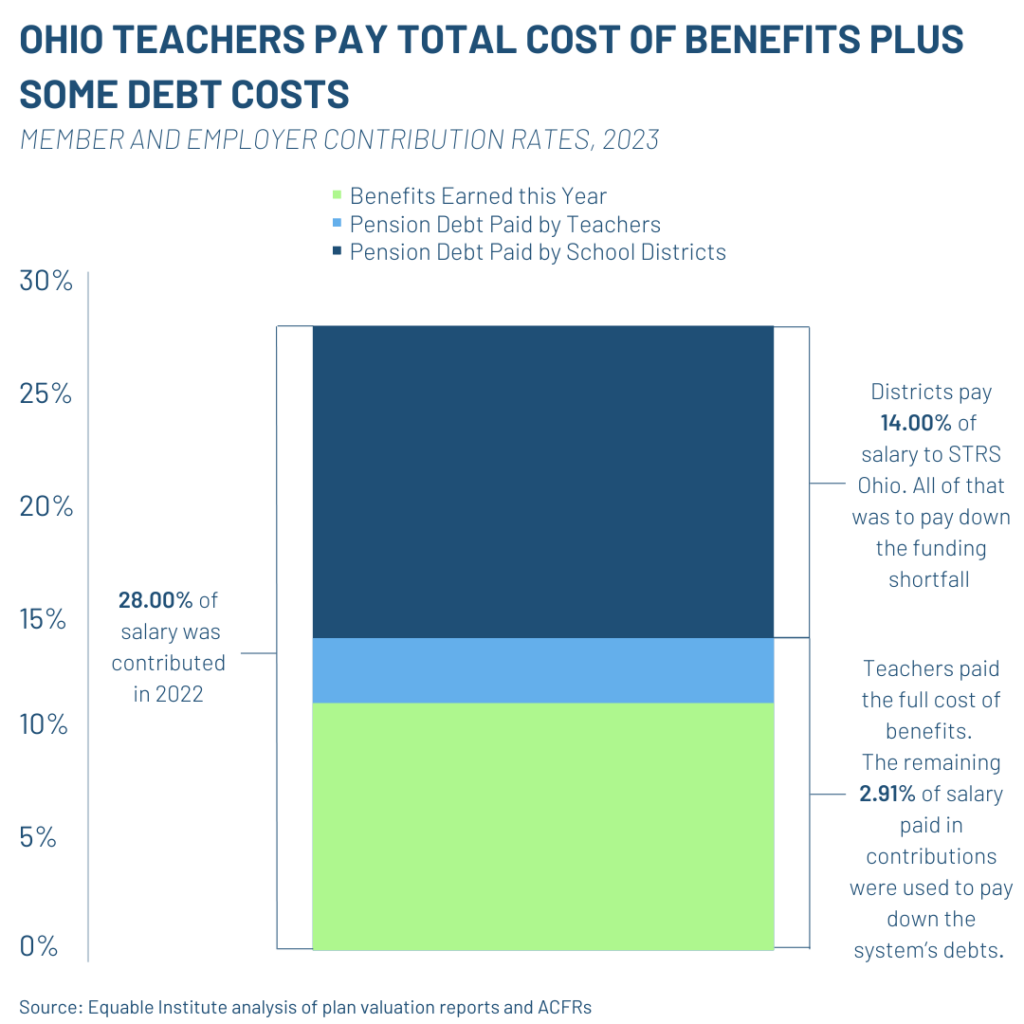

More money is needed to pay for teacher pension debt. Currently, 100% of employer contributions and 20% of teachers' contributions to the pension fund goes toward debt payments.

Who Should Pay for Increased Costs?

School districts and educators are already over-extended with contribution rates. It's eating into school budgets and take-home pay. The state needs to find a solution that protects schools and teachers.

Why Does STRS Ohio Need More Money?

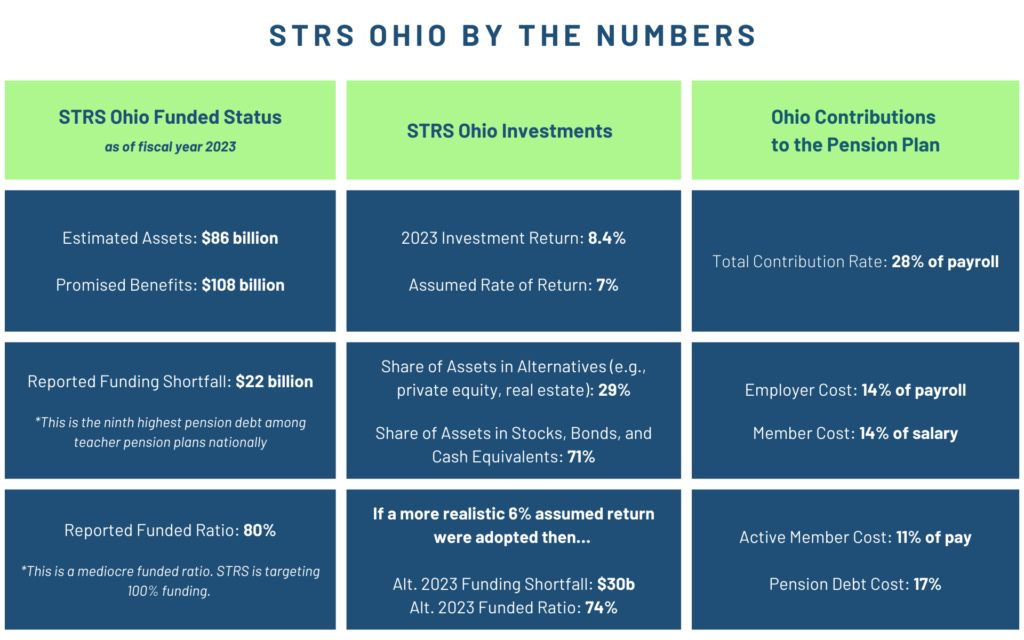

A decade ago, Ohio launched a pension reform effort that increased teacher pension contributions, reduced benefit values, and eliminated COLAs. Despite all of this, STRS Ohio still has around $20 billion to $30 billion in pension debt. And every dollar that school districts contribute to STRS is just for paying down this pension debt. (Teachers cover the whole cost of their own benefits.)

The status quo needs to change and STRS Ohio needs to improve its pension accounting practices while also restoring benefit security to retirees whose incomes are not adequately inflation adjusted. This means more contributions into STRS are necessary and appropriate — but it is critical that such increases do not lead to budget cuts at school districts.

SUSTAINABLE FUNDING

(CLICK TO EXPAND THE SECTIONS BELOW TO READ MORE)

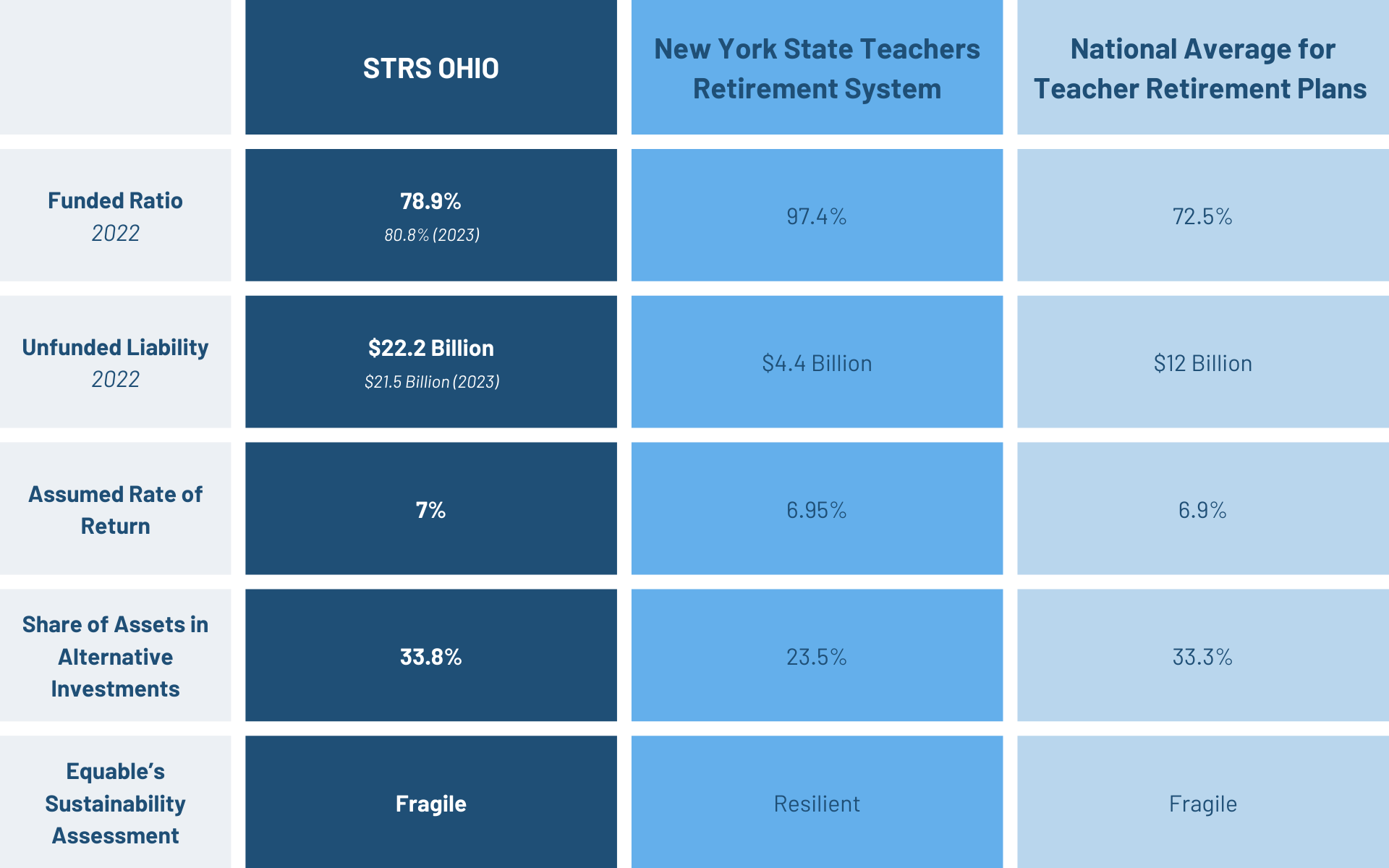

STRS Ohio is currently assuming it can earn 7% annual average returns on its investments. This is unrealistic. At best, there is a 50% chance that STRS will hit this investment target.[1] If they don't meet their investment goal, then STRS will accumulate more unfunded liabilities.

Continuing to target 7% annual returns requires taking considerable investment risk. STRS is aiming to invest nearly $1 of every $10 dollars it has in private capital.[2] That may be a reasonable strategy to try and hit an ambitious investment target, but it should be clear to all stakeholders that this comes with considerable risk. Investments in areas like private equity can have big wins, but also have big losses—and STRS Ohio's past private equity investments have experienced both.

Notes

[1] See "Range of Projected Returns" forecast from Callan, as reported by STRS Ohio Investment Department, March 2023.

[2] The same March 2023 report shows a projected asset allocation of 9% to "private equity." A December 2023 report showed 11.3% of assets in "private equity." STRS Ohio counts "private credit" in a different asset class, according to their regular asset allocation report, meaning the total scope of investments in private capital aims to be around 10% or more of the portfolio.

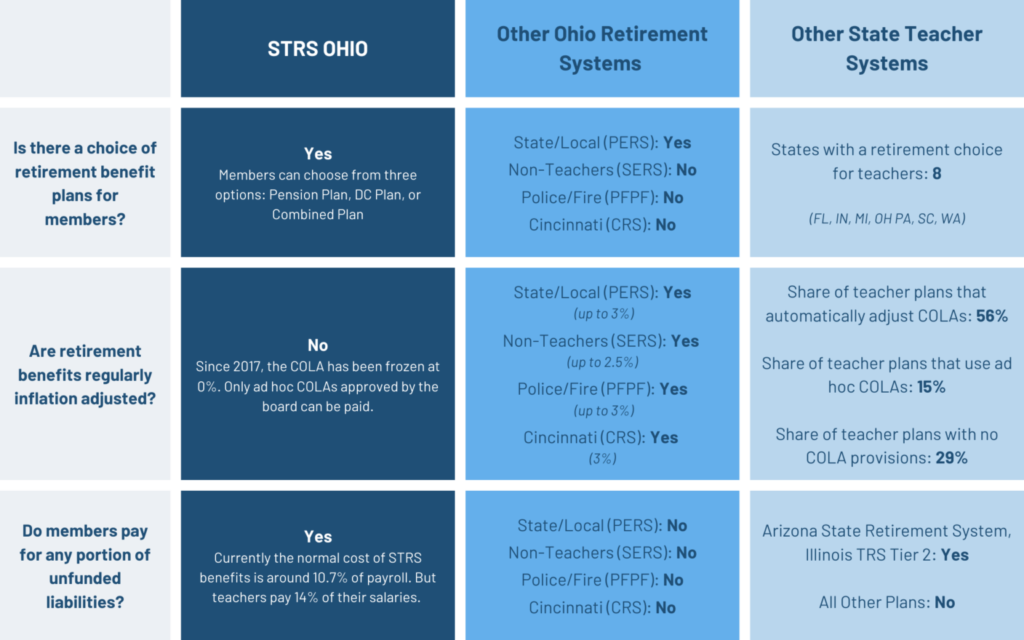

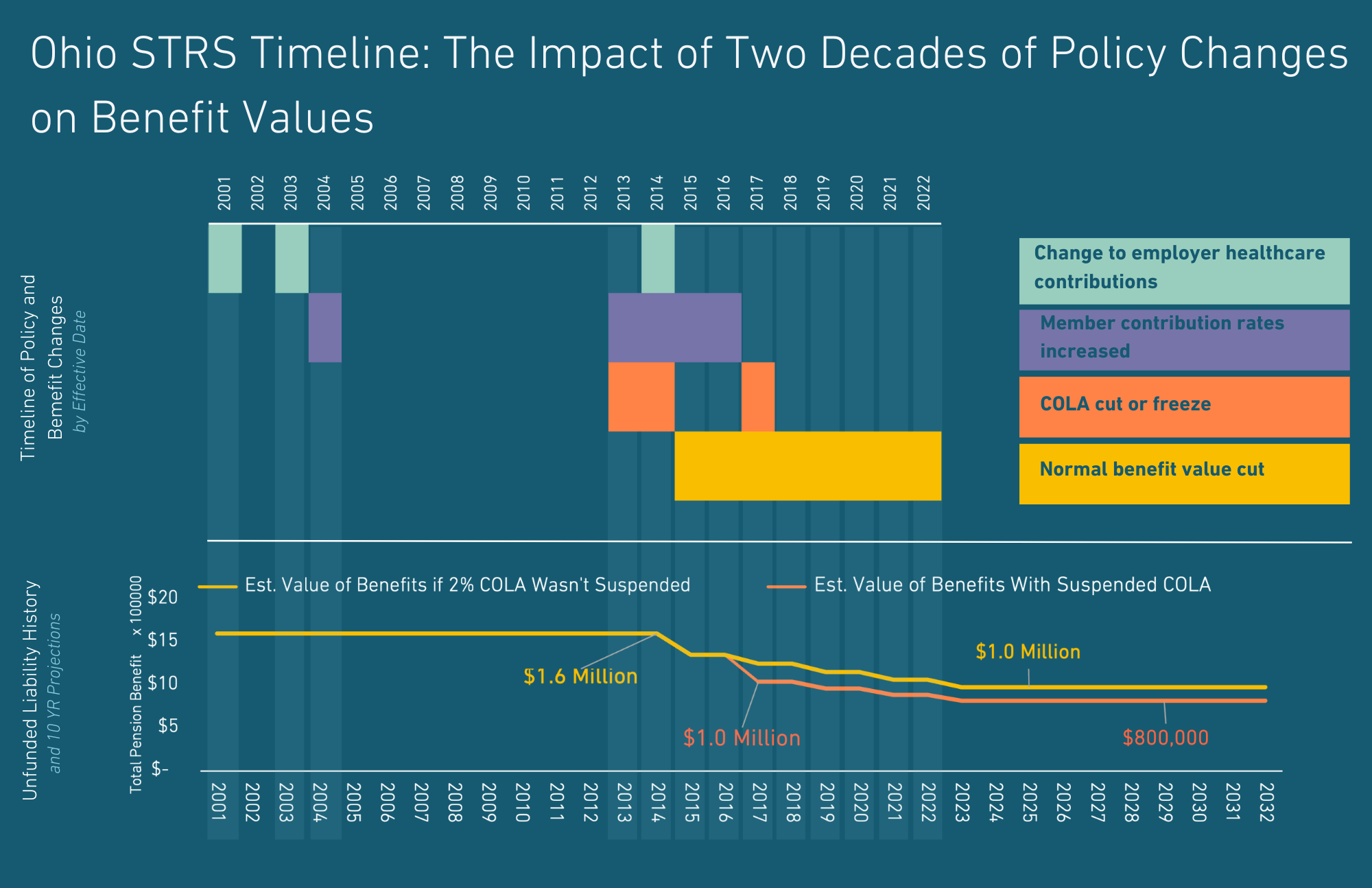

Legislation in 2012 lowered the annual COLA on retired teacher pension benefits from 3% to 2%. It also have the STRS board authority to reduce that COLA in the future. Then in 2017 the board said going forward the COLA would be 0% until funding for STRS improved.

However, political pressure and retiree protests since then have been significant. In 2022 the STRS board granted a one-time 3% COLA, and in 2023 they again granted a one-time 1% COLA to retirees. The STRS board didn't change their COLA policies though. So the reality is that while there are likely (and hopefully) going to be more COLA adjustments in the future, the timing or amounts just won't be completely known in advance.

The problem is that STRS accounting practices currently assume there won't be any more COLAs ever again. All figures for the "funding period" (how long until full funding is reached), the "funded ratio" (the current balance of the fund), and the "unfunded liability" (the current funding shortfall in dollars) are all generated under the accounting assumption that there won't be future COLAs increasing the value of benefits.

While the STRS board doesn't know exactly what COLAs it will grant, to be conservative they should direct the people measuring the value of benefits to assume at least some adjustments in the future. Doing this would "increase" the funding period as measured and mean additional contributions today are needed. But it would also be more honest and realistic.

PROMISED BENEFIT SECURITY

(CLICK TO EXPAND THE SECTIONS BELOW TO READ MORE)

Pensions are supposed to provide retirement income security. However, a fixed dollar amount paid every year isn't actually that secure if it doesn't keep up with inflation. The purchasing power of money falls over time, so at least some kind adjustments are needed.

Cost-of-living adjustments don't necessarily have to be 2% or 3%, and they don't have to happen every year.

However, unless contribution rates are increased, STRS can't provide any COLAs in the future unless its investments earn returns far above expectations to provide enough cash to pay for benefit adjustments.

PROTECT EDUCATION EQUITY

(CLICK TO EXPAND THE SECTIONS BELOW TO READ MORE)

Rising teacher pension debt costs for school district employers are regressive and pass a greater burden to high-poverty districts. Each dollar increase in retirement costs for school districts that is not balanced out with some offsetting revenue means a dollar less that is available for education programs and supports that are critical for quality education outcomes.

If the state passes on STRS Ohio contribution rate increases to school districts, that will increase employment costs. Raising pay for teachers will come with even higher benefit costs than under the status quo. And this will put budgetary pressure on school districts to fight back on salary improvements for educators.

In general, wealthier communities can afford to pay teachers higher salaries. Often, high-income communities are better at retaining quality teachers for a long-term period of time. And the two key drivers of valuable pension benefits are salary and tenure. Which means that wealthy communities typically employ teachers who earn the largest pension benefits.

This is not a problem with pension benefits specifically. The same dynamic exists for the STRS Ohio "Defined Contribution Plan, "and the "Combined Plan."

The problem is that even though certain communities are responsible for a higher share of promised benefits and unfunded liabilities, contributions into STRS are paid on an equal basis as a percentage of payroll. This might make sense from the perspective of the retirement system, but it creates budget pressures in low-revenue communities that exacerbate existing inequities.

What is the Additional Money For? Pension Debt.

The annual cost of pension benefits for active Ohio teachers enrolled in STRS is around 11% of their salaries. But teachers pay 14% of their pay into the pension plan, meaning part of their contributions are used to pay pension debt. This also means all employer contributions are for pension debt. Therefore any increases employer contributions would be for paying off additional pension debt.

Who Should Pay for Increased Costs?

While Ohio has done a lot of work over the past decade to get more money into STRS, there remains a considerable amount of pension debt. Some of this funding shortfall is acknowledged by STRS in their report, and some of it needs to be accounted for by improving actuarial assumptions. (Click here for a technical breakdown.) The main policy question is whether school district employers should be required to pay increased pension debt costs when they don't have any meaningful policy influence in how and why that pension debt has accumulated. If school districts shouldn't bear the burden of these increased costs, is it feasible to tap other existing sources?

Based on Ohio's current funding model and the legal landscape there are four primary funding sources to generate additional revenue:

School Districts?

The policies that have led to more than $20 billion in pension debt are totally outside the control of school districts. Passing the cost increases on to schools could lead to reduced programs, less money for teacher pay, or other budget cuts. And schools in economically disadvantaged areas could face the largest harm. (See here for analysis on the equity implications of increasing school district contribution rates.)

Members?

They've seen their contributions increase from 10% of pay to 14% of pay over the past decade as part of changes adopted in 2012. That already puts them at one of the highest contribution rates in the country for teachers.

Retirees?

The legislature has authorized the STRS board to reduce cost-of-living adjustments to 0%, which has been policy in 2017. There isn't anything there left to cut.

Future Members?

A new, less valuable benefit could be created. But it couldn't create significant, near-term cost savings that address the current pension debt.

If the state is going to take on the necessary increased costs for STRS Ohio, what options are there for accomplishing this goal?

The state could use the general fund to pay for all STRS pension debt costs that are above the current 14% of payroll contribution rate.

There are 33 states where the general fund is used to cover all or a portion of retirement costs as a non-employer contributor. A few examples include California, Illinois, Kansas, Minnesota, Nebraska, and Texas.

The state could tap the rainy day fund to pay for the first few years of increased STRS pension debt costs. While it is fiscally responsible to build up a safety net, it is fiscally irresponsible to allow debt to accumulate and then pass increased debt costs on to schools.

Early in 2023, Ohio transferred funds into its "Budget Stabilization Fund," raising the value of its rainy day fund to $3.5 billion, with Gov. DeWine noting this was "sound budgeting." While rainy day funds are important fiscal tools, part of their value is in using the money when it is critically important.

The state could increase revenues with a specific goal of using the extra funds to pay for any increased STRS pension debt costs.

There are various portions of the tax code that could be tweaked to generate the appropriate additional dollars for offsetting increased STRS Ohio retirement costs.

School districts could be required to pay increased costs directly to STRS, but the state would either pre-appropriate or reimburse them for the contributions that they pay above 14% of payroll (the current rate).

In states that cover some share of teacher retirement costs, most send money directly to the retirement system. However, a few states the legislation proactively appropriates a pension cost reimbursement to each district — for example, in Michigan about a third of teacher pension cost are pre-appropriated in a special line item of the state budget each year. And in at least one other state (Pennsylvania), districts pay actuarially determined pension contributions each year and then apply for a partial reimbursement (in PA it is roughly 50%) of those costs after the fact.

Ultimately, Ohio's policymakers need to consider the pros and cons of any decision on how to handle increased pension debt costs.

The Reason Why STRS OH Needs Increased Contributions

There is a general consensus that STRS Ohio needs additional funding. But there are a few different perspectives and reasons why this is the case.

Additional contributions are needed for the STRS board to partially or completely restore cost-of-living adjustments, adopt a more conservative assumed rate of return on investments, improve the accounting accuracy of future COLA benefits, and/or to take less investment risk with money for retired teacher benefits. Some stakeholders think all of these matters should be addressed, while others only think one or two should be a priority. So while it is clear that additional contributions into STRS Ohio are necessary, there are still decisions that need to be made on exactly how much in additional funding is required.

Why does STRS Ohio say it needs additional funding?

Formally, STRS Ohio's leadership are indicating that additional contributions would help them to improve benefits by restoring at least a part of the COLAs that have been frozen since 2017. Informally, some of STRS Ohio trustees appear to be interested in adopting different actuarial assumptions, and the request for funding increases now may help to absorb the cost increases associated with such assumption changes.

In September 2023, the executive director of STRS Ohio began lobbying the state legislature to increase contribution rates by 0.5% of payroll per year over eight years. This would take the school district contribution rate from 14% of payroll to 18% of payroll. The reported reason why STRS staff leadership is asking for more money is to have some flexibility to increase retirement benefits, such as partially restoring a COLA.

During an October 2023 board meeting, several STRS board members reflected concern with existing actuarial assumptions about investments and the reliability of the current investment portfolio.

During a November 2023 board meeting, STRS trustees were presented with actuarial analysis reviewing a series of options for adjusting employer and employee contributions, COLAs, and retirement eligibility rules. It is anticipated that during the spring of 2024 (February thru April), actuaries will further help STRS trustees work through a review of economic assumptions and the budgetary costs of issuing another COLA.

Is this funding need a result of recent STRS Ohio board debates?

Over the last few years there have been several controversies related to STRS Ohio management. Retirees have criticized the board for paying bonuses to investment staff even during periods of underperformance or when COLAs aren't being paid to teachers. A retiree watchdog group commissioned a report contending that COLAs could have been paid but for excessive investment fees. A board member removed by the governor has since filed a lawsuit asking to be reinstated. The executive director of STRS has been placed on administrative leave related to complaints filed with HR. However, none of these points of contention are reasons why STRS Ohio needs additional contributions from the state legislature.

Reasonable minds can debate the merits of the policies that STRS Ohio's board has adopted related to paying investment bonuses, but the dollars at stake in that matter are miniscule related to the total additional money needed. The state auditor issued a report largely pushing back on the complains of the STRS Ohio retiree watchdog, but even if STRS did pay excessive fees the amounts also aren't anywhere close to what's needed.

All of these administrative matters for STRS Ohio are concurrent with the need for additional contributions, but not factors driving this necessity.

What does Equable Institute's analysis show as reasons for additional funding?

Ohio State Teachers Retirement System unfunded liabilities did not meaningfully improve from 2022 to 2023. Actuaries for STRS Ohio report there are around $20 billion in unfunded liabilities, depending on how assets are measured.[1] And unfunded liabilities are likely even higher than that, using different actuarial assumptions. So when thinking about why more or less money might be needed for a retirement system like STRS, there are three key questions to ask:

- Are the contributions flowing into the pension fund equal to or greater than actuarially determined contribution rates?

- Are the actuarial assumptions used to determine those contribution requirements reasonable and accurate? (E.g., is the investment assumption reasonable? Are updated mortality tables being used? Are payroll projections realistic? Are future potential COLAs being accounted for properly?)

- What are the specific sources of existing unfunded liabilities?

Here is a breakdown of each of those questions:

Fortunately, the current contribution rates going into STRS are actually larger than the actuarially determined employer contribution (ADEC) —

- Actuarially determined contribution rate for the 2022-23 fiscal year: 20.65% of payroll

- This is comprised of a 10.61% normal cost rate for pension benefits and 10.04% unfunded liability amortization rate.

- Actual 2022-23 contributions: 28% of payroll

- Employer contributions from school districts (statutorily directed): 14% of payrollMember contribution rate (to the "Pension Plan"): 14% of salary

Because members pay 14% of payroll, the "ADEC" is formally just 6.65% of payroll — less than what they actually pay today.

However, the ADEC is based on a whole series of assumptions about payroll, mortality, inflation, and more. Two key assumptions that the ADEC is based on include the following:

- 7% average annual investment return over the next several decade

- There will be no COLAs paid to retirees indefinitely.

Neither of these is a particularly reasonable assumption, from Equable's perspective.

The assumed rate of return is the most important actuarial assumption any pension board makes. This drives a measurement of liabilities and unfunded liabilities, which in turn determine actuarial contribution rates. In the case of STRS Ohio, the assumed rate of return also influences the measurement of the "funding period" (how long until 100% funded). So selecting an assumed rate of return that is reasonable is critical for ensuring proper accounting of STRS promised benefits and funded status.

In March 2023, investment advisors for STRS Ohio (Callan) provided a report showing projected returns for the STRS investment portfolio. Based on their estimates there is at least a 3 in 4 chance (e.g. 75% probability) of earning at least 4.3% returns over the next decade, and a 1 in 2 chance (e.g. a 50% probability) of earning at least 7.2% returns over the next 10 years. Based on this information, the actuary advisors for STRS told trustees that they thought a 7% assumed rate return is reasonable.

However, there are three ways that Equable believes this is an overstated position.

First, a 50/50 chance of earning any investment return is a relatively risky proposition. That is effectively a coin flip's chances. If STRS does make this return, then great. But if they don't, its teachers, school districts, students, and taxpayers that all have to deal with the consequences. Even though STRS is a long-term investor, taxpayers, schools, and their students do not all exist in perpetuity. Costs going up for school districts today because of investment returns that underperform in the short-term could affect students today; retired teachers dealing with inflation today because of pension debt are not going to be satisfied knowing that in three or four decades the average investment performance of STRS could be leveled out. Therefore, it would be more reasonable to select an investment assumption with a greater probability of success so that there is less downside risk.

Second, the underlying asset projections used by Callan may be optimistic. While the underlying work is likely honest analysis, there is always the risk of bias in wanting to maintain their contracted services. And this could lead to choosing more optimistic worldview. An independent investment advisory firm called Horizon surveyed dozens of other capital market forecasters and grouped their outlooks into "conservative," "average," and "optimistic" forecasts.

Looking at a typical pension fund portfolio (that is structured similar to STRS), the Horizon survey's average forecast thinks there is a 1 in 2 chance (50% probability) of earning a 6.9% return over the next decade, and the more conservative forecasters project a 5.4% return over the next 10-years. These figures are all shown in the two images below.

The key takeaway is that a conservative forecast of a portfolio similar to STRS is between 5% and 6% returns over the next decade. STRS Ohio might generate above average returns and feel confident that it could hit 7% — but such confidence and use of potentially generous asset forecasts doesn't make the use of a 7% assumed rate of return reasonable.

Finally, the use of a 7% assumed rate of return is also above average with respect to the rest of the country's public pension plans. There is some variance in how other state teacher pension plans invest their money, and different state demographic and economic profiles can lead to different levels of risk tolerance. So some variance in assumed rates of return is warranted. As of fiscal year 2023, the average assumed return for the largest pension funds in the U.S. is 6.9% and trending down. Based on what other states are likely to do with their investment assumptions, it is likely the average will fall to 6.8% by next year, and continue gradually declining. The largest pension fund in the U.S. (CalPERS) has been told by its investment advisors that it would be reasonable to assume a 6% investment return over the next decade. The third largest pension fund in the U.S. (New York Common Fund) dropped its assumed return to 5.9%.

Around the financial crisis of 2008, the common consensus was that 8% investment assumptions were reasonable. Turns out that was wrong. Over the decade that followed investment targets of 7.5% and then 7% were viewed as reasonable. But that common wisdom has changed now too. The general trend is toward seeing 6.5% and 6% assumed rates of return as the general sweet spot for public pension fund portfolios — particularly given the volatility in global financial markets today and falling returns for private equity and real estate asset classes.

All together — the need to avoid downside risk associated with missing investment assumptions, the potentially optimistic worldview of STRS's investment and actuarial advisors, and general market trends that are moving other similar state pension funds — this evidence points toward maintaining a 7% investment assumption as being less than reasonable, and adopting something 50bp to 100bps lower as better policy from the STRS board.

The formal policy of the STRS Ohio board, as of 2017, is that all COLAs for retirees are frozen at zero unless the board decides that paying a cost-of-living adjustment won't undermine the solvency of the pension fund. Informally, the board of trustees has said that this policy will be in place until the funded status of STRS improves, though there is no specific policy timeline. As a result, it appears from notes in the STRS valuation reports that actuaries are assuming zero COLAs will be paid in the future.

However, Equable believes this is unrealistic and unreasonable on two grounds.

First, at some point in the future COLAs will be paid out again, based on informal comments from trustees at STRS board meetings. For example, if the pension fund reached a 100% funded ratio, the STRS board may vote to restore a 3% annual COLA. Of course that would then raise the value of liabilities, so, all else equal, such a policy would mean the plan is no longer 100% funded.

Second, STRS has granted two COLAs in the last two years based on demands from retired teachers, the realities of inflation, and the availability of money from 2021's strong investment returns. It is very plausible to believe that a combination of political pressure and STRS trustee sympathy will lead to more COLAs being paid out in the near future, even if on an ad hoc basis. (And from the perspective of retirement benefit security this would be welcome.)

Together, it is simply unreasonable to assume no future COLAs. What would be more appropriate would be for the STRS board to direct their actuaries to assume some low-level average COLA going forward even if they maintain the same 0% COLA policy. For example, it may be reasonable to expect two to four COLAs would be paid out over the next decade, averaging out to an average annual COLA of 0.75%. So actuaries could simply assume there would be a 0.75% annual COLA. In years where STRS stuck with their 0% COLA policy, then there would be an actuarial gain for STRS Ohio. In years where a COLA is paid out above that line, there would be an actuarial loss.

And, most important for the context of this analysis, using a small COLA assumption would more accurately reflect the value of future promised benefits. A more accurate measurement of liabilities would mean a more accurately defined funding period and measurement of unfunded liabilities, which in turn would lead to a more accurate actuarially determined employer contribution rate.

There are at least two other technical ways that STRS Ohio's funding policy drives the actuarially determined contribution rate (we don't provide a detailed analysis of these points in this format, but can provide more details upon request).

First, any unfunded liabilities accrued are amortized over a closed 30-year period beginning in 2015. It would be more appropriate to use a "layered bases" approach that amortizes each new year's change to unfunded liabilities over a 15-years or less period of time.

Second, STRS Ohio is using 2014 mortality tables that are adjusted to the present. It would be more appropriate to use updated mortality tables as starting points with whatever adjustments are appropriate to the STRS specific context.

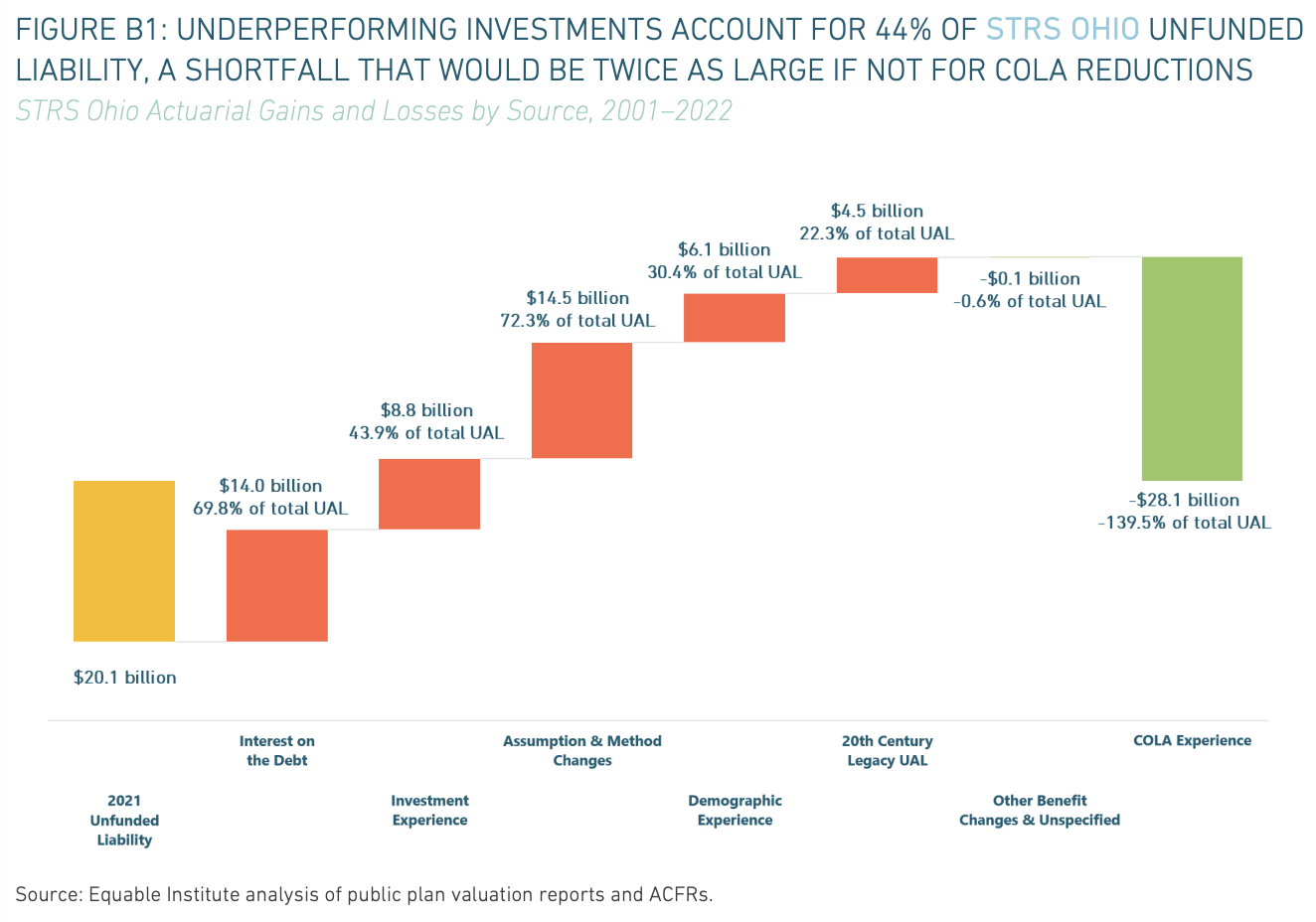

The figure above shows data compiled from STRS Ohio reports going back to 2001. Every year actuaries report the specific reasons that unfunded liabilities increase or decrease. There are dozens of reasons why unfunded liability levels could change from year to year, but they fit into seven general categories, as show in the figure above. (For example, liabilities change each year based on actual payroll change, actual mortality, actual disability claims, actual numbers of new hires or retirees, etc. All of these are totaled up into a single "Demographic Experience" category. Please contact us if you'd like the raw data behind these calculations. The figure was originally published in a January 2023 Equable Institute paper, available here.)

The far left yellow column shows the fiscal year 2022 unfunded liability based on actuarial value of assets, reported in a Ohio STRS valuation report. (The same data has not yet been published for fiscal year 2023 as of November.)

Each of the red columns show increases in the unfunded liability. The green column shows a decrease in unfunded liability. Added together all of the red and green columns equal the yellow column:

- STRS Ohio started the year 2000 with $4.5 billion in actuarially valued unfunded liabilities. (This is shown in the column third from the right.) This means roughly 20% of the current unfunded liability is related to experience and policy decisions made in the 20th century.

- For many years Ohio state statutes did not require STRS Ohio employers to make contributions sufficient to cover the actuarially determined contribution rates for benefits. And even in the year where the state legislature did authorize enough, those contributions weren't always enough to match interest accruing on the underlying pension debt. The net effect over two decades has been $14.0 billion of growth in the STRS Ohio funding shortfall from expected "interest on the pension debt." (This is shown in the column second from the left.) Notably, in recent years this category has not been increasing.

- Between 2001 and 2022, there were good years and bad years of investment returns, but all added together there was enough underperformance to add $8.8 billion to the STRS Ohio unfunded liability. This is not to say Ohio has experienced large investment losses or is it even making an argument they've made bad investments. Rather, actual investment returns have underperformed actuarial assumptions. Put another way, the average STRS Ohio investment return wasn't good enough to effectively hit their assumed rate of return. Until 2012, STRS Ohio was assuming it could earn an 8% return on investments. They lowered that target slightly to 7.75% for five years and then lowered it again to 7.45% in 2017. None of these were particularly realistic targets.

- The STRS Ohio board has attempted to adapt and keep up with changes to investment climates and demographic patterns. These changes to actuarial assumptions have somewhat improved accuracy, but they have also meant recognizing an additional $14.5 billion in pension debt that wasn't accounted for under previous actuarial assumptions.

- Actuaries did not always consistently properly estimate changes to future demographic patterns like mortality or retirement rates, and this led to $6.1 billion in additional unfunded liability increases.

- But . . . the total unfunded liability would be a lot higher if the legislature had not reduced the cost-of-living adjustment for retirees in 2012 legislation, or if the STRS Ohio board had not further reduced the COLA to 0% in 2017. These combined changes created an "actuarial gain" of $28.1 billion — which means that the unfunded liability today is around $28 billion lower than it would have been without these cuts to benefits.

If the assumed rate of return were reduced, that would cause the category "Assumption & Methods Changes" to increase. (This column is fourth from the left.) If a small annual COLA assumption were added, even keeping the formal policy of 0% COLAs in place, that would reduce the "savings" shown in the green column on the right. Together, those would reflect a $10 billion or $20 billion increase in the yellow column on the left — the unfunded liability.

So what has caused unfunded liabilities in STRS Ohio? The biggest factor was a history of not fully funding STRS Ohio meant interest accruing on the debt. Fortunately, that isn't as much of a problem under existing funding policy. Underperforming investments have been a problem going back to 2001, and that could continue to be the case going forward without a reduction in the assumed rate of return.

Most notably, though, a major reason why STRS Ohio unfunded liabilities aren’t larger — and thus why their funding period isn’t longer — is the elimination of COLAs. If that policy were reversed, the funded status of the Ohio State Teacher Retirement System would look much worse.

[1] Actuaries contracted by the Ohio State Teachers Retirement System reported to STRS trustees in an October 2023 meeting that unfunded liabilities as of June 30, 2023 are: (a) $20.2 billion based on actuarially valued assets (e.g., using a five-year phase-in of any given year's investments gains and losses); or (b) $22 billion based on market valued assets (e.g., using the market-based prices for certain assets like stocks and the valuation-based prices for other assets like private equity and real estate). These numbers are not meaningfully changed from fiscal year 2022.

Conclusion: Why more money is needed

Equable's analysis finds that the assumed rate of return and assumed 0% COLA are both unreasonable. The STRS Ohio board should adopt different assumptions for each, and in doing so this will raise the value of liabilities.

Raising the value of liabilities will mean a longer funding period than the current 11.2 years reported, and it would mean a higher unfunded liability.

For context, a 2022 report for STRS Ohio estimated that if the assumed rate of return were lowered from 7% to 6%, would increase unfunded liabilities from around $20 billion to around $30 billion.

Adding the COLA assumption back in would only build on this. When the COLA was cut from 2% to 0% in 2017, this removed more than $20 billion in liabilities from the STRS Ohio books. And that was based on an even higher assumed rate of return. Adding back in the assumption of a small annual average COLA would push up liabilities too, maybe by an additional $5 billion to $10 billion (depending on the actual assumption).

Therefore, it is plausible that STRS Ohio unfunded liabilities are closer to $40 billion and not $20 billion, depending on future investment returns and COLA policies. Which would mean the funding period for STRS Ohio is closer to 20 years than 10 years. All of which will push up the actuarially determined contribution rate.

The ADC for 2022-23 as reported by STRS Ohio in their 2022 actuarial valuation was 20.65%, and that number included a 10.61% normal cost. We estimate that if a 0.75% COLA were assumed, along with a 6% assumed rate of return, that the normal cost would rise to around 15%.

In addition, adopting a more prudent assumption about COLAs and investment returns would increase the actuarially determined unfunded liability amortization payment too. This could double the current 10.04% payment toward pension debt.

Based on how investment and COLA assumptions are changed, it is easy to see how the ADC could increase to 32% or 36% of payroll for STRS Ohio. If member rates stay at 14% of payroll, this would mean increasing employer rates by 4% to 9% of payroll.

The best policy is for pension funds to receive 100% of actuarially determined contributions, which are based on reasonable assumptions and a funding policy that targets a 100% funded ratio within the next 20 years or less. And an appropriately determined contribution rate for STRS Ohio is definitely more than 28% of payroll.

In theory, a pension fund can make certain adjustments that would reduce costs while simultaneously improving its accounting practices. However, almost all cost reduction levers have been pulled with respect to STRS Ohio:

- There is no more room to adjust COLAs (other than for the state legislature to formally ban any future COLA issuances along with a budgetary requirement that any legislatively authorized COLAs come with full funding based on a low discount rate).

- There is very little savings to be gained from increasing the retirement age (the 2012 legislation already triggered a gradual increase in the normal retirement eligibility age to 65).

- There is no legal ability to cut the pension multiplier for active members and little near-term savings to do that for future members (which would also threaten their retirement security).

- There is no large near-term savings from changing the default retirement plan from the Pension Plan to the Combined Plan or Defined Contribution Plan. The reason is that the key driver of the actuarially determined contribution rate today is the unfunded liability of legacy members of STRS Ohio.

- And finally, member contribution rates have already been raised to a considerably high 14% of payroll. Technically members could be asked to pay more—but it is hard to make the argument that it would be appropriate policy.

Based on all of this, Equable concludes that:

- A. STRS Ohio needs to adjust its accounting practices, and this will require more funds to pay off unfunded liabilities,

- it would be appropriate to pay those increased contribution rates, and

- there are few options to meaningfully reduce those increases. Therefore, additional employer contribution rates into STRS Ohio are warranted. And as we've argued elsewhere, it would be best policy for the state to take on these increased costs rather than forcing school districts to pay the increased costs as an unfunded additional mandate.

Funding Equity

Passing on STRS Contribution Rate Increases to School Districts Could Result in Hidden Cuts to Education Funding

Ohio school districts haven't had to think much about pension costs. They pay some of the lowest employer contribution rates in the country: 14% of payroll is well below the roughly national average for teacher pension plans (around 20% of payroll) and significantly below neighboring states (Michigan's teacher retirement costs are over 30% of payroll, Kentucky's teacher pension costs are over 40% of payroll). Plus, Ohio school district retirement plan costs haven't changed since the 1990s.

However, changes to STRS Ohio costs are now coming sooner rather than later. It is just a matter of when, and not if, employer contribution rates are increased. And the fundamental question is whether school districts will continue to be required to pay for all employer costs or if Ohio will join 28 other states in having the state become a non-employer contributor to its teacher retirement system.

The reason this is a critical question is that any cost increases passed along to school districts without some increase in resources will become a kind of hidden education funding cut. This would be bad for all school districts, but particularly challenging for those districts in low-income communities.

Consider that there are already education resource equity challenges with the status quo:

- Pension debt costs are regressive and pass a greater burden to high-poverty districts.

In general, wealthier communities can afford to pay teachers higher salaries, as well as the corresponding higher costs of their retirement benefits. Those larger salaries mean larger pensions and a greater share of the unfunded liabilities for STRS and School Employees Retirement System of Ohio (SERS). However, the pension debt costs associated with underfunding those liabilities are shared evenly by districts — even those in areas with greater poverty and fewer resources. - Low-income communities have fewer resources to pay pension costs generally — and would be disproportionately harmed by increases in those costs.

Low-wealth districts can only generate limited resources from local property taxes. Given these limited resources, even a slight increase in pension costs can have a much higher marginal cost for low-wealth communities than more affluent ones.

Ohio public schools make employer contributions to two separate state retirement systems: STRS Ohio, which enrolls certified teachers, and SERS Ohio, which enrolls non-certified school staff.

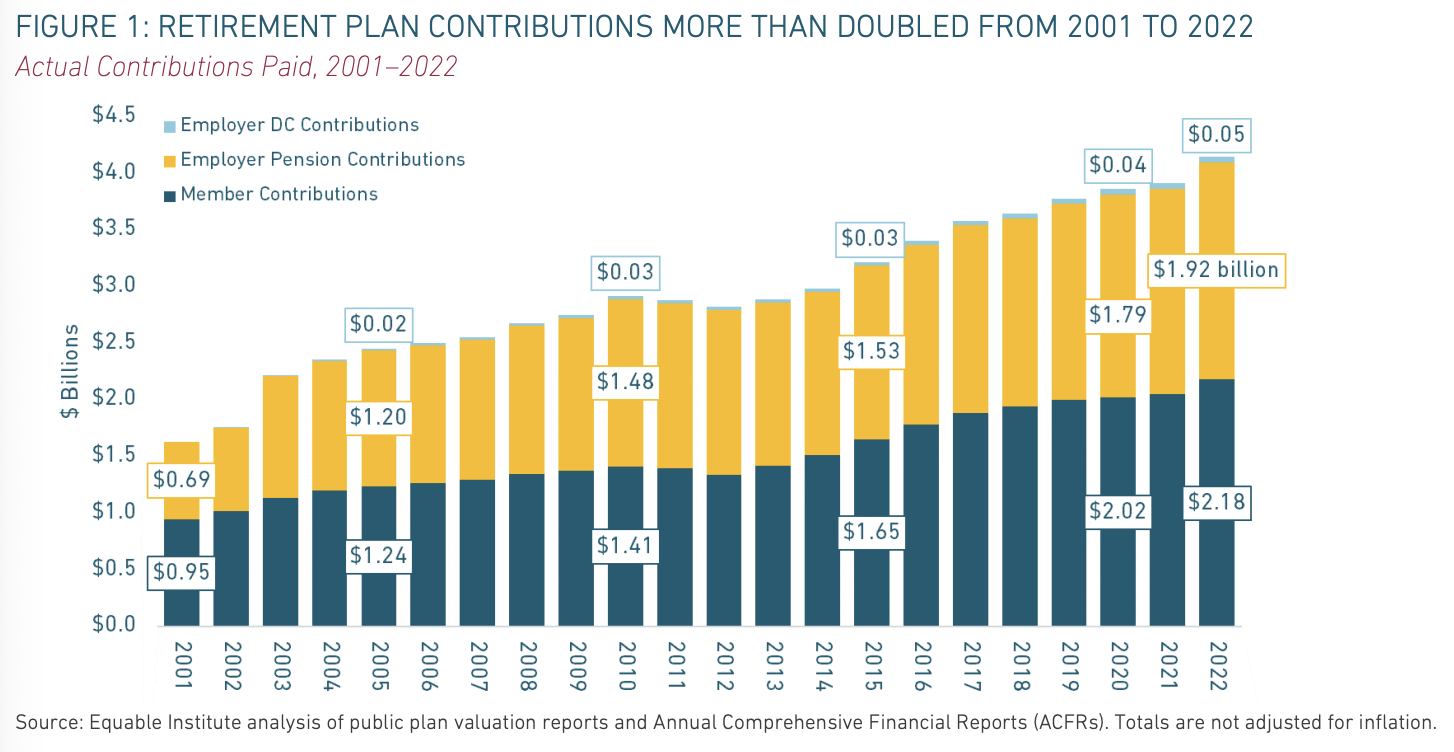

Across the two systems, $4.2 billion in 2022 was spent by school districts, the state, and employees to finance retirement benefits — a 154.1% increase from 2001. To put the 2022 expenditure number in context, it is almost 8 times the federal funding Ohio received to support economically disadvantaged students in the same year, as shown in Figure 1.

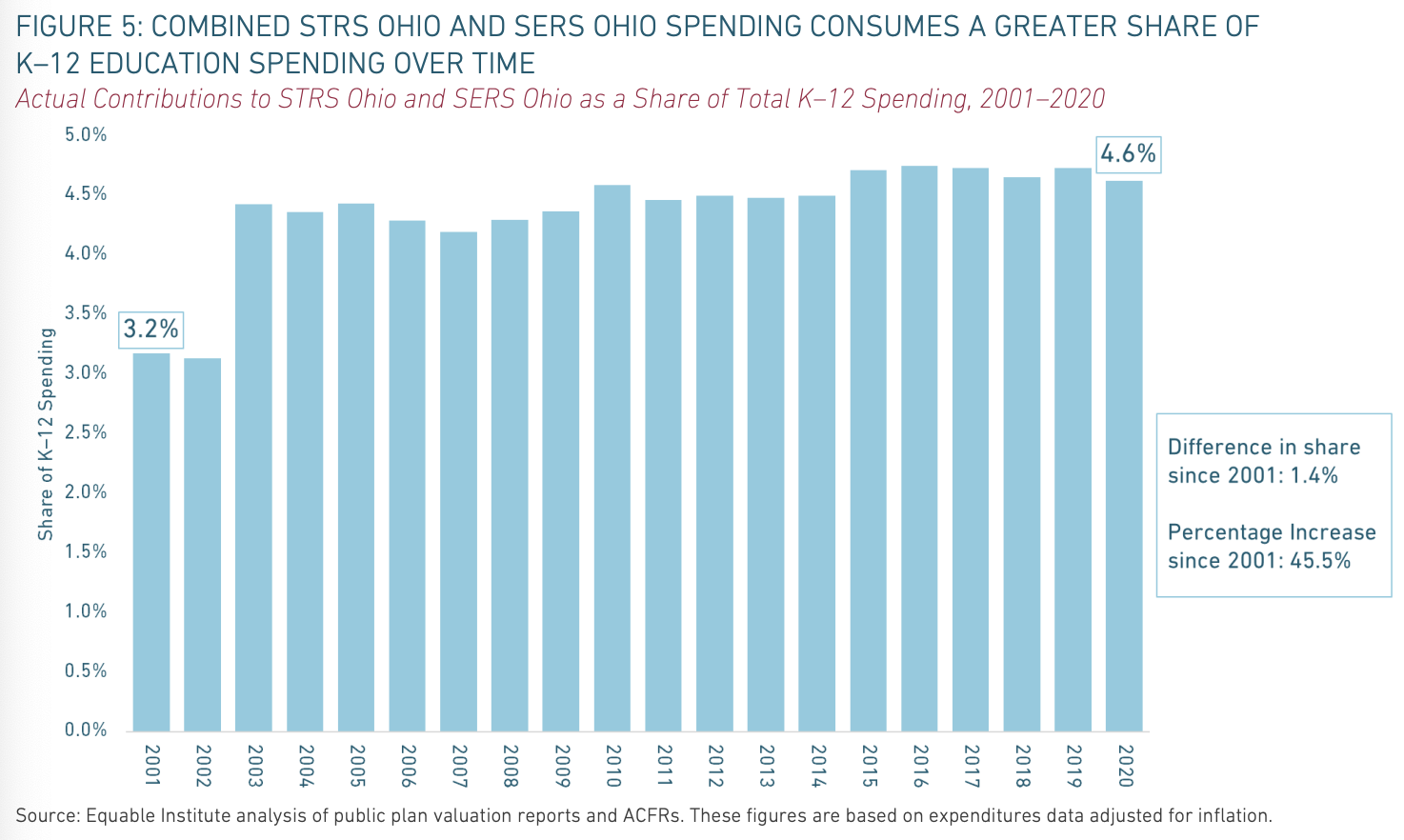

Large pension costs are not inherently a problem, but what is a problem is pension costs that are rising faster generally than K–12 funding. From 2001 to 2020, retirement spending (across both STRS Ohio and SERS Ohio) increased an average of 4.69 percentage points per year, while state and local K–12 funding rose by an average of 1.41 percentage points annually. The net effect is that an increasing share of state and local K–12 education spending has been siphoned off to cover pension costs. For example, in 2020, 4.8% of local education funding went to STRS Ohio, an 18.4% increase since 2001.

The increased spending on both the teacher retirement system and school employee pension system came from higher contribution rates for members and a larger share of employer (e.g., school districts) contributions being allocated to pension benefits.

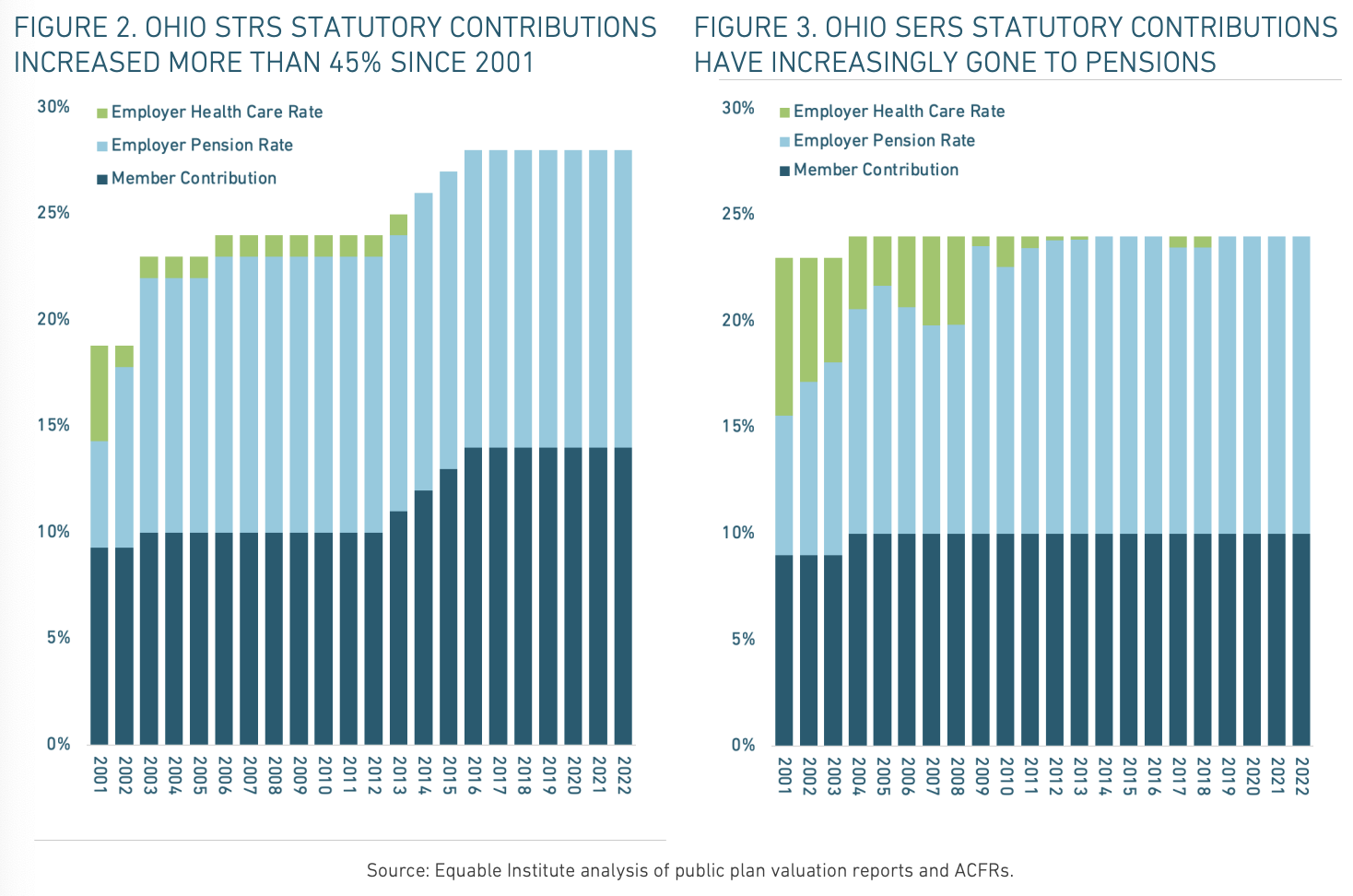

In total, spending on retirement plans went up from $1.6 billion in 2001 to $4.2 billion in 2022. The changes in contributions differed across the two retirement systems. For STRS Ohio, there were two primary changes to contributions. First, the statutory member contribution rate for pension benefits increased several times between 2001 and 2022, shown in Figure 2. Second, while the employer contribution rate remained at 14% of payroll for the last two decades, the share of that contribution being allocated to pension benefits instead of health care benefits also steadily increased — this is also shown in Figure 2.

For SERS Ohio, employers have provided the majority of increased contributions since 2001. Figure 3 shows the change in statutory member contribution rates and employer contribution rates. The figure also shows the portion of the employer contributions that was allocated to the SERS health care trust fund versus the pension trust fund.

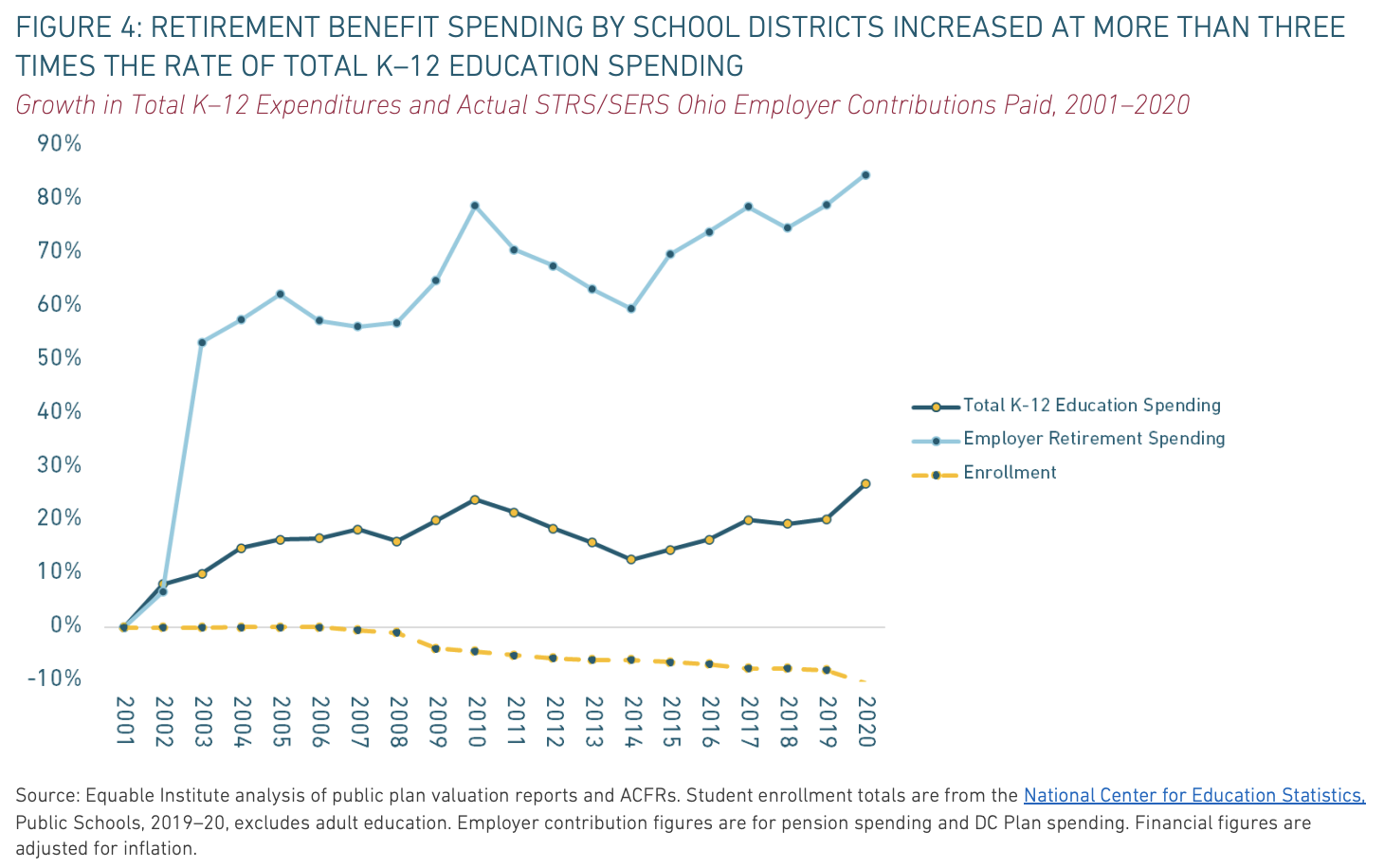

Overall, between 2001 and 2020, after adjusting for inflation, retirement plan spending across both Ohio state school retirement systems grew at more than three times the rate as total K–12 spending. Excluding the rapid increase in spending from 2001 to 2003, retirement plan expenditures grew at roughly 1.5 times the rate as K–12 spending over the same period.

The state education formula is rightly attentive to students. However, the cost of an underfunded retirement system like STRS Ohio cannot be ignored. The state does not specifically allocate K–12 funds for STRS Ohio or SERS Ohio, and it also does not provide supplemental funding to address each retirement system's unfunded liability. As a result, those costs are left for districts to figure out, and each time the cost to pay down the unfunded liability for either system rises, it can be equated to a hidden cut to the budget that districts have to provide a quality education.

School district leaders across Ohio have felt immune to changes in retirement costs because their bottom line contribution rate hasn't changed since the 1990s. Public school employers have just paid a flat 14% of payroll every year to STRS and SERS, and let state retirement systems figure out how to distribute that money. And for a while those systems were able to set aside a portion of the money for health care benefits in addition to retirement system costs.

But the retirement systems themselves weren't immune from external changes to financial markets, interest rates, and the general investment climate for pension funds. The actual costs of retirement benefits for public school teachers and staff has been steadily on rise, and the state's previous efforts to stop the growth — making members pay more and giving less to retirees — has not been sufficient. As a result, school districts are facing the probable reality of an increase in their contribution rates for the first time in decades.

Even though employer total contribution rates haven't risen in years, that doesn't mean the share of K–12 spending going to cover retirement costs hasn't been increasing (as shown in Figures 4 and 5).

Contributions to Ohio STRS, from both teachers and their employers, are based on salary. The higher a teacher's salary, the more she and her employer contribute to the fund. Given that more experienced educators earn higher salaries, this structure is designed to reward teachers who remain in the profession for their entire career. In general, wealthier communities can afford to pay teachers higher salaries, as well as the corresponding higher costs of their retirement benefits, as higher salaries result in greater STRS Ohio pension liabilities. In other words, districts that pay larger salaries are responsible for a greater share of the total pension liability at STRS Ohio. However, the pension debt costs associated with underfunding that liability are shared evenly by districts across the state through evenly distributed contribution rates. This means that economically disadvantaged communities pay at least part of the retirement costs of educators earning higher salaries in wealthier districts.[1]

This regressive effect is compounded by higher teacher turnover rates in high-poverty districts as well. This is because higher turnover districts have a lower rate of educators vesting in the system, and with more teachers leaving the district or profession, they may also have a lower rate of educators spending their highest earning years in the district. Both workforce trends lead to lower state pension investments in high-poverty districts.

There are several strategies Ohio could pursue to disrupt these patterns. For one, the state could make its own contribution to STRS Ohio to cover the burgeoning pension debt cost. This would reduce the burden on local districts and limit costs over the long term. The state could address the problem of burdening economically disadvantaged districts with more than their share of the debt cost by developing a funding structure that ties a district's share of the overall debt cost to their contribution to STRS Ohio's liability. This would reduce or eliminate the issue of low-income districts subsidizing retirement costs in wealthier ones.

Low-income communities have fewer resources to pay retirement plan costs generally — and would be disproportionately harmed by increases in those costs.

Local communities pay the entire employer contribution for STRS Ohio and SERS Ohio. This disproportionately harms lower-wealth districts, which are less able to raise additional revenues beyond state aid to offset the costs. In effect, contributions to STRS Ohio and SERS Ohio act as a flat tax and treat the teacher salaries that Ohio school districts need to pay as the same regardless of context.

This is challenging enough on its own, in the status quo context where employer contribution rates have been relatively stable for the past few decades. But should contribution rates for employers be increased in the coming years to address persistent unfunded liabilities or additional costs related to improving retiree benefits, districts with lower income would be disproportionately harmed.

For a low-wealth district that generates only limited resources from local taxes, spending an increasing amount on retirement costs — even if just an increase equivalent to 2% to 5% of payroll — has a much higher marginal cost than it does in a wealthy district generating considerable local revenues. To use an everyday example, a $100 parking fee costs a lot more to a minimum wage worker than it does to a corporate executive. In this same way, increasing district pension costs similarly burdens low-wealth communities more than it does affluent ones.

(Text from this page was adapted from "Pension Debt Challenges for Equity in Education: The Effect of Teacher Pension Debt Costs on K–12 Education Funding in Ohio," Equable Institute and Opportunity Institute, January 2023.)

Notes

[1] To be clear, the problem of shared unfunded liability costs is not the fault of districts that pay higher teacher salaries. It is the result of state policy. First, the state sets contribution rates that flow into STRS Ohio, which historically have not always been sufficient to pay actuarial determined requirements. And the board of trustees at STRS Ohio manages actuarial policies and certain aspects of benefit levels (like COLA rates), which collectively can either contribute to rising unfunded liabilities or reduce them. Districts have no control over the operation of STRS Ohio and therefore do not determine whether the system's debts increase or decrease. Second, when STRS Ohio's pension debt increases, requiring additional funding, the state doesn't appropriate supplemental funds to districts to cover any of the rising debt costs, despite being at least partially responsible for causing them through policy decisions made at the state level.

Benefit Equity

How Do Ohio Teacher Benefits Compare to Others?

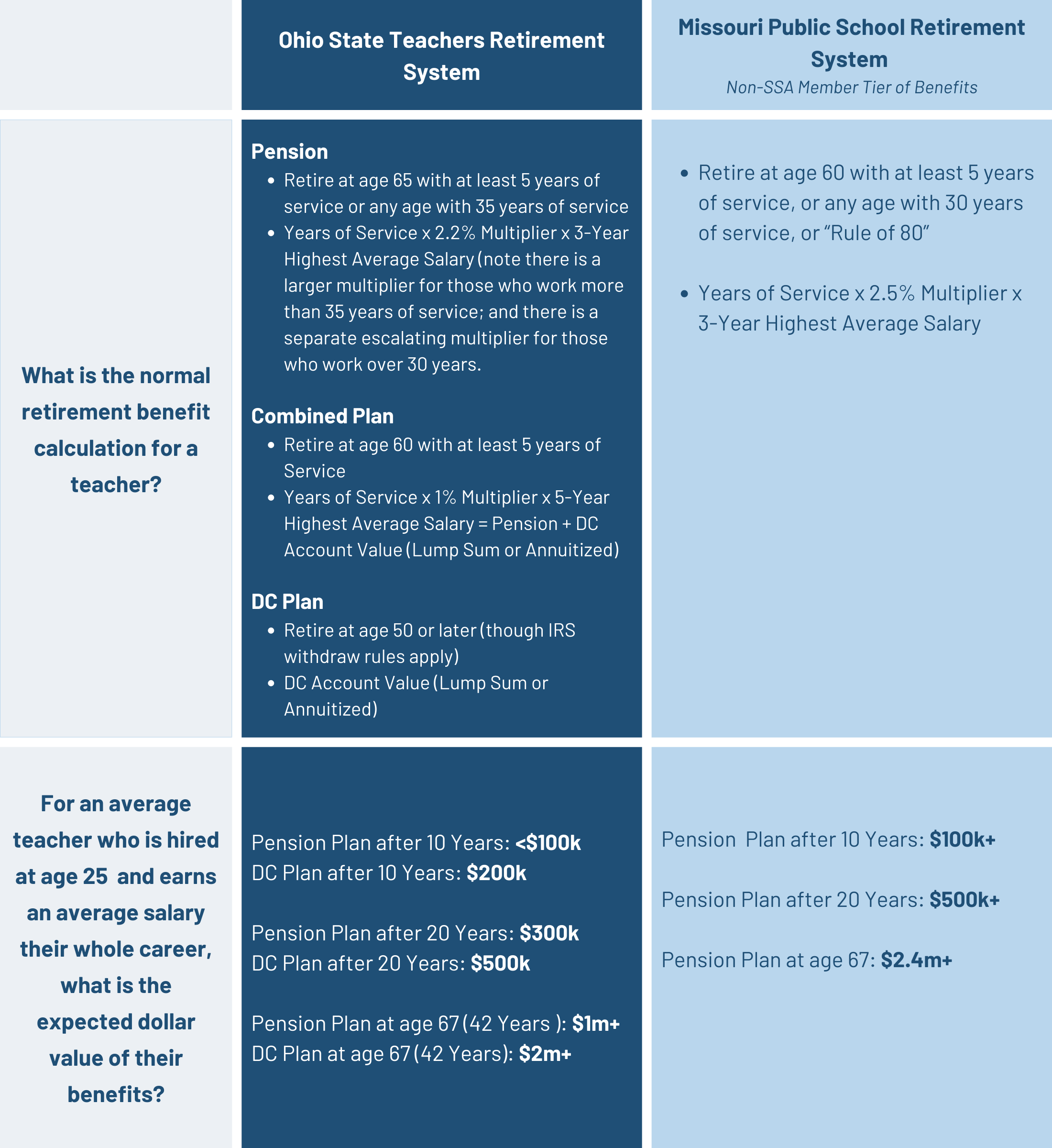

There are a range of ways that retirement benefits can be compared, including costs, values, quality, and relative generosity. In this section we approach various ways of comparing STRS benefits to others, such as other Ohio pension plans and other state teacher pension plans where the members are also not enrolled in Social Security.

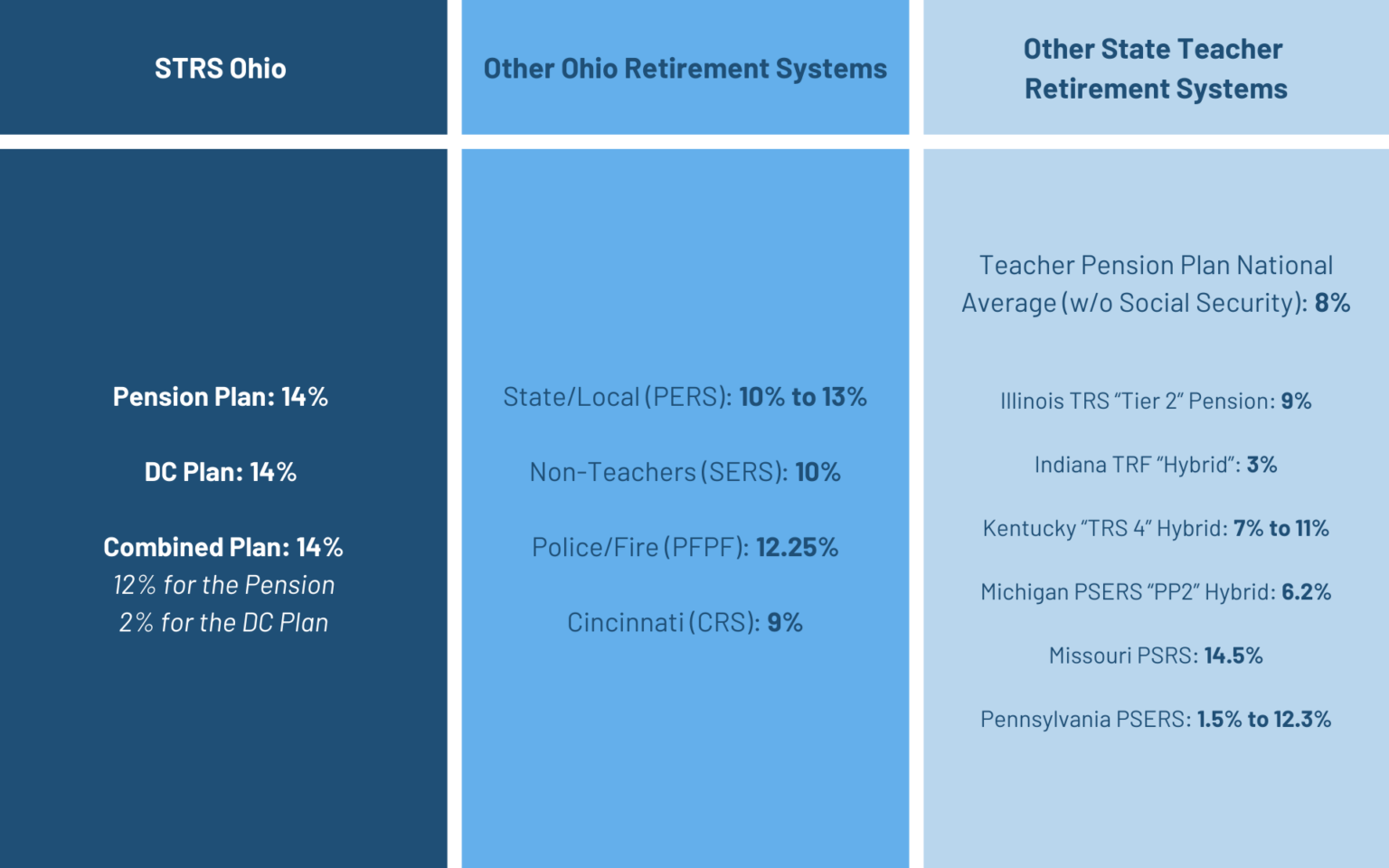

Contribution Rates as a % of salary

Note: We compared Ohio STRS to Missouri's pension plan for teachers not enrolled in Social Security, because we estimate the MO PSRS plan to be the best available to teachers not enrolled in Social Security nationwide that is also still adding new members.

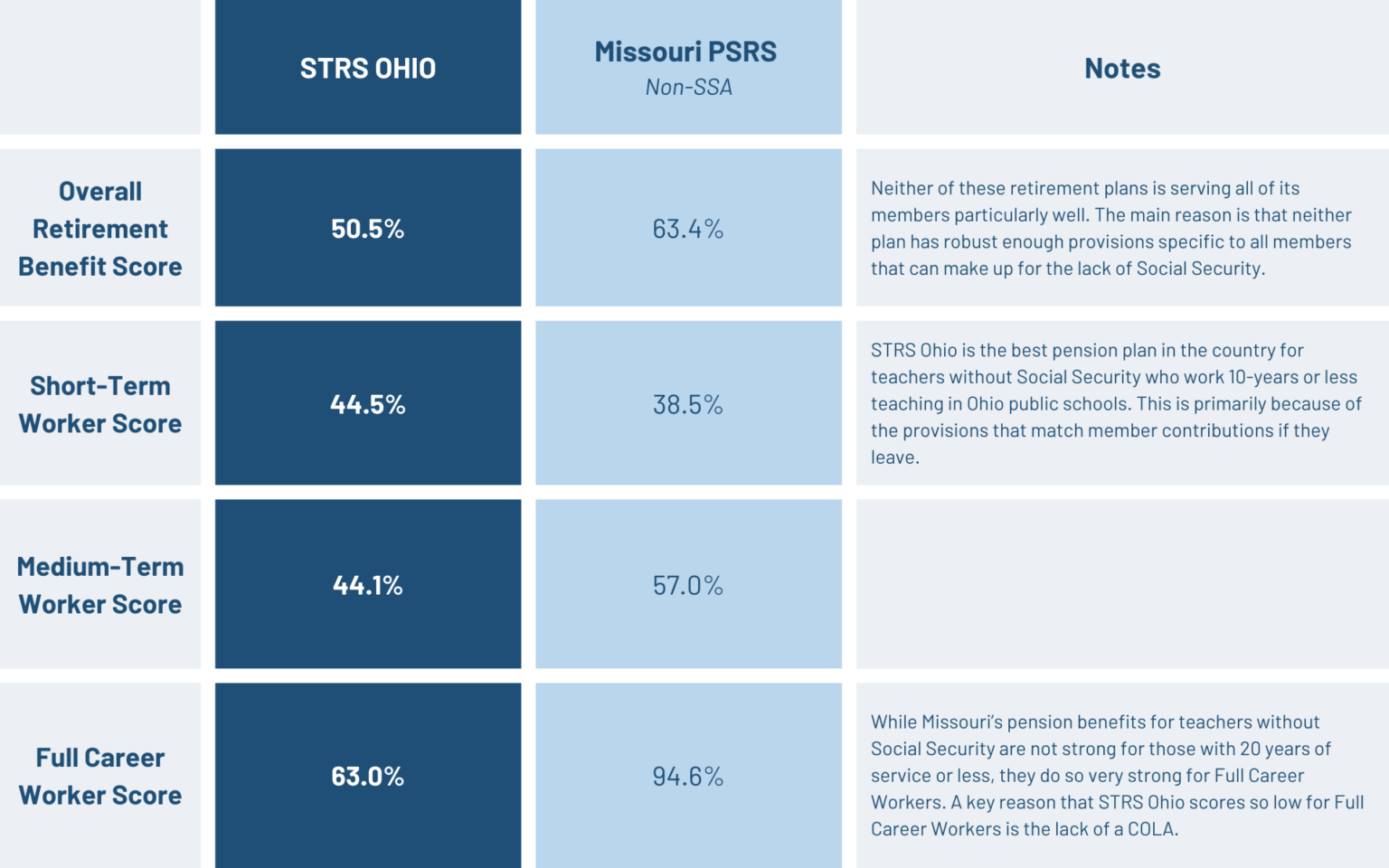

The "Retirement Security Report" is a project that grades every public retirement plan in the country on key plan provisions that relate to the value of benefits, such as benefit formula, the availability of COLAs, crediting interest rates, contribution rates, normal retirement age, and access to Social Security benefits. Each tier or class of retirement benefits is given a "Retirement Benefit Score" for three groups of employees, Short-Term Workers (STWs) who have 10 years or less of service, Medium-Term Workers (MTWs) who have 10-20 years of service, and Full Career Workers (FCWs) who work until their plan's normal retirement age or age 67. Those three scores are also combined for a composite overall score.

Note: Most teachers in the United States are enrolled in Social Security, however there are 12 states where some (GA, MO, TX) or all (CA, CO, CT, IL, LA, MA, ME, OH, NV) school districts do not enroll their teachers in Social Security. Most of these states have just one retirement plan that is open to new members. Our analysis compares STRS Ohio against the open tiers or classes of benefits in those non-Social Security states.

Note: Figures are based on market valued liabilities (or fiduciary net position)

Further Reading

More resources to help you understand the challenges facing Ohio in both local and national context.

Pension Debt Challenges for Equity in Education: The Effect of Teacher Pension Debt Costs on K–12 Education Funding in Ohio

Dive deeper into the pension debt challenge facing Ohio's K-12 budgets.

America's Hidden Education Funding Cuts

Read more about the hidden education funding cuts effecting schools across the U.S.

Ohio Pension Laws: Infographic

Learn more about the laws governing Ohio's pensions.