Tier 5 was Adopted in Mississippi. What Should Happen Next?

With $26 billion in unfunded liabilities and inadequate benefits for workers, it is undeniable that Mississippi needs to improve how it manages the Mississippi Public Employees Retirement System (PERS) and the benefits this system offers to teachers, state and local employees, and public safety across the state. But if the legislature does not act before the end of their next session, they will miss their current window of opportunity to save PERS from debilitating pension debt, inadequate benefit design, and the risk of becoming insolvent in the coming decades.

In fact, the Mississippi Legislature has already missed two opportunities to make necessary changes that fix PERS. First, in 2024, the legislature voted to increase contributions into PERS, but not up to a level sufficient to prevent interest from accumulating on the debt or to cover the costs of lowering their assumed rate of return on investments.

Then, in March 2025, the legislature ignored the need to complete their changes to contribution rates and funding policy. Instead the legislature tweaked benefit design in a way that slightly improves portability for short-term workers while stripping future career public employees of inflation protected benefits.

The new benefit design calls for a “hybrid” retirement plan that would blend a small pension with a small individual defined contribution account for each PERS member. In theory, hybrid plans can be well structured ways to create a path to retirement income security. However, the adopted Tier 5 design uses all of the funding policy rules that got PERS into its fiscal distress in the first place. The version adopted by the legislature does nothing to address the retirement system’s funding shortfall — and because the benefit terms offer no inflation protection the package as a whole would it be a net negative for workers’ benefits, according to our recent analysis.

This decision to adopt a poorly designed “Tier 5” for PERS has narrowed the timeframe in which policymakers can get Mississippi’s statewide pension fund on a road to financial sustainability. But either during a special session in 2025 or the normal spring 2026 session, the legislature could take actions that improve the benefit design structure of Tier 5 before it gets fully implemented. And at the same time the Mississippi Legislature could direct the PERS board to adopt better funding policy rules related to this new tier of benefits.

To be clear, this doesn’t mean the ideas or intent behind the legislature’s hybrid initiative are misguided. Modernizing benefit designs and improving funding policy are critical for PERS — which is among the worst funded state pension plans in the country. But it’s important to ensure that the proposed solutions to these problems actually address their root causes and ensure that they don’t reoccur in the future. And unless actions are taken in the coming months, the currently designed Tier 5 “hybrid plan” for PERS is going to be implemented that doesn’t solve PERS funding problems and makes benefits worse for career public employees.

The following is a roadmap for what additional changes are necessary in Mississippi to take advantage of this moment in order to improve PERS for all and prevent PERS pension debt from becoming a further fiscal strain on the state.

Why Mississippi PERS Needs Improvement

Mississippi PERS needs improvement for two primary reasons. The first is that PERS benefits are not adequately providing a path to retirement security for most workers. The second reason is that PERS is critically underfunded.

When it comes to retirement benefits, Mississippi PERS is not serving most workers very well. Most public employees enrolled in PERS don’t work long enough to qualify for a pension and many of those who do aren’t on a path to retirement security. In fact, more than 4 in 5 workers will receive a benefit of less than $1,800 per year. According to our analysis, only workers with more than 20 years of service are served well by the current retirement plan, and this accounts for just 10% of the workforce.

Looking at funding, Mississippi PERS faces a significant shortfall. It is currently 55.9% funded with $26 billion in unfunded liabilities as of 2024. Part of that shortfall was caused by past experience, like underperforming investments or taking too long to adopt safer actuarial assumptions. But, another part of the unfunded liability comes from a failure to ensure that large enough contributions are paid every year to cover the full principal and interest payments on PERS pension debt.

Fortunately, there are a range of proven best practices that can be integrated into the PERS legislation to ensure Mississippi accomplishes both its retirement security and funding goals. Below, we look at concrete policy steps the Mississippi legislature could take to ensure the financial health of both PERS and the state’s public workers.

What to Improve #1: Mississippi PERS Needs a Plan to Pay Down the $26 Billion Funding Shortfall Responsibly

Right now, the state is trying to keep budget costs low by prescribing a fixed amount of money to be put into PERS each year. But it is not enough money to keep PERS pension debt from growing, and the pension plan’s actuaries say that more should be paid. The most responsible way to pay down a funding shortfall is to use “actuarially” determined contribution rates that are based on a plan to get the debt paid off in 20 years or less instead of legislator-set contribution rates that are based on politics.

The hybrid plan adopted in Mississippi’s income tax bill relies lower overall retirement benefit costs and fewer future liabilities as the path to preventing future growth of unfunded liabilities. However, our research shows that benefit changes alone do very little to prevent the growth of unfunded liabilities. Without a plan to inject more money into the system to address this problem, it is likely the shortfall facing Mississippi PERS would continue to grow.

What to Improve #2: Mississippi PERS Needs to Adopt Realistic Investment Assumptions

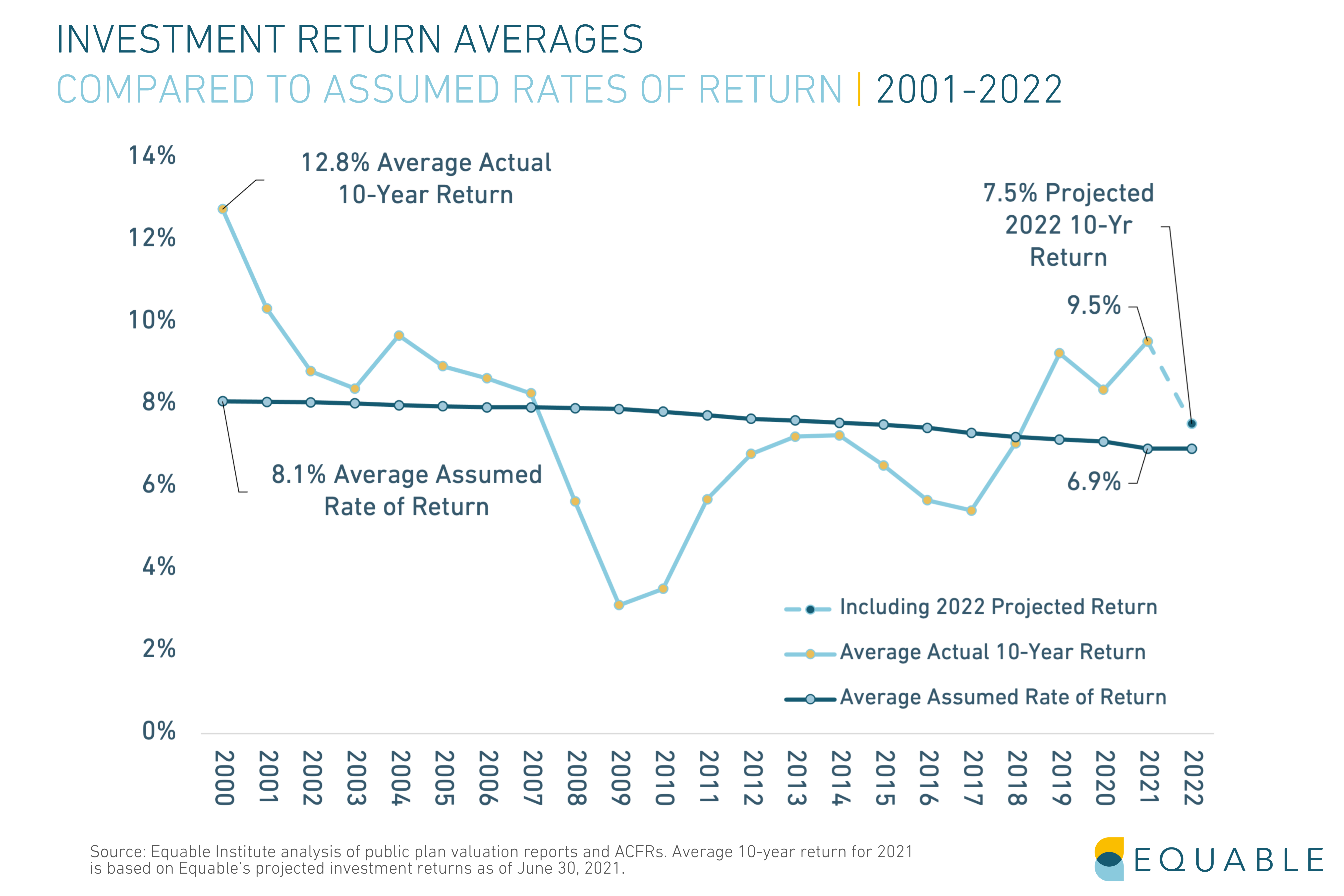

One way states determine how much they need to pay into the retirement system to prevent shortfalls from growing is by estimating how much the plan’s investments will make on a yearly basis. This is called the assumed rate of return, also known as an investment assumption.

Currently, the Mississippi legislature assumes its investments will yield a 7% return. However, there’s only a 45% likelihood they will be able to earn that much, meaning the legislature is underestimating its yearly contributions, allowing the debt to snowball.

The changes adopted this session use these same, outdated assumptions and amortization methods that got PERS into its current fiscal mess. But, if the legislature wanted to make a serious attempt at improving future funding levels, they could follow the example of Michigan which adopted a new hybrid tier of benefits that had its own 6% maximum investment assumption. All they would need to do is pass a law saying that when the PERS board implements the new Tier 5 that they have to use a rate at 6% or less.

Technically, the Mississippi PERS board could use their own authority to make this decision on their own—and they should if direction isn’t going to come from the legislature.

Without applying improvements to the new benefit tier, even the hybrid plan proposed by the Senate runs the risk of accumulating pension debt in the coming years and driving up future costs for workers and taxpayers.

What to Improve #3: The Mississippi Legislature Must Ensure that All Workers Continue to Have Inflation Protected Benefits

There have been reductions to pension benefits in the past, such as when Mississippi introduced Tier 4 to replace Tier 3. But even those benefit changes didn’t take away cost-of-living adjustments (COLA) that aim to help pension benefits keep up with inflation (this inflation adjustment is commonly referred to as the “13th check” in Mississippi). If the purchasing power of pension benefits erodes over time it’s not really guaranteed retirement security.

The plan proposed under SB2439 and adopted in Mississippi’s 2025 tax bill eliminated the COLA (i.e., 13th check) for future workers, putting the retirement security of thousands of workers in jeopardy. But the legislature can amend Tier 5 before it is implemented to restore some degree of inflation protection in the form of a COLA, even if the specific COLA rules are different from Tier 4.

What to Improve #4: Mississippi Must Ensure All Workers Have Access to a Path to Retirement Security

The simple truth is the current PERS pension plan design doesn’t work well for workers with less than 10 years of service, who account for 84% of all those enrolled in the retirement system. And the legislature’s one-size-fits-all Tier 5 hybrid would similarly fail to ensure all workers have a path to retirement income security.

Luckily, there are many ways to address this with smart and flexible retirement plan design decisions.

For example, the legislature could introduce a choice-based system that includes a plan designed for short-term workers (like a defined contribution plan) to go alongside the current Tier 5 hybrid plan. And a choice could be added such that workers in either plan design are allowed to switch once during their careers. There are more than half a dozen states with such options, including nearby Florida and South Carolina.

PERS doesn’t have to be one-size-fits-all.

The Bottom Line

Mississippi should adopt the following changes:

- Increase contributions into Mississippi PERS up to a level that is both paying at least 100% of the actuarially required contribution and is also ensuring that there is no interest accumulating on unfunded liabilities each year.

- Meeting these goals will need increasing contributions as a percentage of payroll and getting pension debt paid off faster.

- Ideally, lower the assumed rate of return for all of PERS to a number below 6.5%. But if that is not feasible then the PERS board should at the very least start the new Tier 5’s benefit portion with a lower assumed rate of return.

- When Michigan created a second hybrid plan in 2018 their legacy pension fund was using a 7.5% assumed return, but their new hybrid plan started with a 6% assumed return.

- Adjust the Tier 5 structure to add a COLA. For example, paying a COLA equal to CPI up to 3% on a compounding basis.

- Add a second retirement plan choice that has more portability, such as a defined contribution plan.

Effective reforms balance fiscal responsibility with providing a path to retirement income security for all public employees. Any solution that substantially reduces benefits for career employees, shifts virtually all costs of retirement benefits onto future workers, while eliminating inflation protection fails to maintain this essential balance. The Mississippi legislature would be doing the state a disservice if it failed to address anyone of these issues.

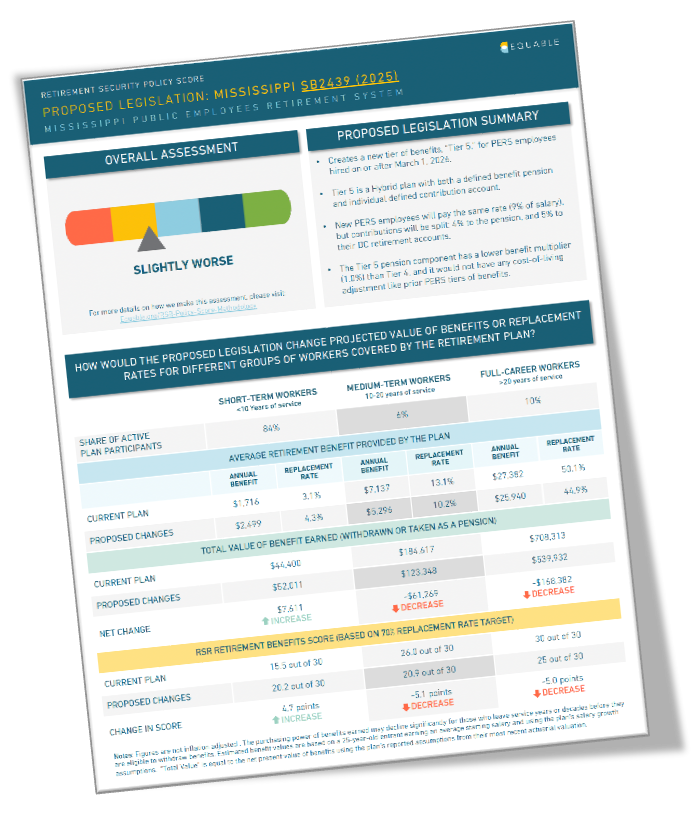

Mississippi Senate Bill 2439: Retirement Security Policy Scorecard

Mississippi is considering changes to its retirement plan provisions for the Mississippi Public Employees Retirement System (MSPERS), as presented in Senate Bill 2439. The bill, which passed the Senate in mid-February, would replace the current “Tier 4” pension plan offered by MSPERS with a “Tier 5” hybrid plan that combines a defined benefit pension and individual defined contribution account for employees hired on or after March 1, 2026.

Equable Institute has analyzed the proposed changes in Mississippi Senate Bill 2439 using Retirement Security Report methodology, finding that Tier 5 as proposed in SB2439 is slightly worse overall for workers than the currently available Tier 4 pension plan. While workers with less than 10 years of service would see modest increases to their retirement benefits, the bill would result in significant losses for the longest-tenured employees (-$168,382 on average for workers with more than 20 years of service), while also failing to address the underlying fiscal sustainability challenges facing MSPERS.

DOWNLOAD THE SCORECARD

EQUABLE INSTITUTE’S ANALYSIS OF MISSISSIPPI SENATE BILL 2439

Positive Elements of the Proposed Changes in SB2439:

- The introduction of a partial defined contribution plan makes retirement benefits more portable for members who won’t remain enrolled in PERS for their whole career. The PERS board has adopted assumptions that suggest more than 4 in 5 public workers in Mississippi work fewer than 10 years, meaning this improvement could help many future workers covered by PERS.

- The benefits for Short-Term Workers (who work 10 years or less) are more generous than those offered by the current Tier 4 pension. The annual benefit is almost 50% larger and the total benefit value is more than $7,500 higher. Because this is overwhelmingly the largest segment of PERS members, Tier 5 would be a better fit for today’s more mobile workforce.

- While the proposed benefits for Medium-Term Workers (who work 10 to 20 years) and Full-Career Workers (who work 20+ years) are less than Tier 4, they are still enough that, when combined with Social Security, they will still provide a secure retirement benefit to PERS members that replaces more than 70% of pre-retirement income.

- The costs of providing Tier 5 benefits are substantially lower than the current plan offerings, which is an important consideration for a plan that was only 55.8% funded with $26 billion in unfunded liabilities in 2023. Tier 5 would be less likely to see costs rise moving forward.

Neutral Elements of the Proposed Changes in SB2439:

- Social Security benefits are estimated to replace 50% or more of PERS employees’ salaries in retirement and, when combined with the PERS benefits, Tier 5 members can still experience total replacement rates above 90%, well above the 70% target identified by Social Security and private retirement providers.

- Tier 5 increases the service requirements for early and normal retirement (which will affect some future workers), but leaves the normal retirement age at 65 which is still lower than Social Security.

Negative Elements of the Proposed Changes in SB2439:

- The elimination of inflation protection through a COLA is a significant reduction in the value of benefits from Tier 4 to the proposed Tier 5. This reduces the total value of benefits and means retiree income will be susceptible to the decay of inflation over time.

- While the costs of Tier 5 are lower than Tier 4, nearly all of the costs will be paid for by members while the vast majority of future employer contributions to PERS will just be for paying down legacy pension debt. This effectively means future worker benefits are being lowered to make it more affordable for the state to pay for unfunded liabilities.

- Tier 5 would mean a substantial reduction in the benefits earned by Medium-Term Workers and Full Career Workers. As the table shows, total benefits would be reduced by over $60,000 for Medium-Term Workers and more than $160,000 for Full Career Workers.

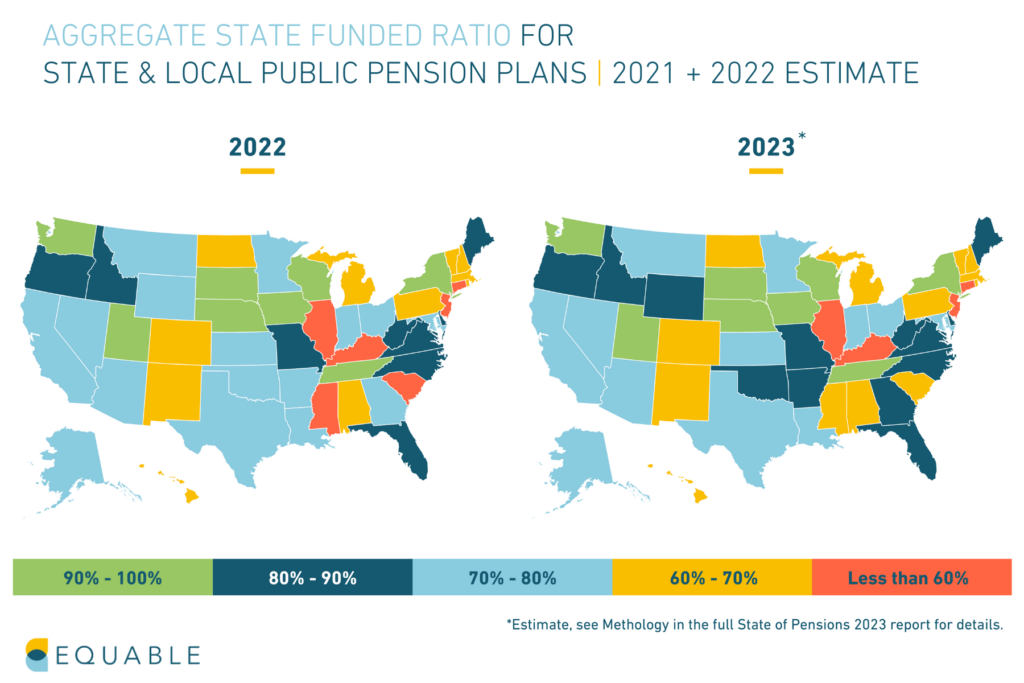

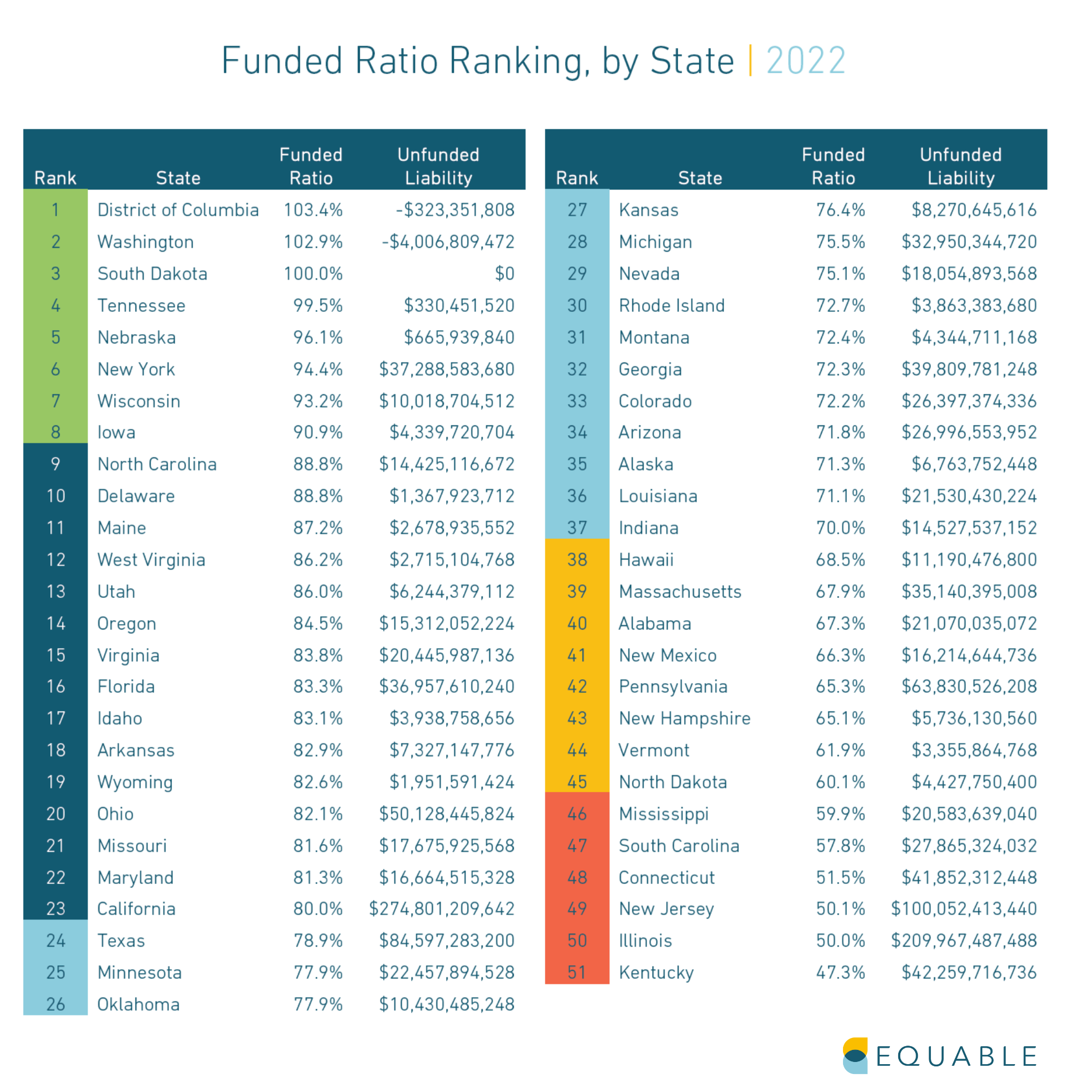

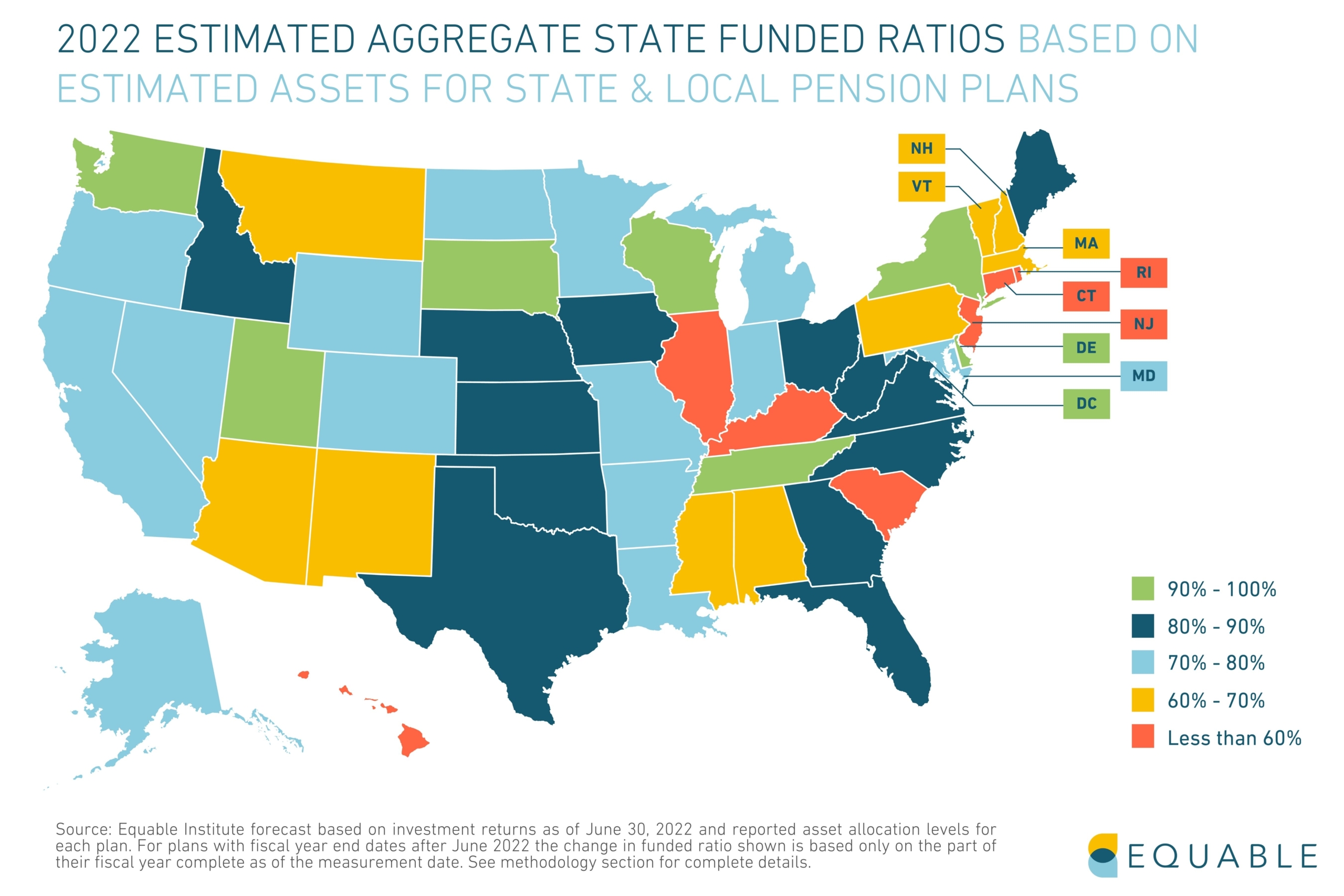

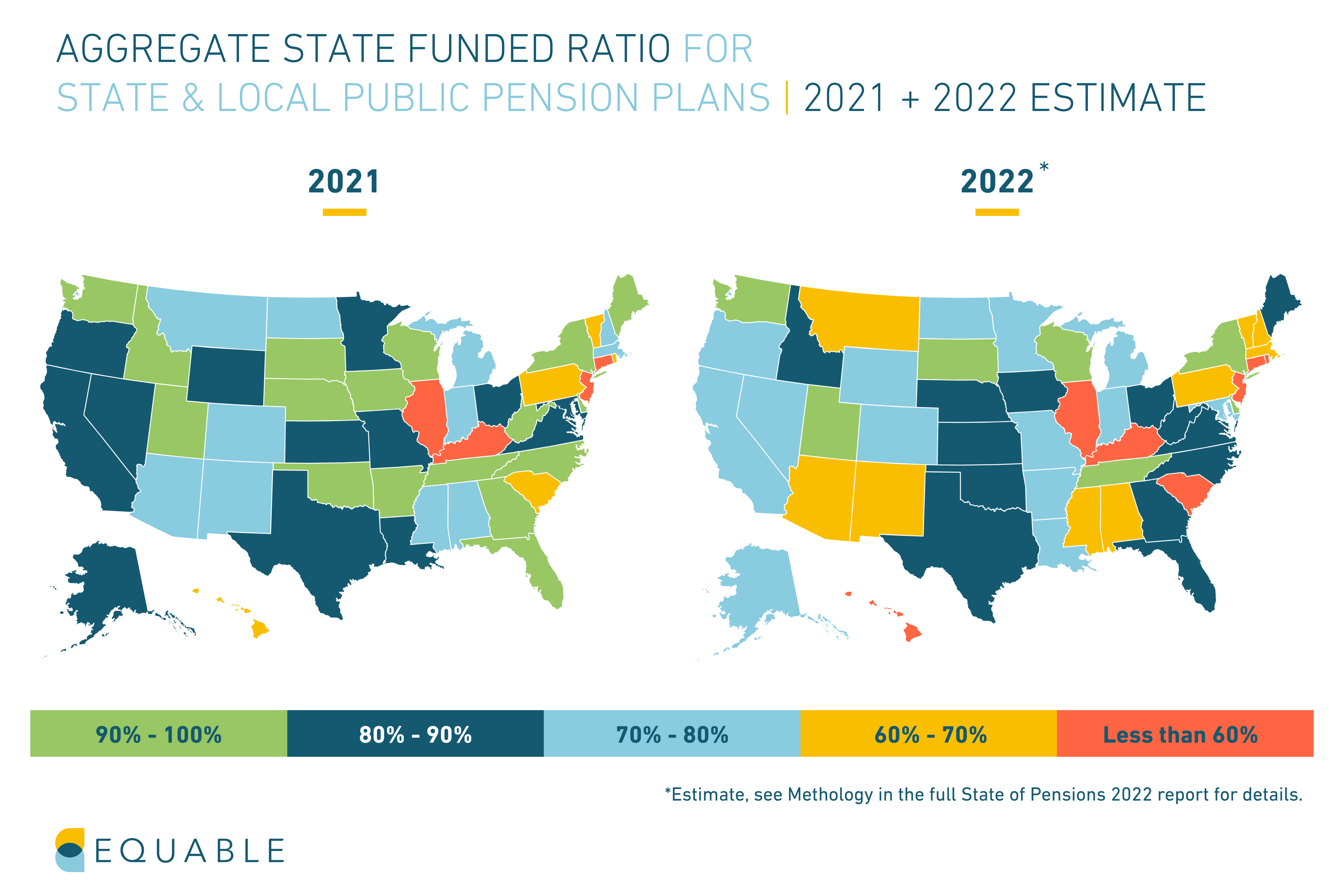

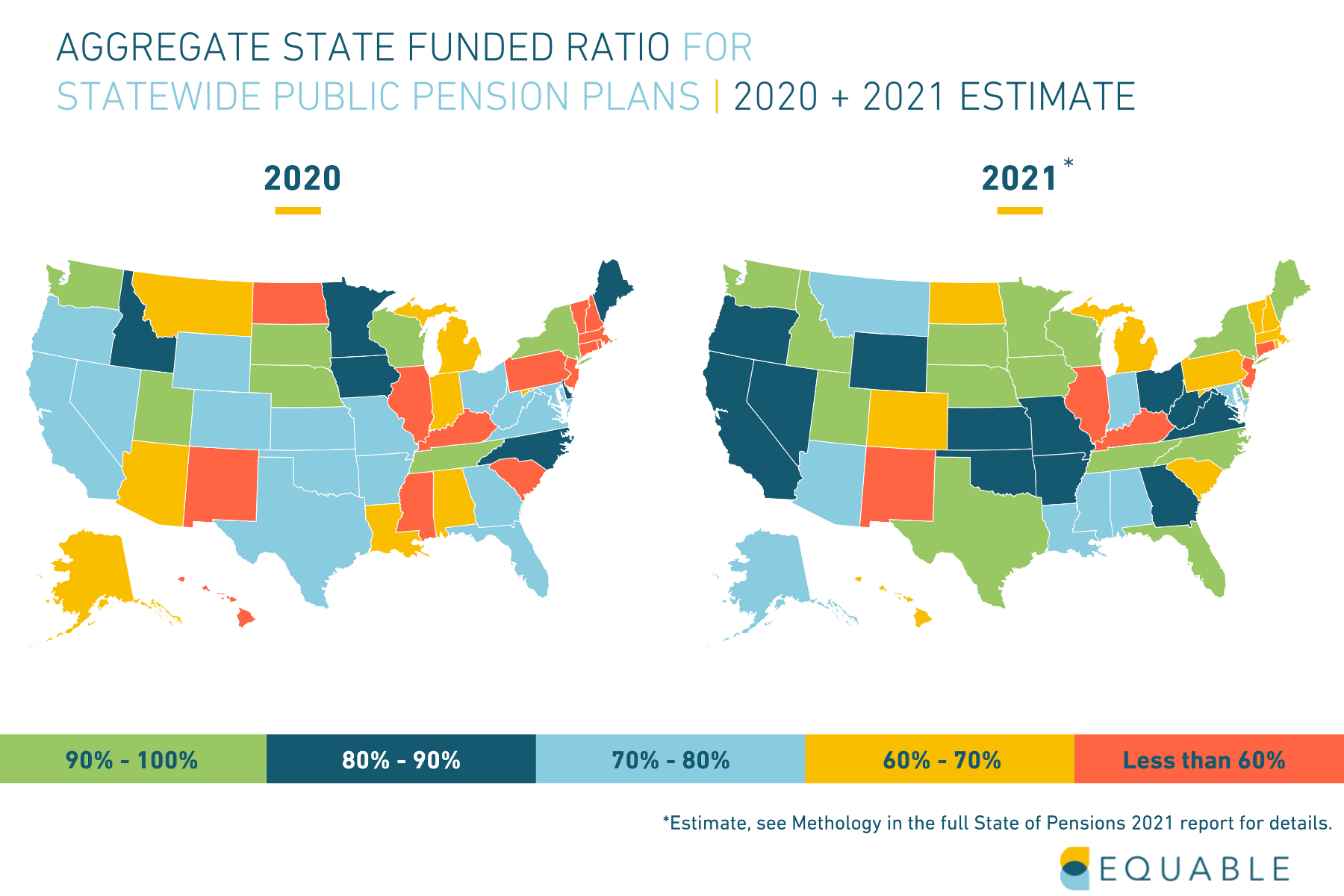

Pension Plan Funded Ratio Rankings 2024

The funded status for state and local pension plans improved in 2024, propelled forward by solid financial market performance. Yet, public pension plans are still in a fragile financial condition. Between 2023 and 2024, the average market valued public pension funded ratio increased from 75.5% up to 80.2% and once all public pension plans release their 2024 data, we estimate that unfunded liabilities will be $1.37 trillion.

This marks 18 consecutive years with an average funded ratio below 90%, the minimum threshold for pension plans to be considered resilient.

This year’s 10.3% average investment return is better than the average assumed rate of return that public plans were using last year (6.87%), but it is less than the performance of most major public equity indices like the S&P 500. Generally, this can be attributed to the poor performance of fixed income investments over the last year. For example the return for Barclay’s U.S. Aggregate Bond Index was effectively 0% for the 2024 calendar year.

There’s no question that the aggregate funded status for public pension plans while improved is still mediocre. But, funded ratios and unfunded liabilities vary widely across states and plans. Below, we look at public pension funded ratios ranked by plan and by state.

State of Pensions 2024 | State Funded Status Rankings | Plan Funded Status Details

The Top 15 Plans by Funded Status for 2024

The best funded pension plans, as of fiscal year 2024, have a few things in common. Recently designed plans with cost-sharing components, plans with risk-sharing tools, and legacy plans with a multi-decade history of strong funded status all fared well.

The Bottom 15 Plans by Funded Status for 2024

The worst funded pension plans are largely from Illinois, New Jersey, Connecticut, and Kentucky. Among the worst are a few plans funded on a pay-as-you-go basis. Here are the 15 worst pension plans by funded ratio.

*Estimate based partially on reported preliminary returns and partially on asset allocation and benchmark returns.

**Estimate based on asset allocation and benchmark returns.

2024 Funded Status by State

A Full List of Plans by 2024 Funded Status

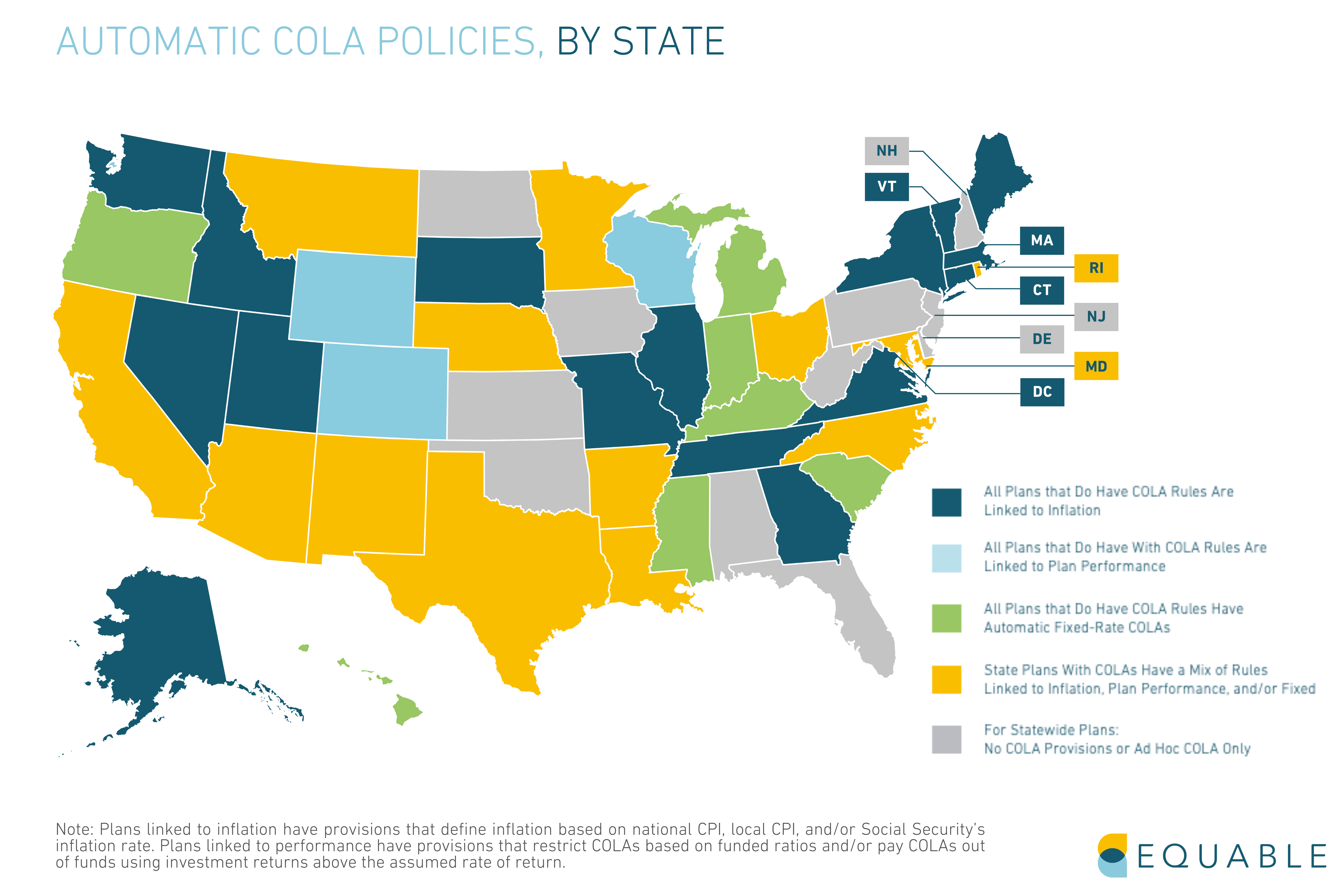

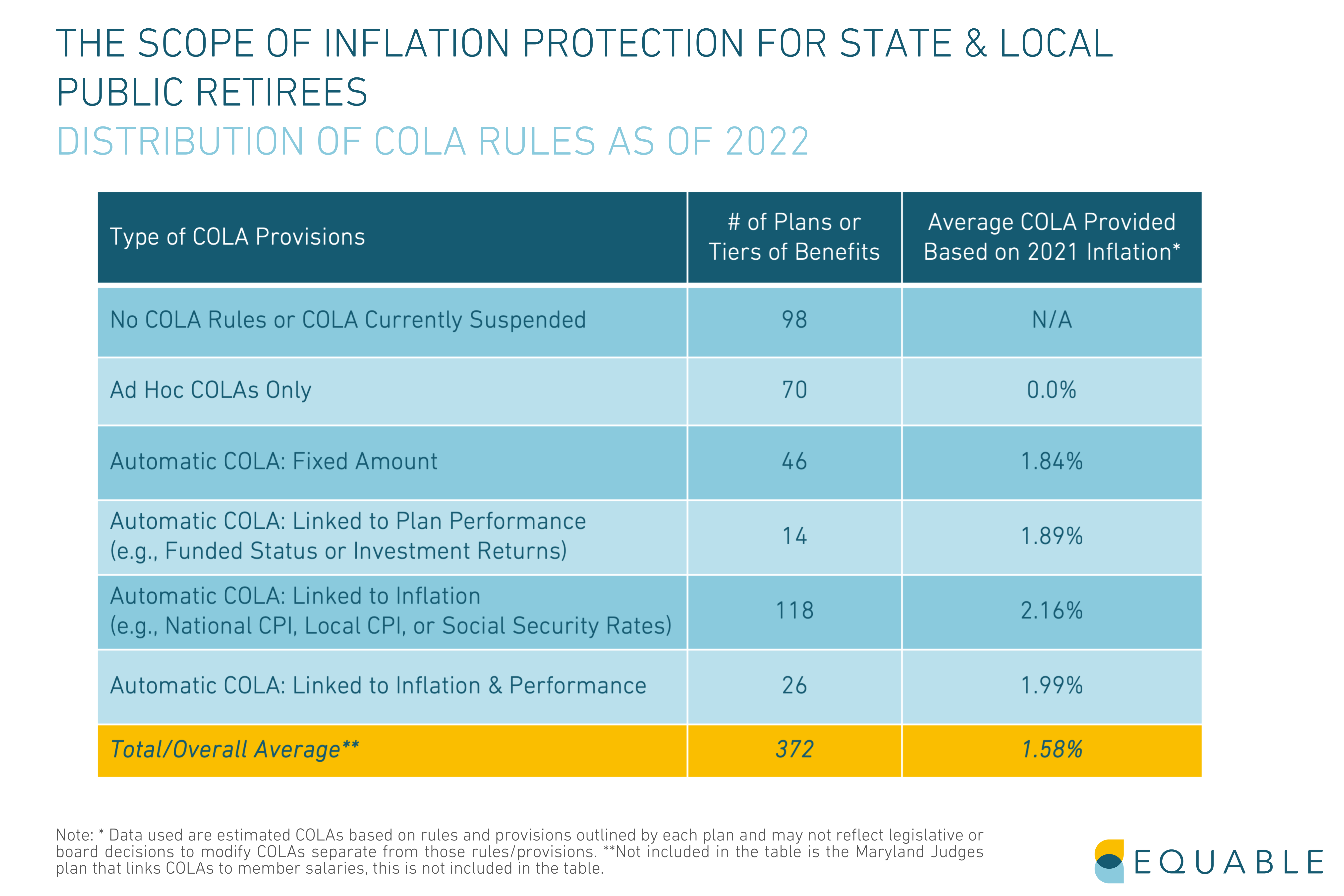

Teacher Pension COLAs in 2023

A key feature of teacher pension plans is that they offer guaranteed income for life. But unless the purchasing power of that pension income keeps up with inflation, the guarantee doesn’t necessary provide ensured financial security. That is why many defined benefit pensions for teachers come with cost-of-living adjustments, or COLAs.

However, just because there are many plans with COLAs doesn’t mean there is widespread protection from inflation.

The average COLA provided by teacher pension plans this year has been 1.96%.[1] This is effectively the same as the average cost-of-living adjustment offered to all public pension plan retirees.

The 1.96% figure is below most measures of actual price inflation in 2023. That is because many COLA policies do not exactly match inflation. Instead COLA rules have maximum rates (e.g., increasing at the rate of inflation up to 2%) or they are linked to other factors (e.g., a 2% COLA, but only if the pension fund for base benefits has adequate resources).

There are some reasonable financial reasons for these rules. Some years retired teachers get COLAs that are actually larger than inflation. However, the net effect in 2022 and 2023 has been that public pension COLAs frequently are less than inflation.

Teacher pension COLAs vary in how much inflation protection they provide, and in who gets the benefit adjustments. In this article, we explain some of the different kinds of cost-of-living adjustments provided to retirees from public employee pension funds.

First, here is a list of teacher pension plans and classes of benefits and the COLAs they’ve provided in 2023.

Not all teacher pension COLAs are created equal. If you are trying to determine whether or not a COLA is adequate enough to maintain the spending power of your retirement benefits, you should consider the following elements of your plan's COLA policy:

1. Compounding versus Non-Compounding Benefits

Retirement funds have two ways of adjusting underlying benefits when paying out teacher public pension COLAs.

Compounding Benefits: Retirement funds permanently adjust the base benefit and add any any future changes to benefits on top.

For example, someone with a $40,000 pension that gets a 2% COLA will have their base benefit increased to $40,800. The next year, if inflation means a 1.5% COLA, then the adjustment is calculated based on the new, higher number. So in this case, the benefit would increase to $41,412.

Non-Compounding Benefits: This means that all inflation adjustments are based on the original pension benefit value. Each year benefits increase, you get to keep the adjustment from the previous year. But, the percentage increase is based on your original pension.

For example, a former teacher with a $40,000 pension that got a 2% COLA would see $800 added on top for a total pension of $40,800. The next year, a 1.5% COLA would be calculated on the original $40,000 pension. $600 would then be added on top for a total pension of $41,200.

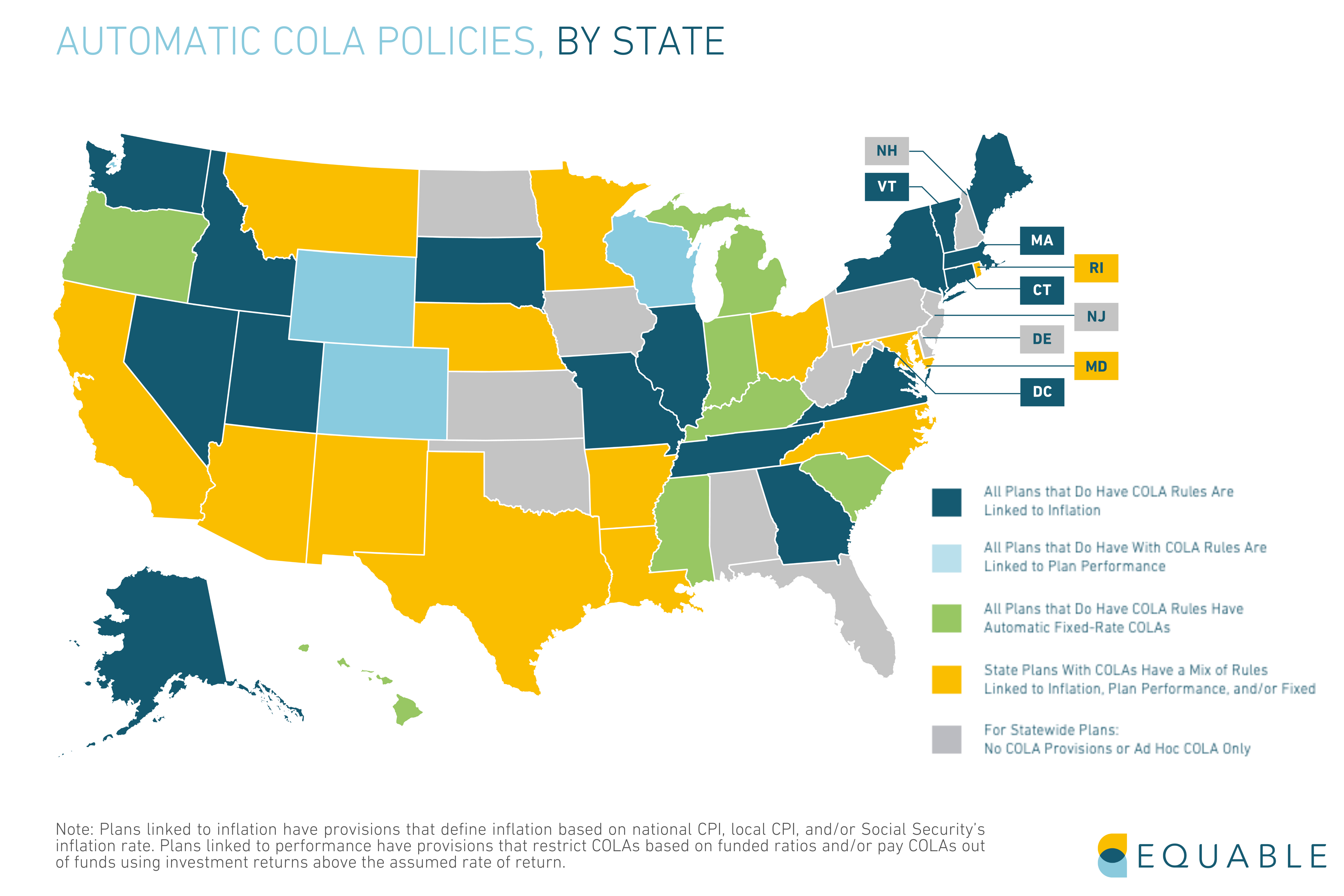

2. Three Types of Automatic Public Pension COLAs

There are generally three policy frameworks for those teachers who do have automatically granted COLAs that protect public worker pensions from inflation:

- Fixed-Rate COLAs: A pre-fixed specific percentage of benefit increase (or minimum dollar amount).

- COLAs Linked to Inflation: A percentage increase to benefits based on the national consumer price index (CPI), a local CPI, or the Social Security inflation rate. The actual amount is typically “up to” a maximum rate, such as 2% or 3%.

- COLAs Linked to Plan Performance: A percentage increase to benefits that is dependent on the funded ratio and/or investment performance of the underlying pension plan. The actual amount is also typically “up to” a maximum rate, but that maximum rate is determined by the specific provisions around plan performance. For example, the maximum COLA rate may be cut in half or suspended if the pension fund is under 80%.

Some state pension funds have inflation adjustments linked to both inflation and pension plan performance.

3. Ad Hoc Cost-of-Living Adjustments

There are a number of teacher pension plans that do not provide consistent inflation protection. Some of these states have no legal provisions to offer COLAs. Other states only payout COLAs if the legislature authorizes the benefit adjustment. Because COLAs are not legally required in these states, they are called "ad hoc" COLAs. These COLAS are also heavily dependent on local politics and legislative budgets.

Note [1]: This is an average of 158 classes of defined benefits, including actual reported percentage rates adjusting benefits starting in the 2023 calendar year and percentage rates based on published COLA policies.

Pension Plan Funded Ratio Rankings 2023

At the end of fiscal year 2023, the average funded ratio for American public pension plans was 78.1%. While this is a modest improvement over the losses of 2022, it is also a continuation of the fragile funded status that has persisted for more than a decade and a half after the financial crisis.

Once all public pension plans release their 2023 data, we estimate that unfunded liabilities will be $1.44 trillion. The combined funded status for the top state and local retirement systems will be 78.1%, based on available data through December 31, 2023. This is up from the 74.9% funded ratio during fiscal year 2022.

Despite modest improvements in funded status and unfunded liabilities, investment returns tell a more complex story. Strong investment returns in the last few months of the year drove the average investment return to 7.47%, beating the average 6.9% assumed rate of return. But, on a plan-by-plan basis, just 53% of plans beat their investment assumptions. Meaning 2023 was much better to some plans than others.

There’s no question that the aggregate funded status for public pension plans while improved is still mediocre. But, funded ratios and unfunded liabilities vary widely across states and plans. Below, we look at public pension funded ratios ranked by plan and by state.

State of Pensions 2023 | State Funded Status Rankings | Plan Funded Status Details

The Top 10 Plans by Funded Status for 2023

The best funded pension plans, as of fiscal year 2023, have a few things in common. Recently designed plans with cost-sharing components, plans with risk-sharing tools, and legacy plans with a multi-decade history of strong funded status all fared well.

The Bottom 15 Plans by Funded Status for 2023

The worst funded pension plans are largely from Illinois, New Jersey, Connecticut, and Kentucky. Among the worst are a few plans funded on a pay-as-you-go basis. Here are the 15 worst pension plans by funded ratio.

*Estimate based partially on reported preliminary returns and partially on asset allocation and benchmark returns.

**Estimate based on asset allocation and benchmark returns.

2023 Funded Status by State

A Full List of Plans by 2023 Funded Status

State of Pensions 2023: National Pension Funding Trends

This article features content from State of Pensions 2023

Read the Full Report

Download the Fact Sheet

The State of Pensions in 2023: Public Pension Debt has Flatlined

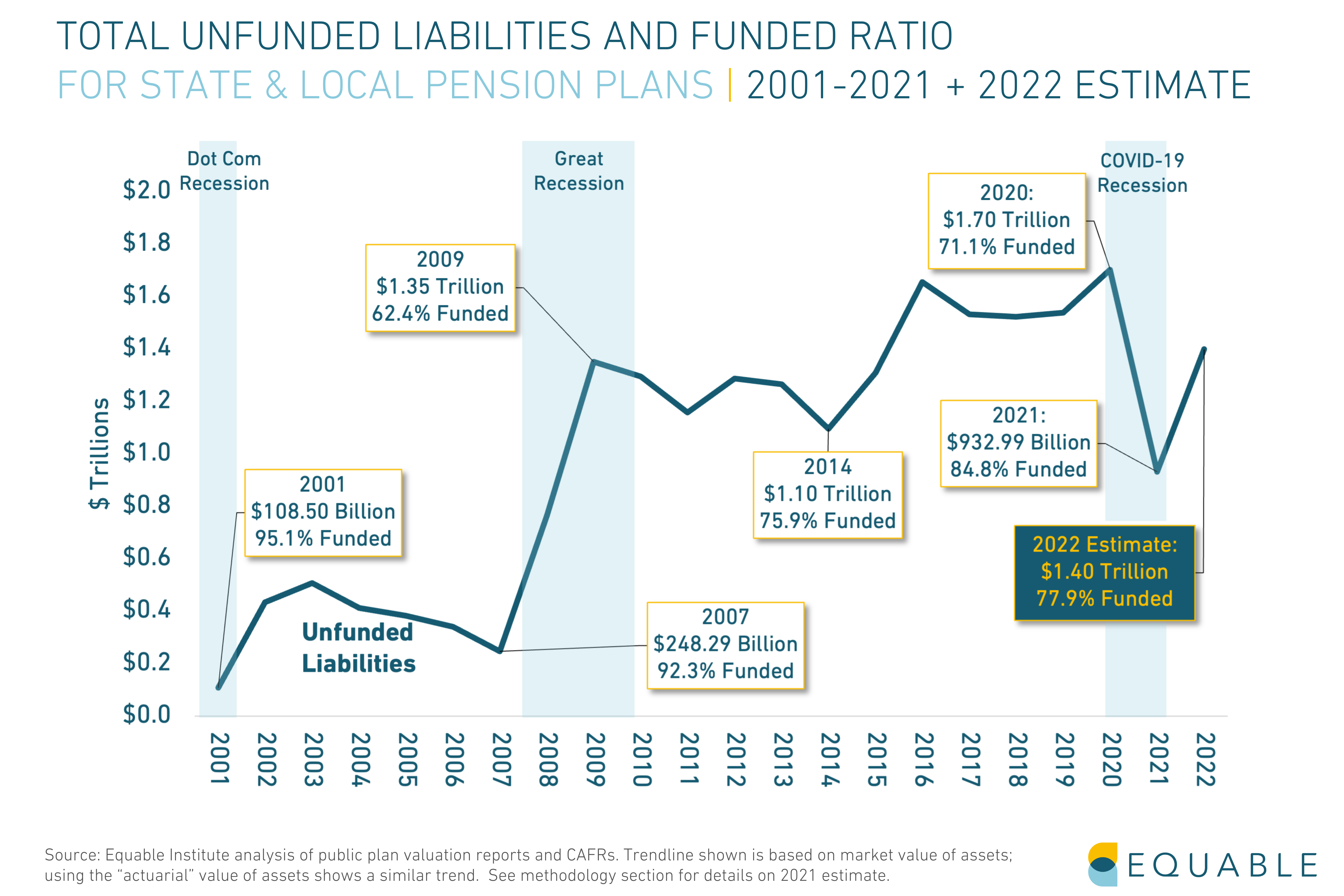

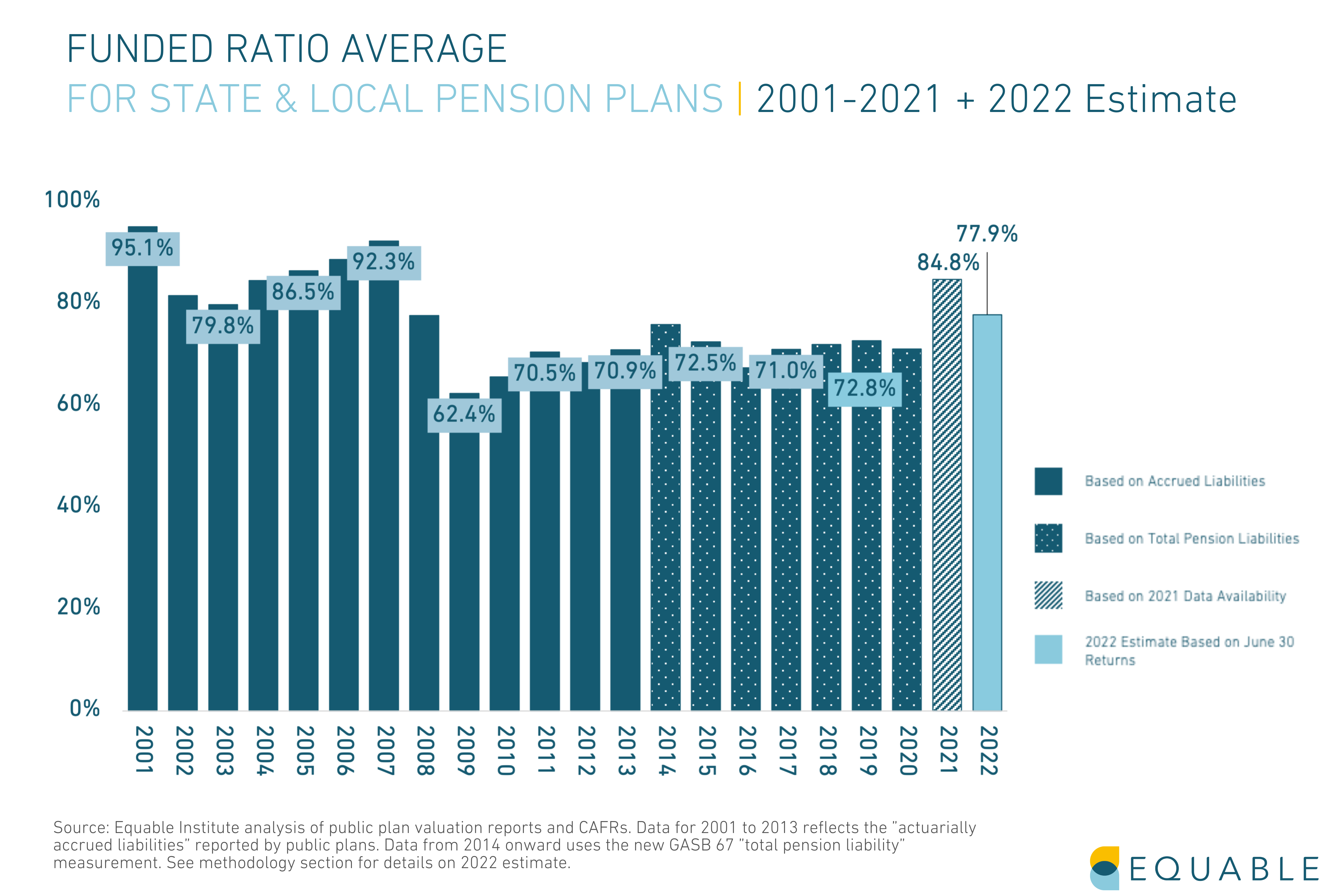

What is the pension funding gap in 2023?

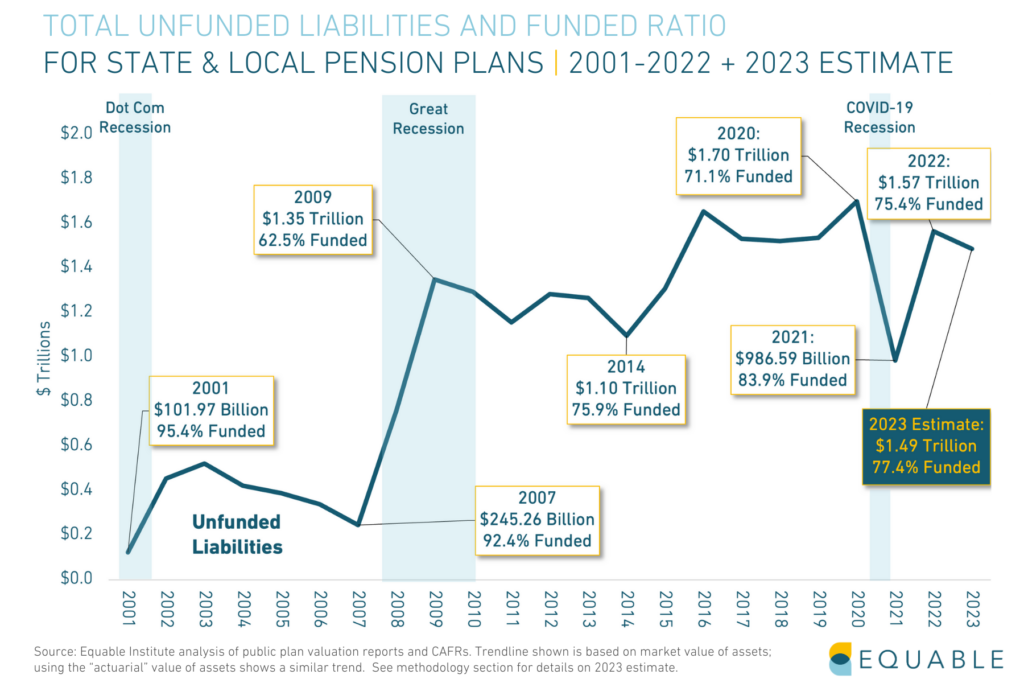

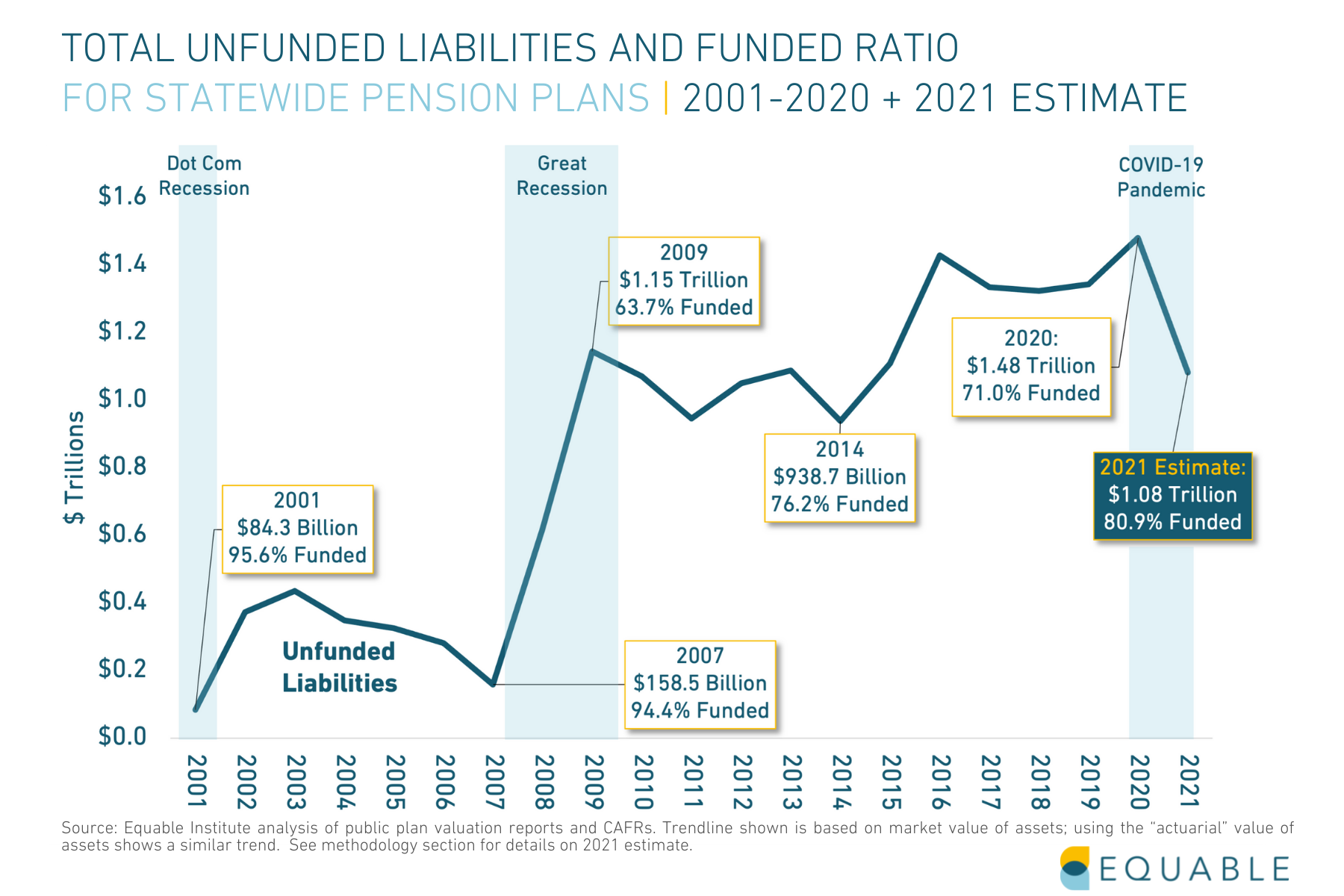

The national pension funding shortfall (or pension debt) for statewide retirement systems was $1.57 trillion at the end of 2022, per Equable Institute’s State of Pensions 2023 report. We estimate that 2023 unfunded liabilities will remain effectively flat, decreasing slightly to $1.49 trillion.

The funding shortfall is the gap between money held by pension funds and the value of all future benefits it has promised to pay. This is formally called "unfunded liabilities" and is also sometimes called pension debt.

The shortfall was, in part, caused by investment volatility set off by the Covid-19 pandemic. However, there has been relatively little change in the national shortfall in assets for state and local pension plans since the Financial Crisis. Unfunded liabilities decreased to their lowest level in 2021, but since then have reverted to just a slight improvement from pre-Covid 19 pandemic levels.

Preliminary 2023 investment returns for state and local plans are 5.3% on average. Federal Reserve policy to address inflation ended an era of easy money, which translated into a bear market for public equities and reduced valuations, known as markdowns, for private equity and real estate.

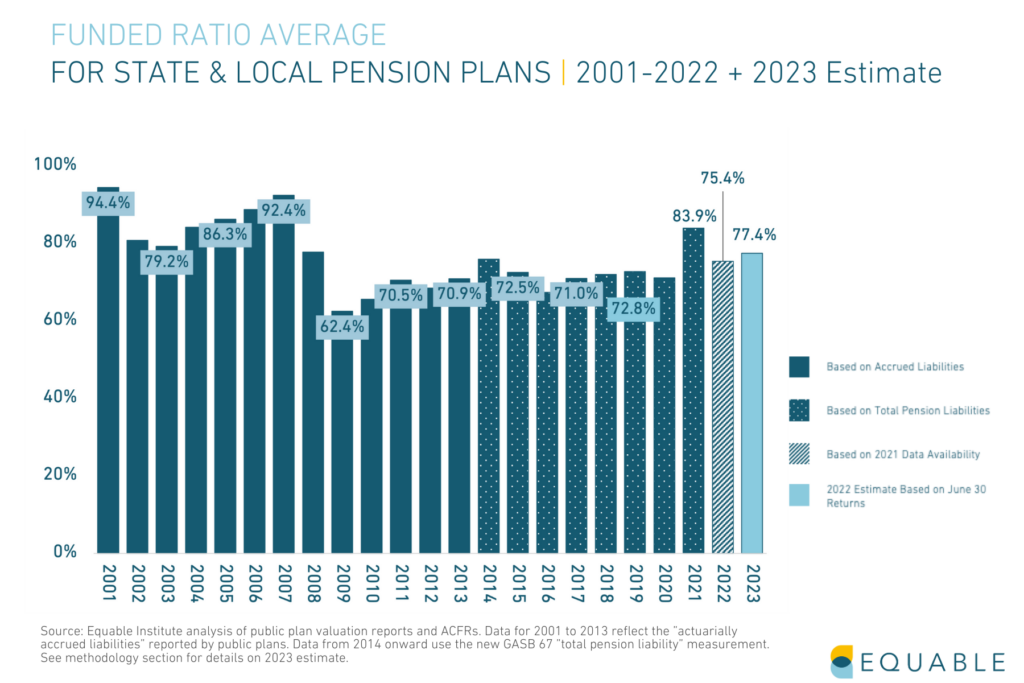

On average, American public pensions plans currently hold 77.4% of assets needed to pay future retirees their pension benefits. This is a positive improvement over the 72.8% pre-Covid funded ratio in 2019. But, it is still much lower than the 83.9% funded ratio in 2021. More importantly, it's dramatically lower than the pre-Great Recession funded ratios of 2007 and 2008.

In contrast, retirement systems in the U.S. had 92.4% of the money promised to public retirees in 2007, before the Great Recession. Losses because of the Financial Crisis of 2008 knocked this funded ratio down to 62.4% by 2009.

Pension funds have been able to recoup some of the losses experienced during the beginning of the Covid-19 pandemic. But, they still have not recovered from the 2008 recession. And capital market forecasts are warning future returns are likely to be muted.

To maintain the positive trends in pension funding, states will need to adopt safer practices. This includes establishing realistic assumed rates of return and appropriately managing the risk level of their investments.

Public Pensions in 2023: Why the Assumed Rate of Return Matters

There is a significant gap between projected earnings and fiscal reality for public pension plans in many states. This gap has persisted for several years.

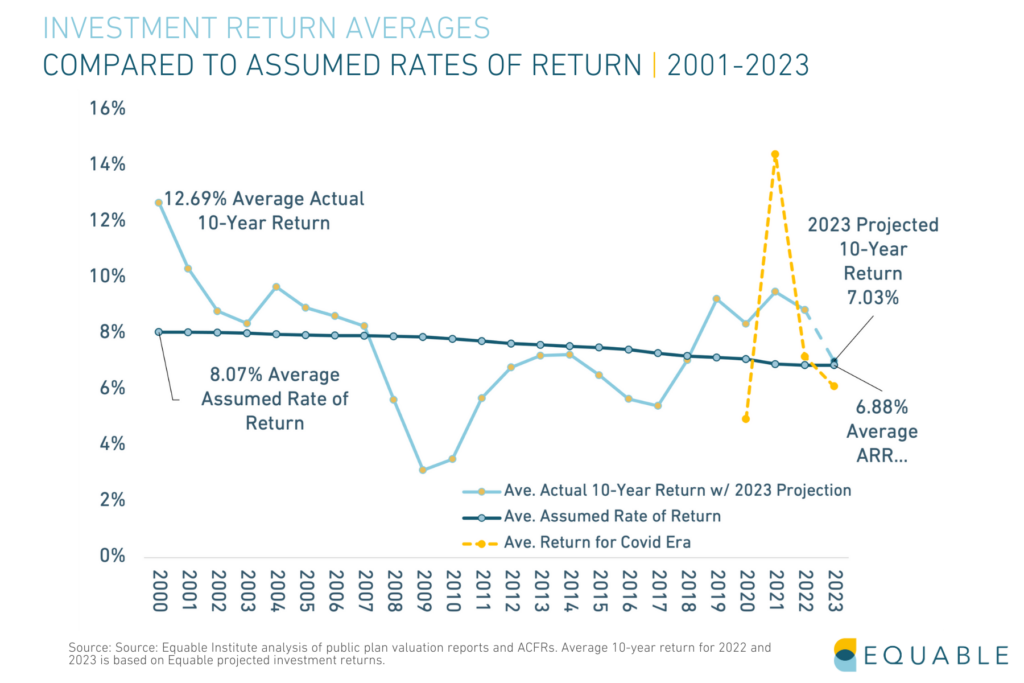

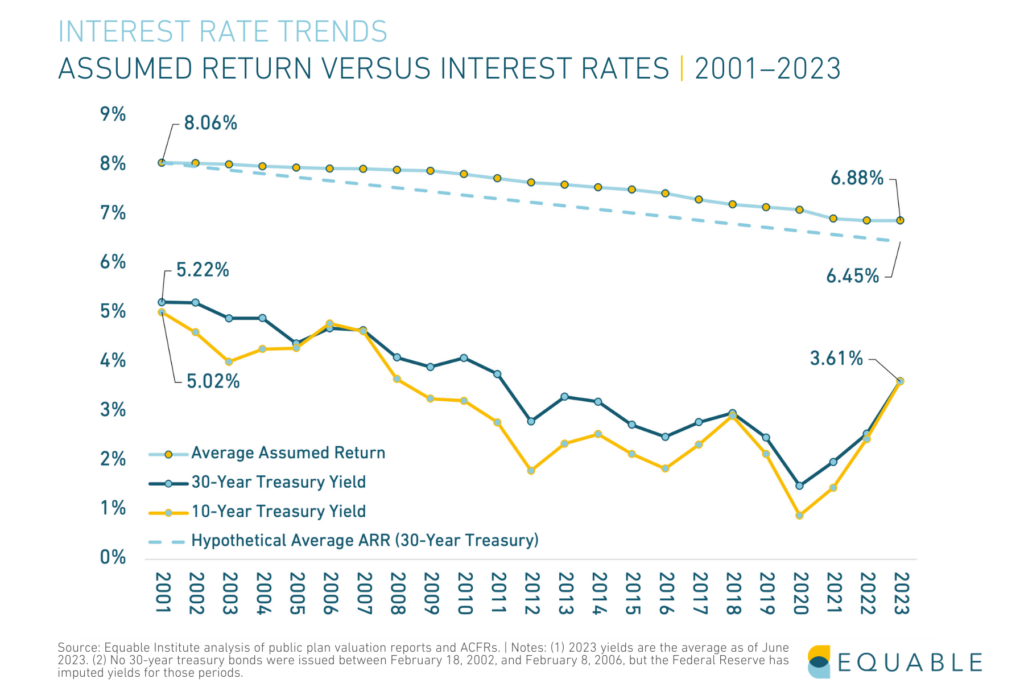

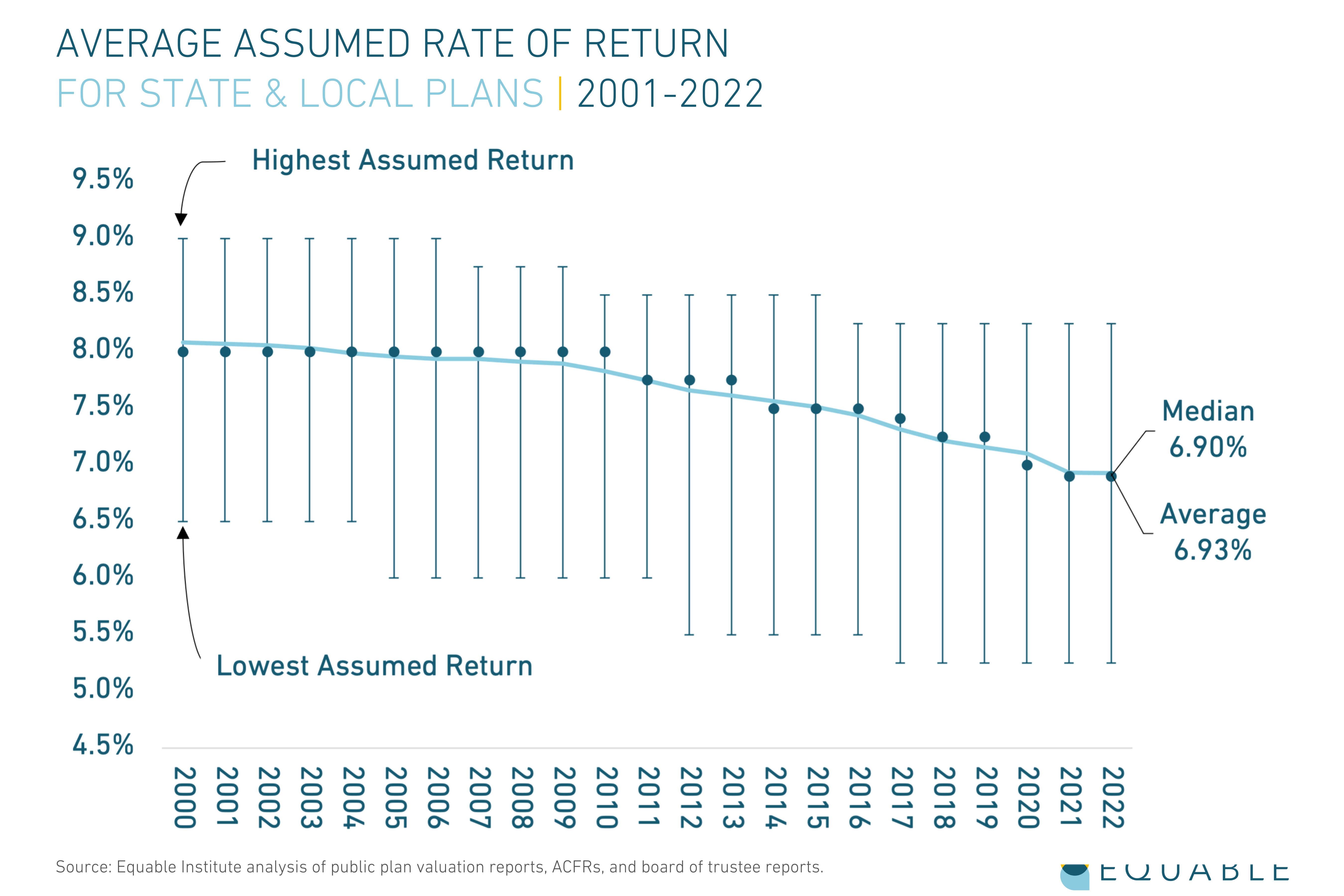

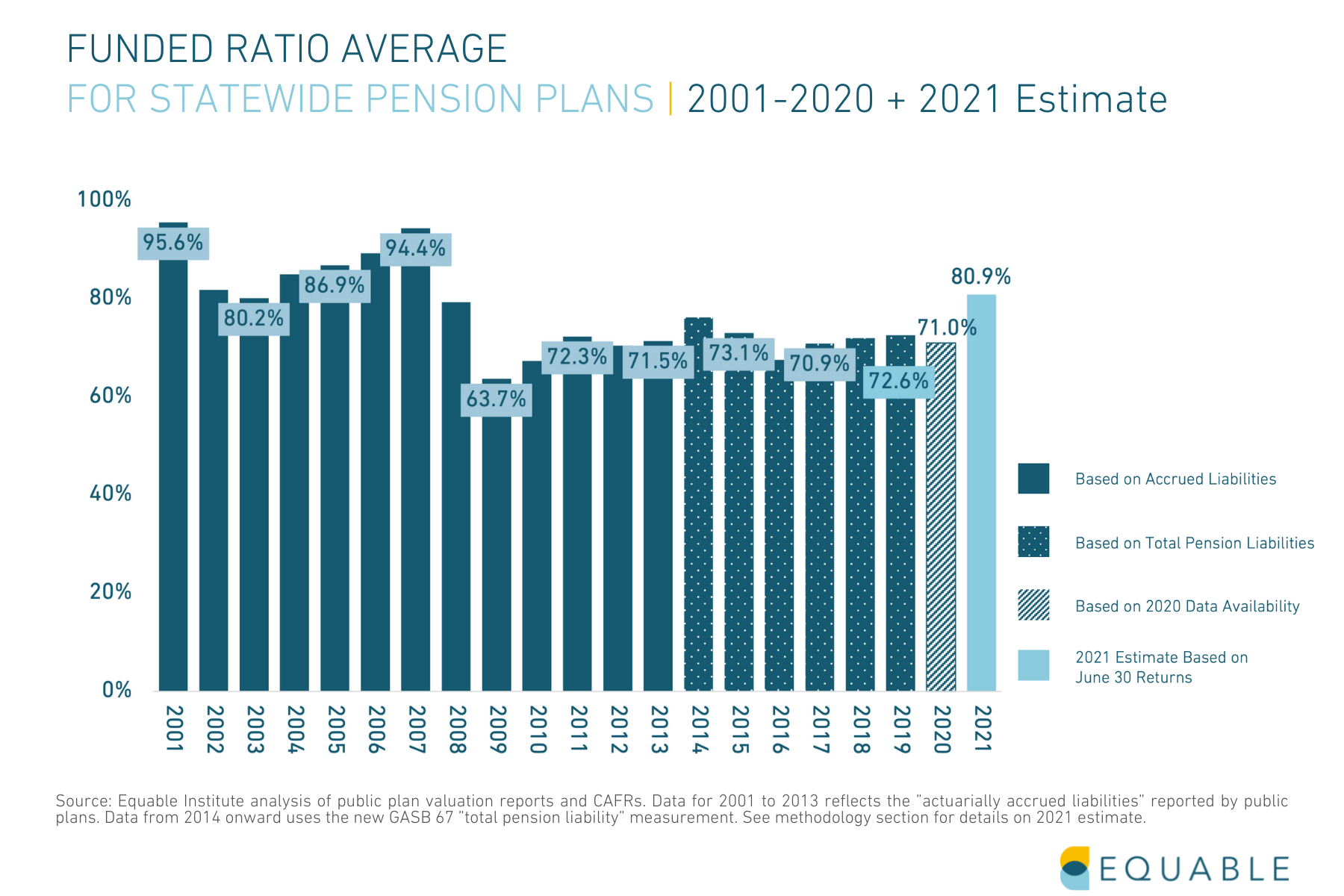

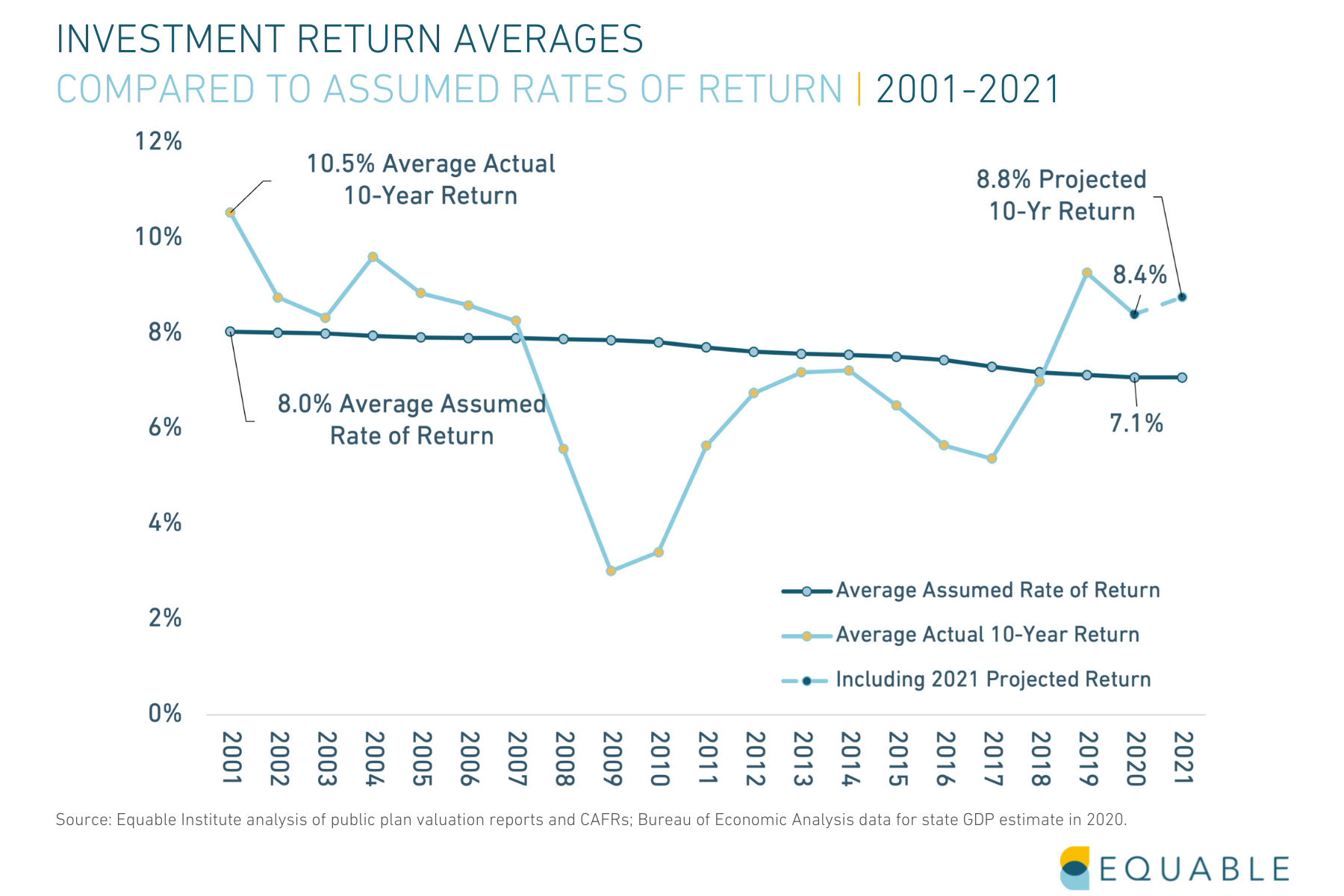

Still, the assumed rates of return used by many retirement systems have remained significantly higher than actual investment earnings. However, many states have meaningfully reduced their assumed rates of return in response to economic shifts. The average assumed rate of return is now 6.88% in 2023—down from 8.05% in 2001.

We estimate 2023 investment returns for U.S. public pension funds will average 5.3% (based on data through June 30).

This is significantly lower than the 6.88% average assumed rate of return. For the first time, however, the average 10-year investment return has fallen to around the assumed rate of return. This indicates a dampened outlook for investment returns long-term.

The average investment return for the Covid era (2020-2023) is 6.15%, which is below average investment assumptions. Despite record investment returns in 2021, the Covid era has not proven to be overly beneficial for pension funds.

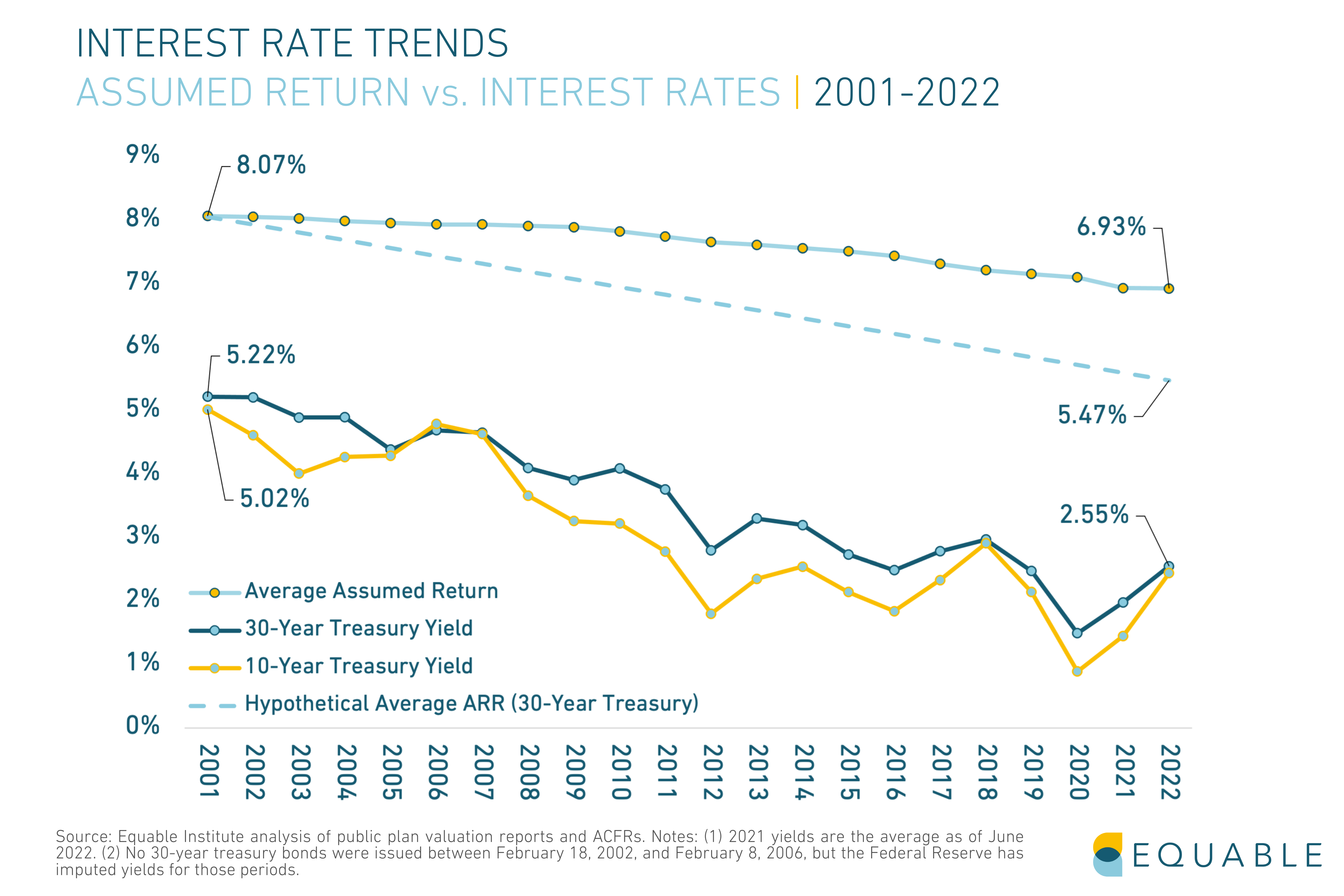

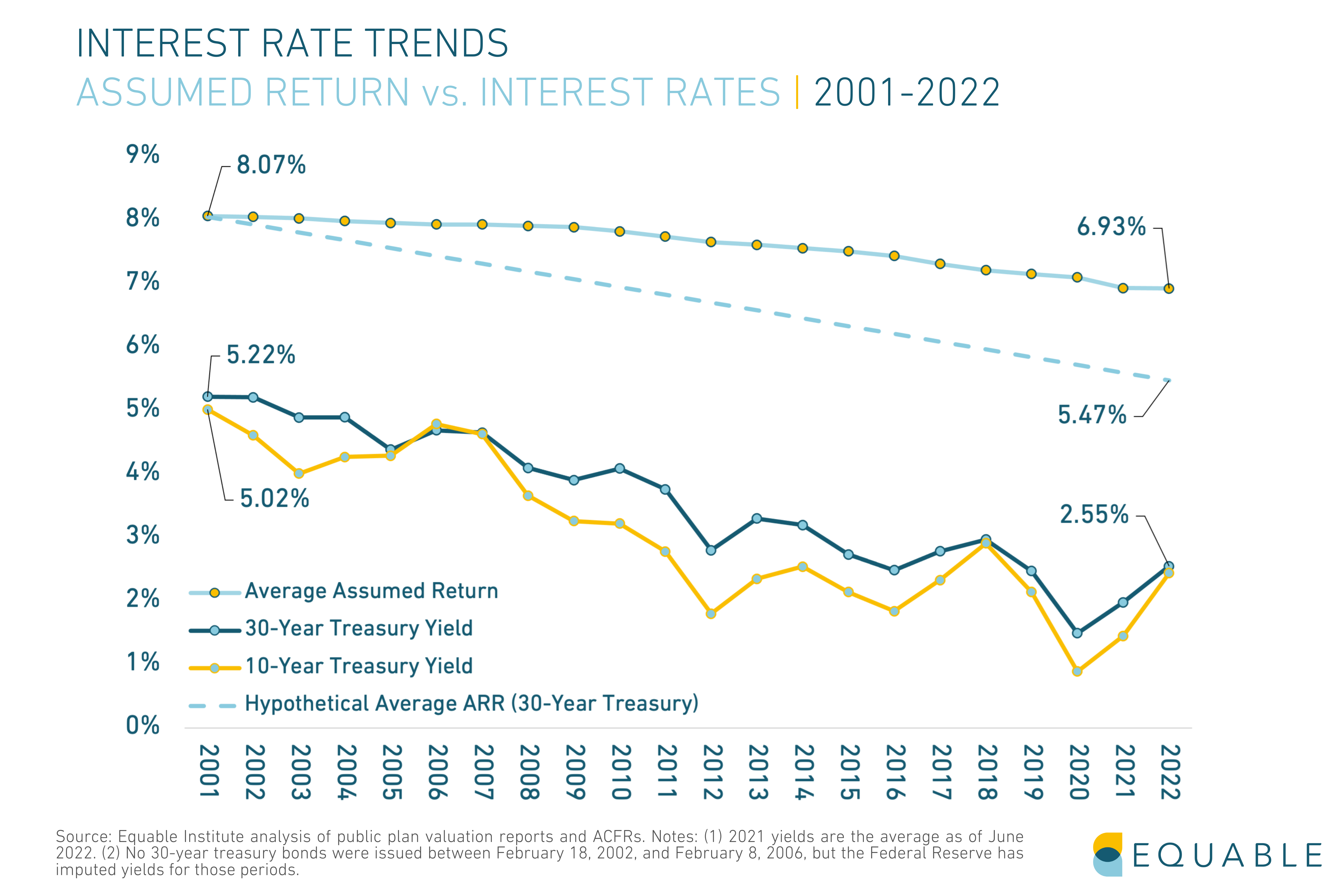

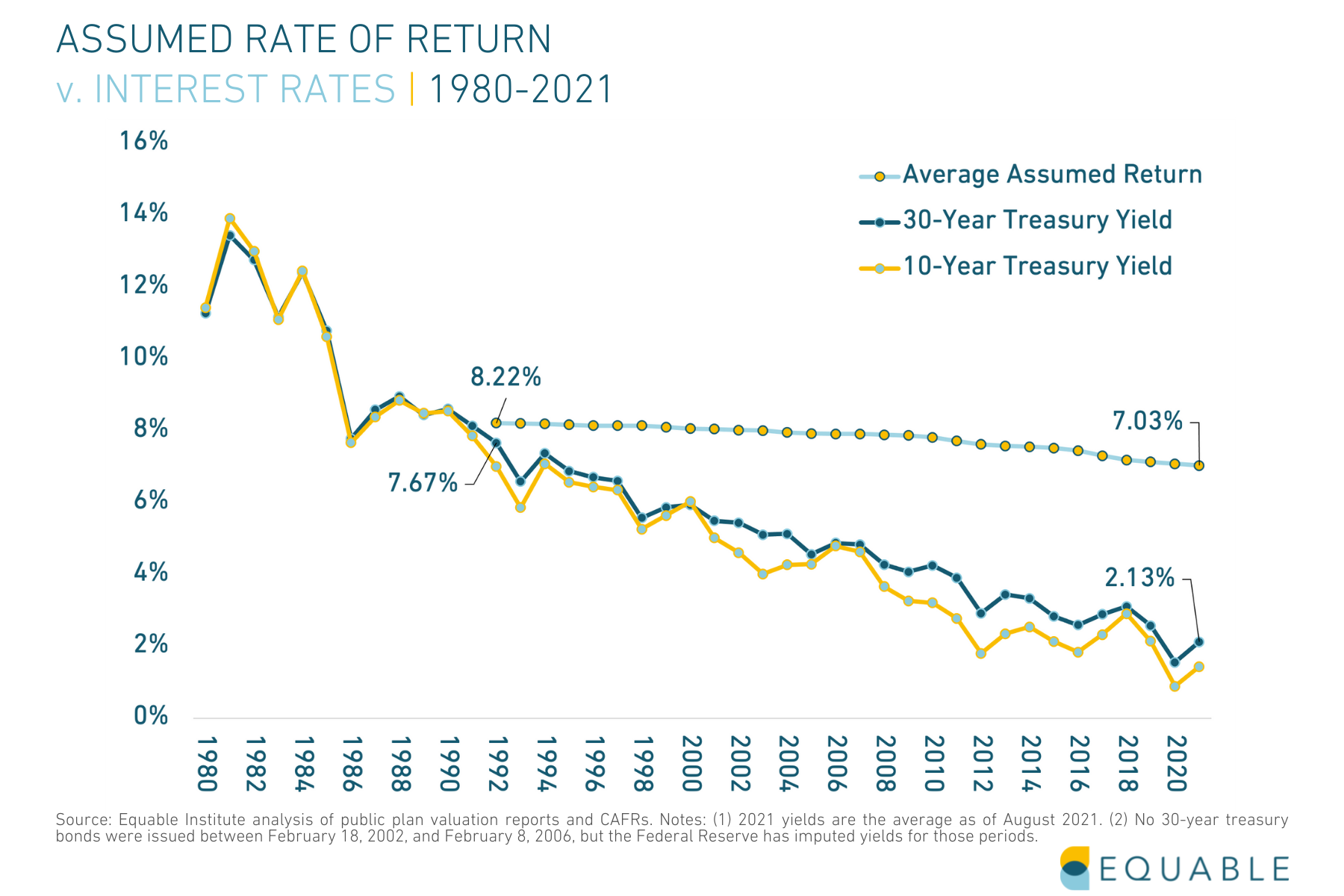

Interest rates are considered an indicator of future market performance. States and pension boards have been slow to reduce their assumed rates of return, relative to declining interest rates. Even factoring in recent interest rate increases, the gap between interest rates and assumed rates of return reflects an increased amount of risk that pension funds are accepting relative to two or three decades ago.

Pension fund assumed rates of return have not kept pace with rapidly declining interest rates over the last two decades. Many funds are over-estimating what their investments will earn. Others are making a lot of high risk, high reward investments to try and hit their optimistic targets. Some funds are doing both.

The chart below shows the recent trend in assumed rates of return in tandem with interest rates.

If assumed returns had kept pace with declining interest rates since 2001, the average assumed rate of return for 2023 would have been around 6.45%, not the 6.88% plans currently average.

The optimistic assumed rate of return used by most pension funds to make financial decisions may be increasingly hard to achieve if America’s economic future remains uncertain.

Pension Funding in 2023: How does national pension debt affect public workers?

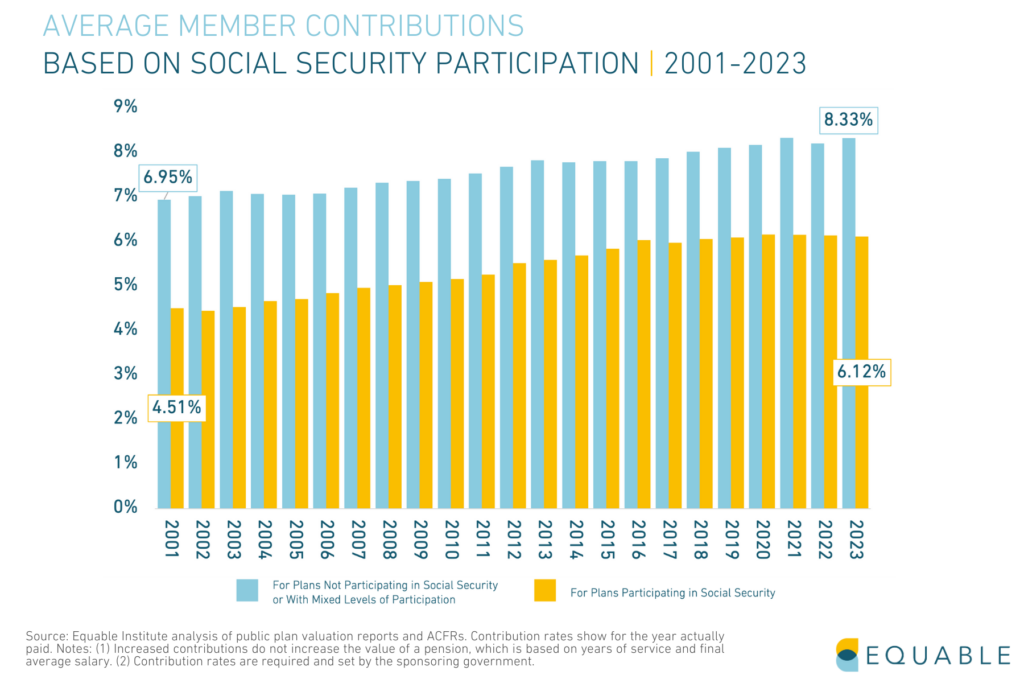

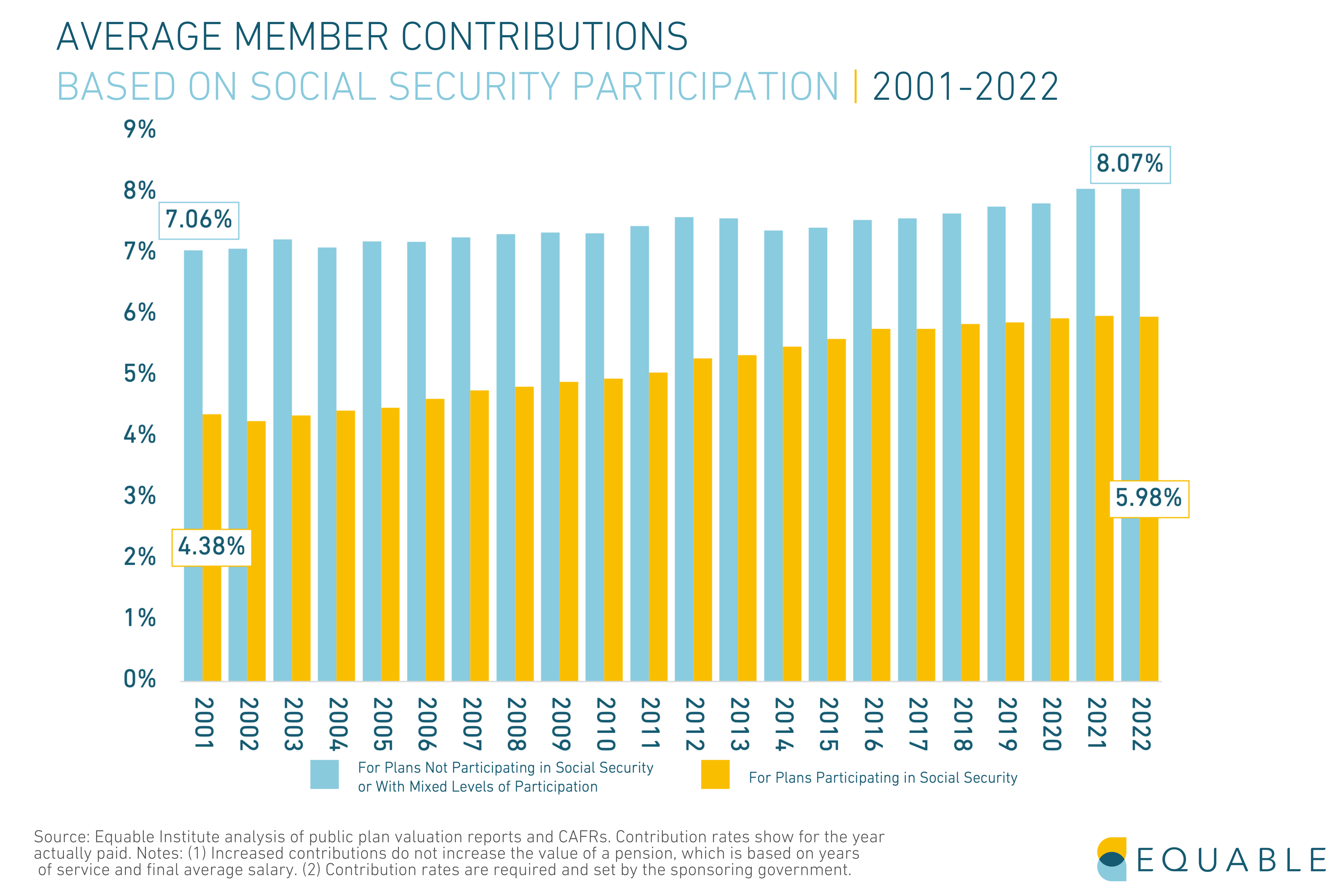

The pension debt carried by governments is costly to pay down and creates pressure on the public budget. It may cause an increase in required pension contributions for public employees or benefit reduction like the elimination of cost-of-living (COLA) adjustments for retirees, which in an era of record inflation is increasingly important. Higher employee contribution rates means less money in public workers' paychecks. In recent years, the first number has been growing while the latter shrinks.

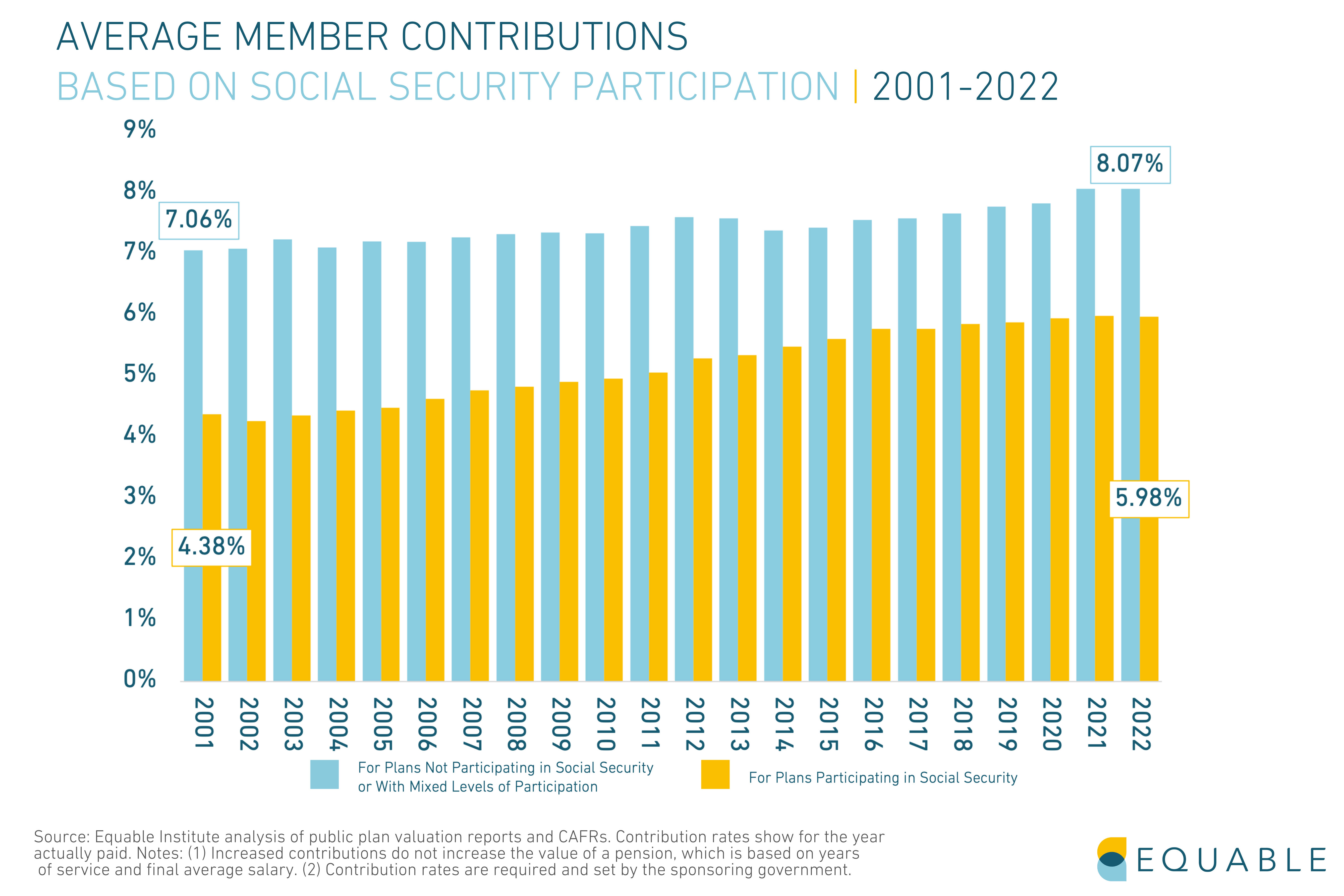

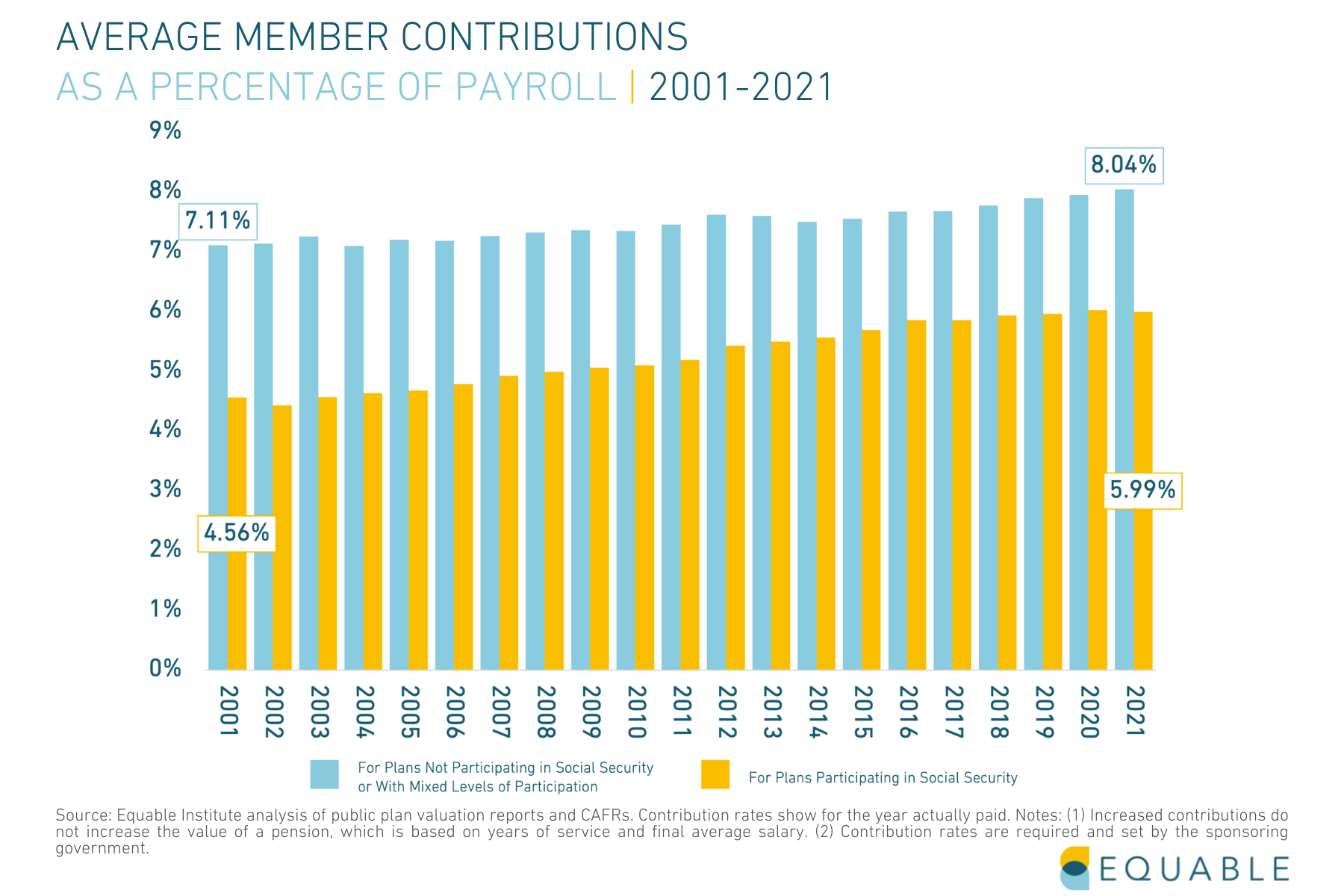

In 2023, average member contribution rates reached an all-time high. Public sector workers who are enrolled in Social Security are paying 35.7% more than they did in 2001. Workers who are not enrolled in social security are paying 19.9% more than they did in 2001.

In times of economic hardship, higher contribution rates for governments may have other impacts. They may result in higher property taxes, delayed raises, cuts in school funding, or reductions in essential services.

Pension Trend to Watch in 2023 and Beyond: Public Pension Plans Are Addicted to Risk

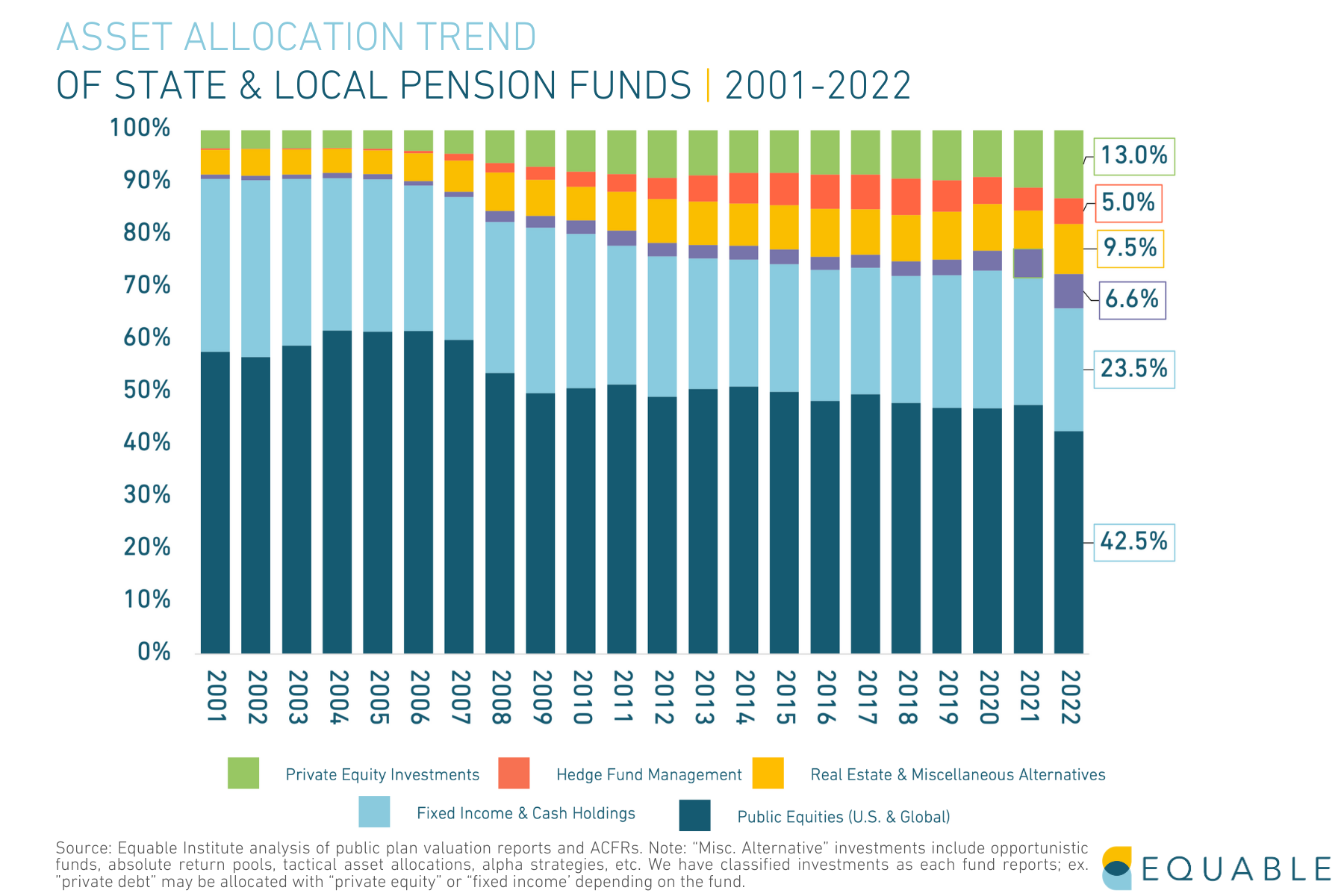

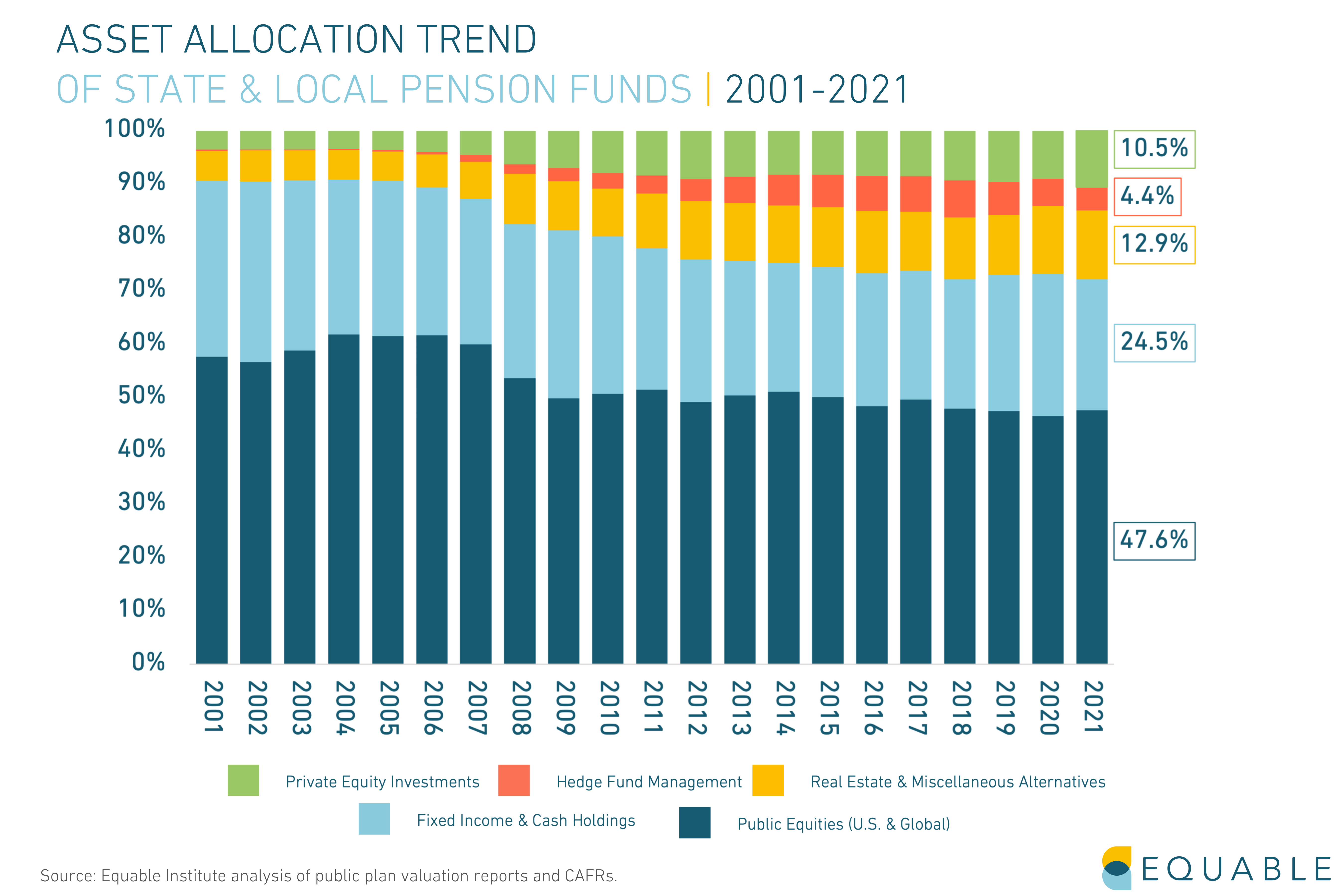

How are pension plans investing their assets?

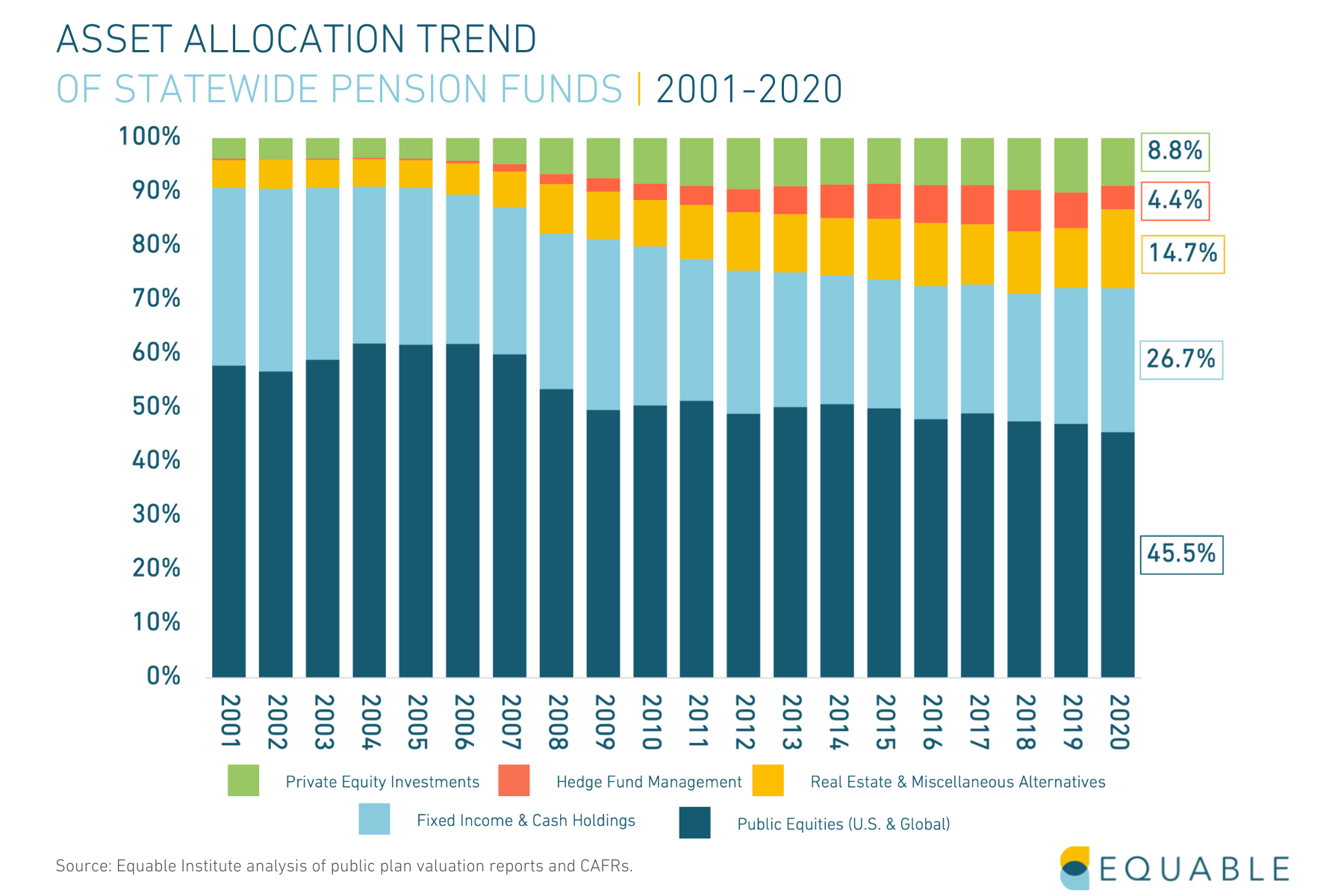

States are trying to make up for negative pension funding trends like lower projected returns on stocks and bonds. They are utilizing more and more alternative investments to chase higher returns. This includes investments hedge funds and private equity strategies, as well as real estate.

Since 2001, pension funds invested a higher percentage of their assets into these alternative investment categories. Hedge funds, real estate, and private equities are known for a lack of transparency. They also tend to be more volatile in times of economic uncertainty.

In 2023, “Alternatives” comprise a third of pension fund investments (34.0%), the largest share in history. Notably, private equity jumped to 13.0% of allocations.

Ultimately, state pension funds are in competition with each other when vying for these deals and market strategies. Statistically speaking, there are going to be plans that lose out on this work. Unless state pension funds have better success than the market, it is likely that the net average result across all plans will be modest at best. At worst, these strategies will perform worse than traditional passive equity investment strategies.

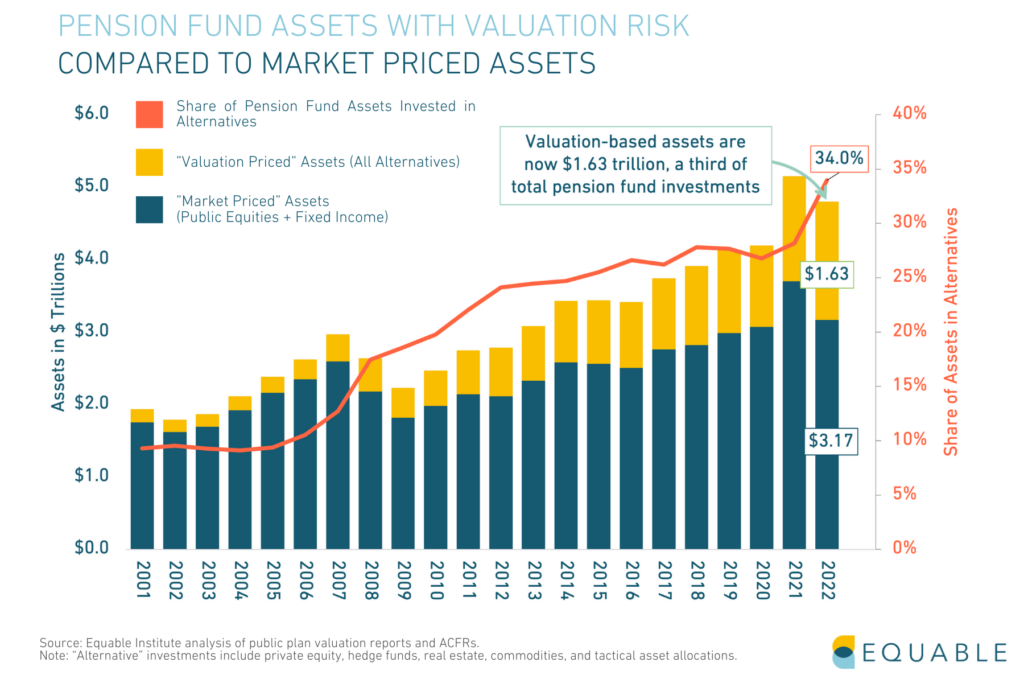

Public Pension Funds are Vulnerable to “Valuation Risk”

Public pension funds now face an emerging concern: “valuation risk.” While traditional investments like stocks and bonds are based on prices set by the market, alternative assets are not.

The majority of alternative investments via private equity and real estate use valuation models to get priced or for when they sell. There is very little transparency when it comes to these models. They are not updated in real time the way market prices are, so it is almost impossible to prove if the value of these assets are accurate or “fair.”

This means that a large and growing share of pension fund investments might not be correctly valued. If that’s the case, many states may not be making large enough contributions to their pension funds to ensure their stable funding. And, if the value of those assets get marked down, states could see significant declines to their funded ratio. This is valuation risk.

As of 2022, $1.6 trillion of public pension fund assets have exposed themselves to valuation risk. This comprises 34% of pension funds’ investments.

However, not all states expose themselves to the same level of valuation risk. The interactive map below shows what percentage of each state’s investments are in alternative assets.

The State of Pensions 2023: Most Public Pension Systems Are Still Financially Fragile or Distressed

What do pension funding gaps mean for states?

Despite an improvement over 2022’s -5.94% investment returns, 2023 is unlikely to yield meaningful improvement for most states’ funded status.

Most states are going to have flat funded status from 2022 to 2023: only 7 states changed color on the map from 2022 below. Out of the 225 plans in Equable’s analysis, 46 plans will have a lower funded ratio in 2023 than the previous year.

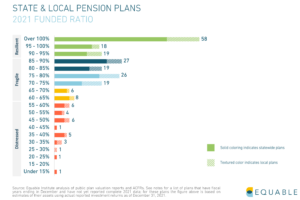

Currently, 59% of all statewide plans are "fragile" and more than 16% of plans are "distressed" as of 2023. These plans face an uphill climb to recovery due to sharp losses in 2022, despite strong returns in 2021.

Fragile status generally means a retirement plan is between 60% and 90% funded. While they’re not at immediate risk of insolvency, they are accumulating unfunded liabilities. Over time, that will gradually become a strain on budgets and government revenues. One or two asset shocks could send the plan into a downward spiral.

Today, only 25% of state and local pension plans are economically resilient, according to the Equable Institute report. This means the plans hold assets that cover 90% or more of promised public employee pension benefits for at least a few consistent years.

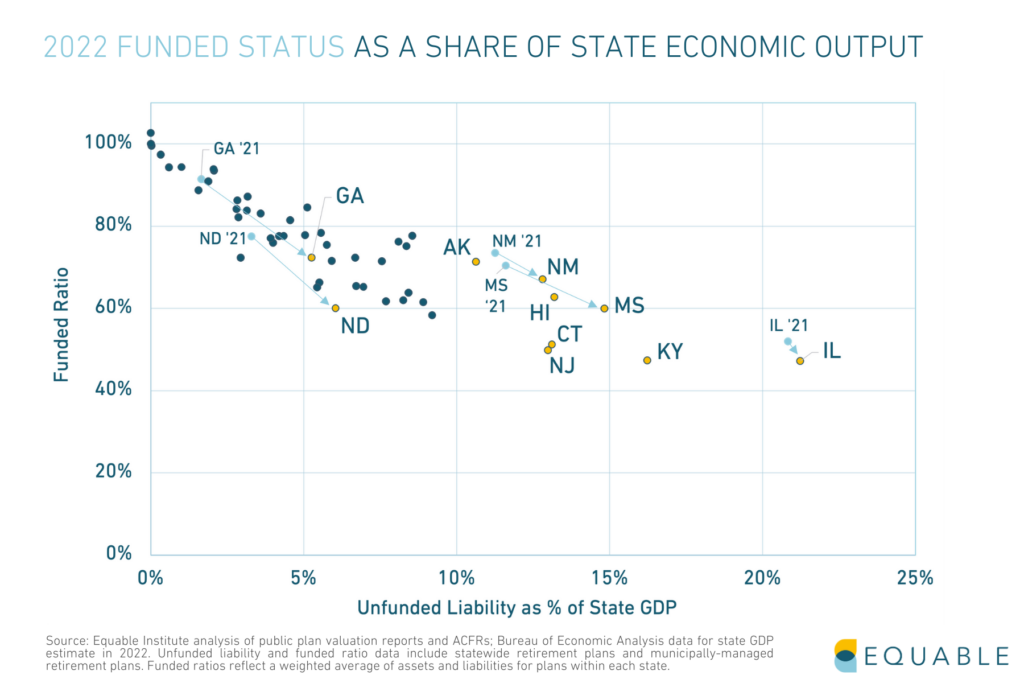

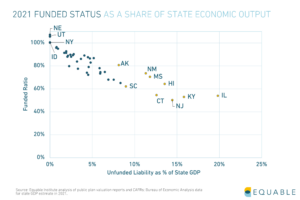

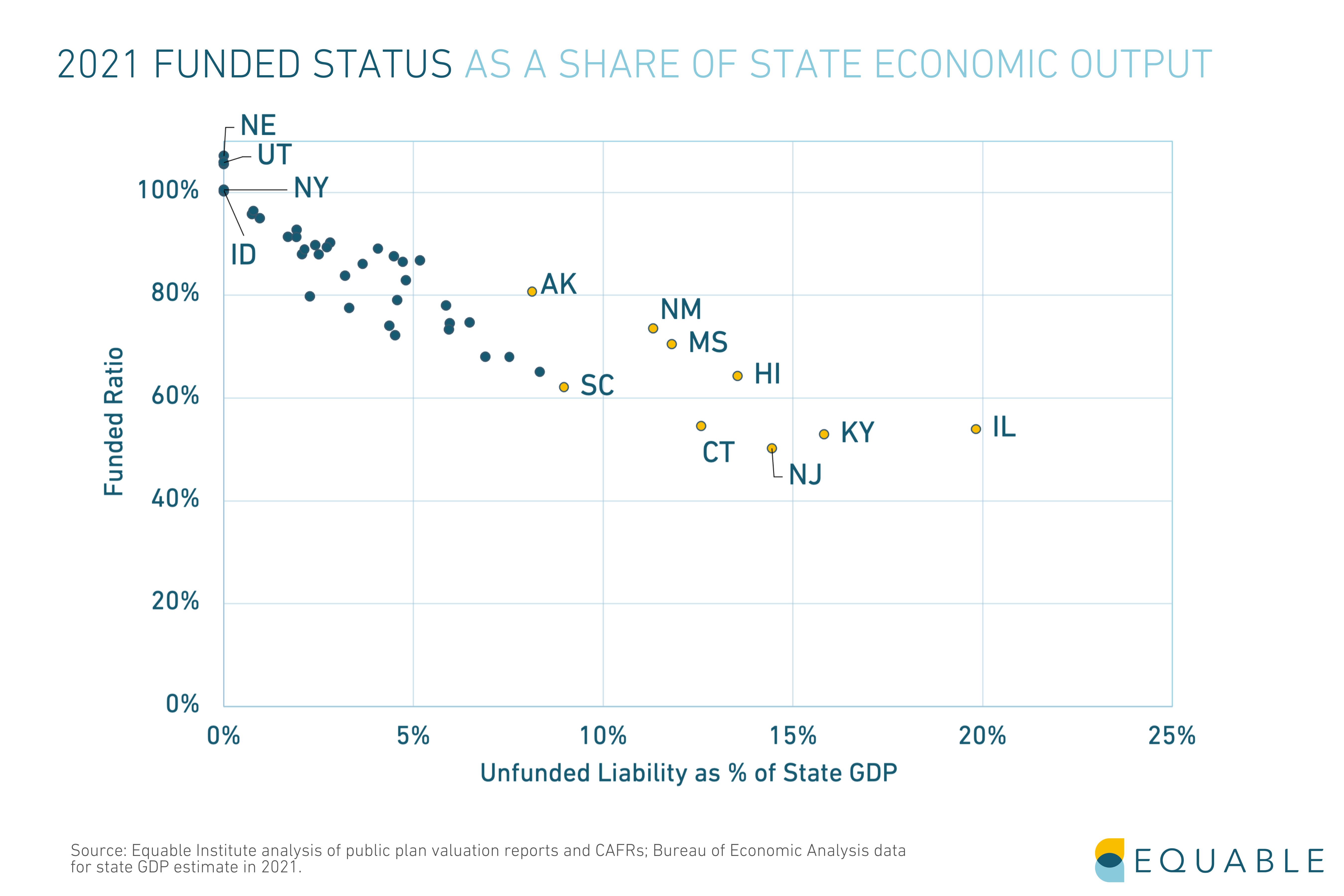

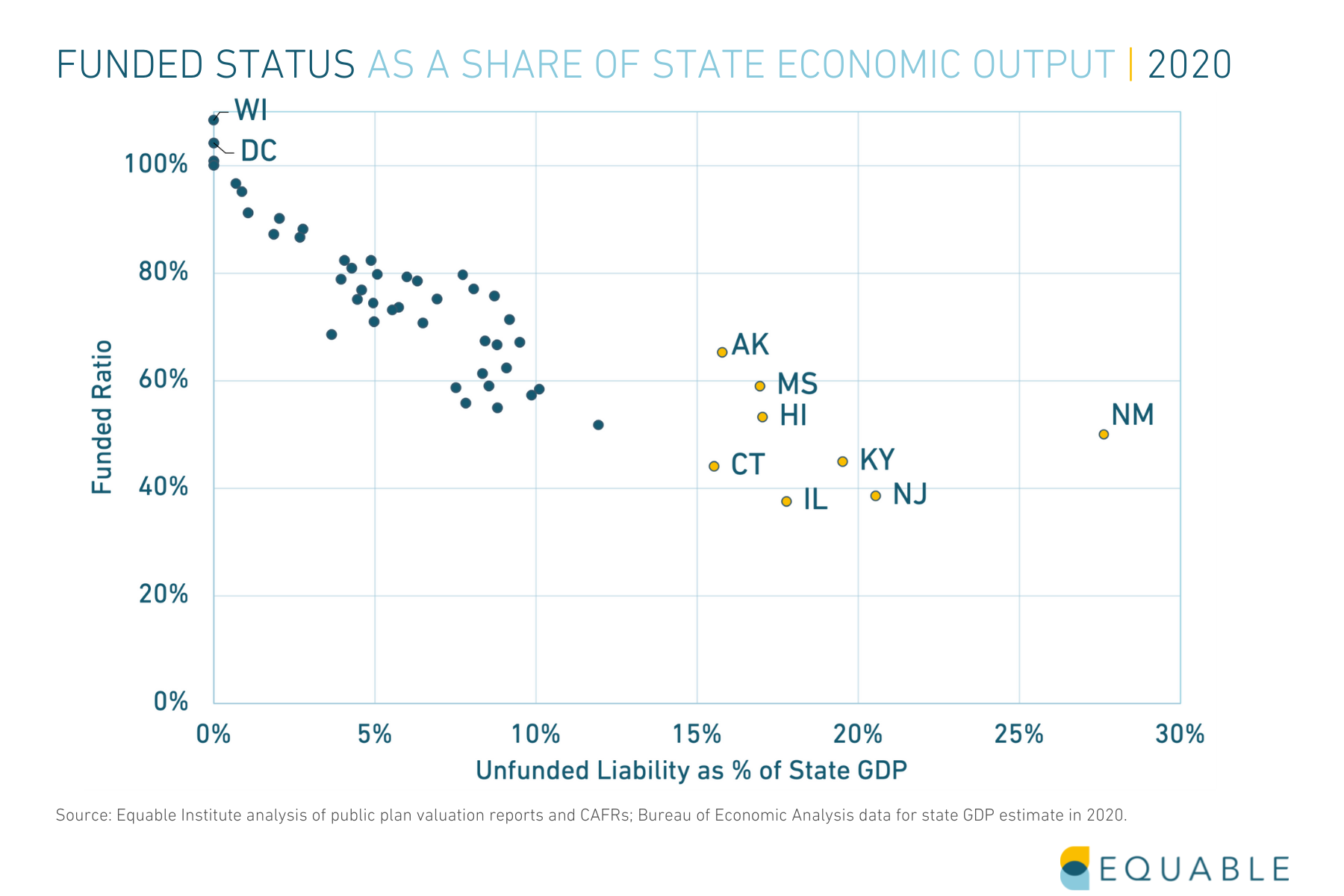

The funded ratio and pension funding shortfall are not the sole indicators of the health of a pension plan, however. Understanding the size of unfunded liabilities relative to the size of a state’s economy gives a sense of the scale of resources needed from a local tax base to improve pension funded status.

Prior to the pandemic, unfunded liabilities already accounted for a large share of many states’ GDPs. In our previous pension funding reports, we predicted the pandemic would lead to higher unfunded liability to GDP ratios. This is due to increasing funding shortfalls and economic contraction.

The chart below shows this for state totals and highlights how some states moved between 2021 and 2022.

How does pension debt impact states?

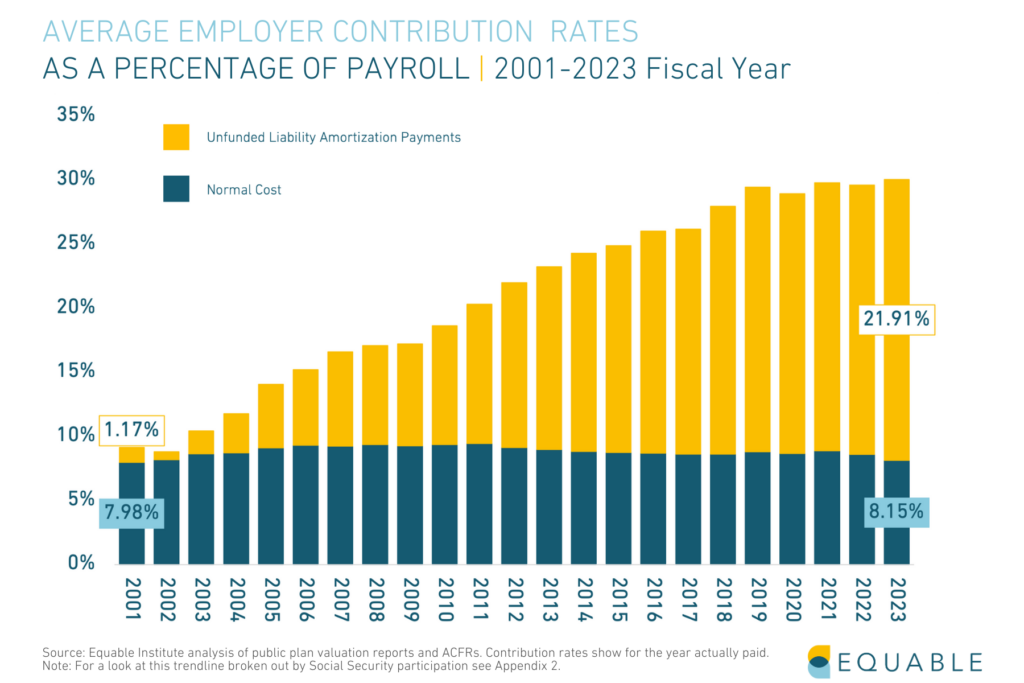

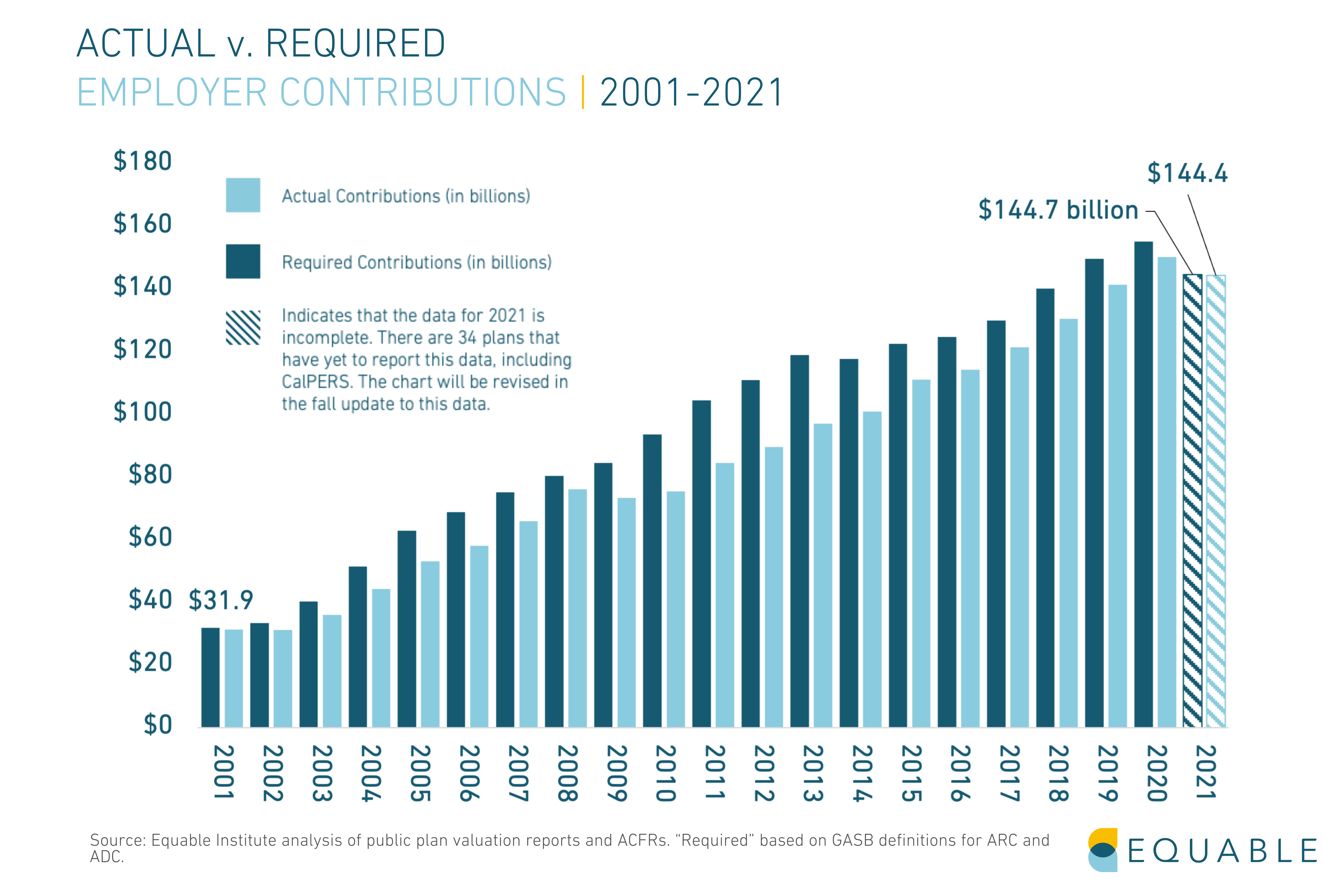

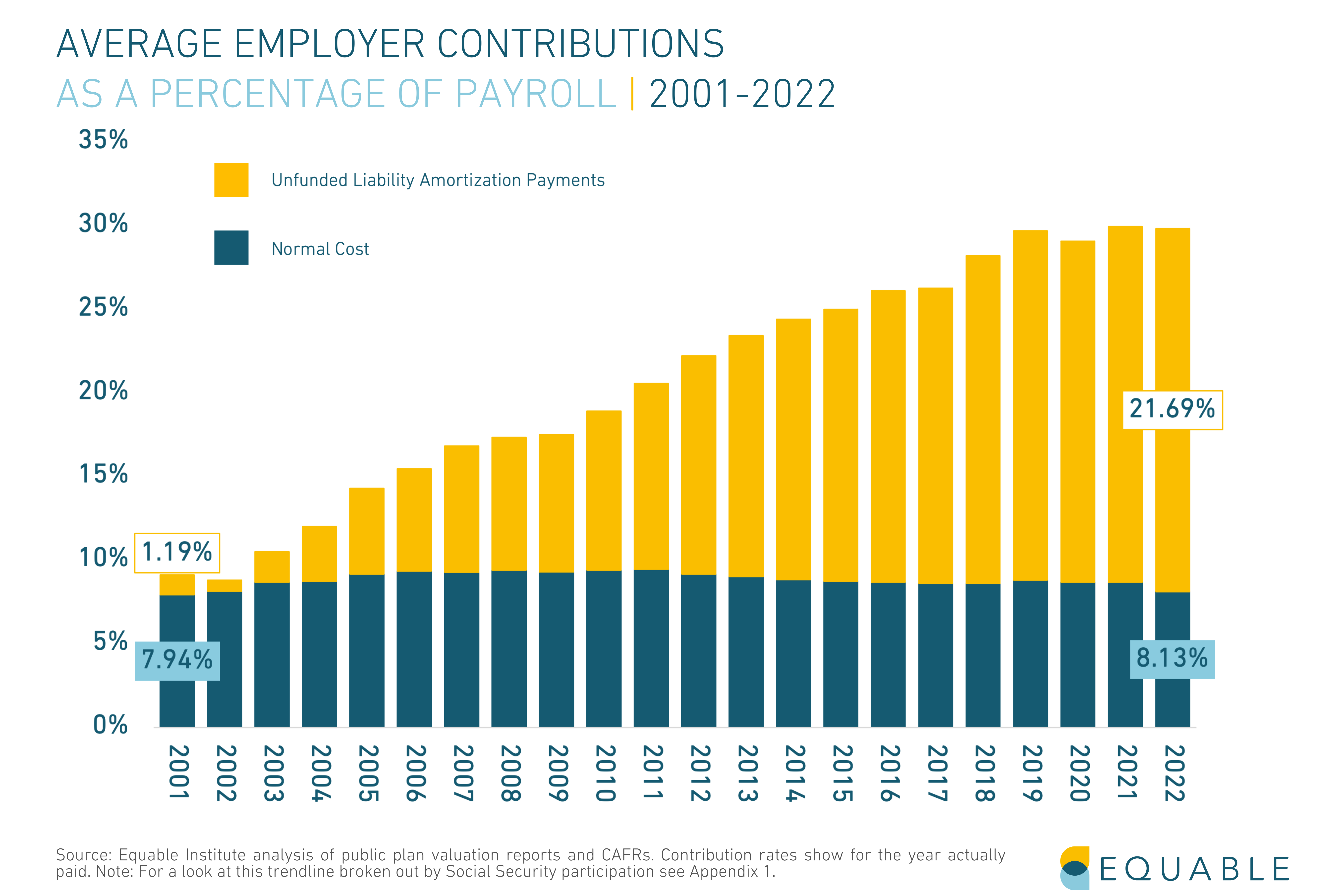

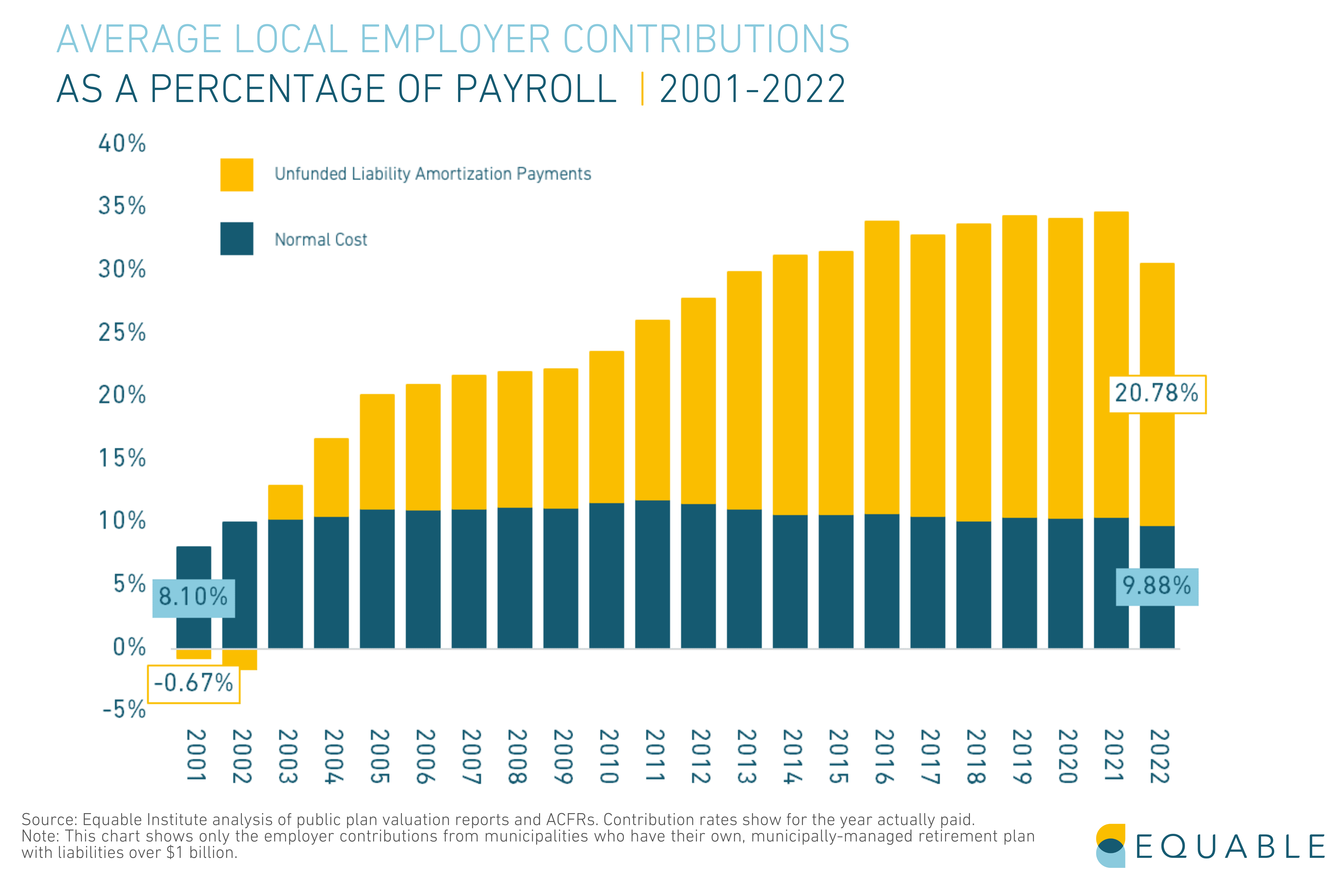

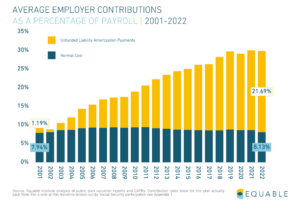

The growth of unfunded liabilities has made it significantly more expensive for states to provide public retirement benefits. In 2023, employer contribution rates reached an all-time high.

Government employer contributions have steadily increased over the past two decades, mostly because of increased payments to cover pension funding shortfalls (e.g., unfunded liability amortization payments).

Combined state and local employer contributions in 2001 were 9.15% of payroll. During the fiscal year ending 2023, employer contributions are 30.05% of payroll. In the chart above, you can see the normal cost of benefits has remained stable, while unfunded liability payments have grown exponentially.

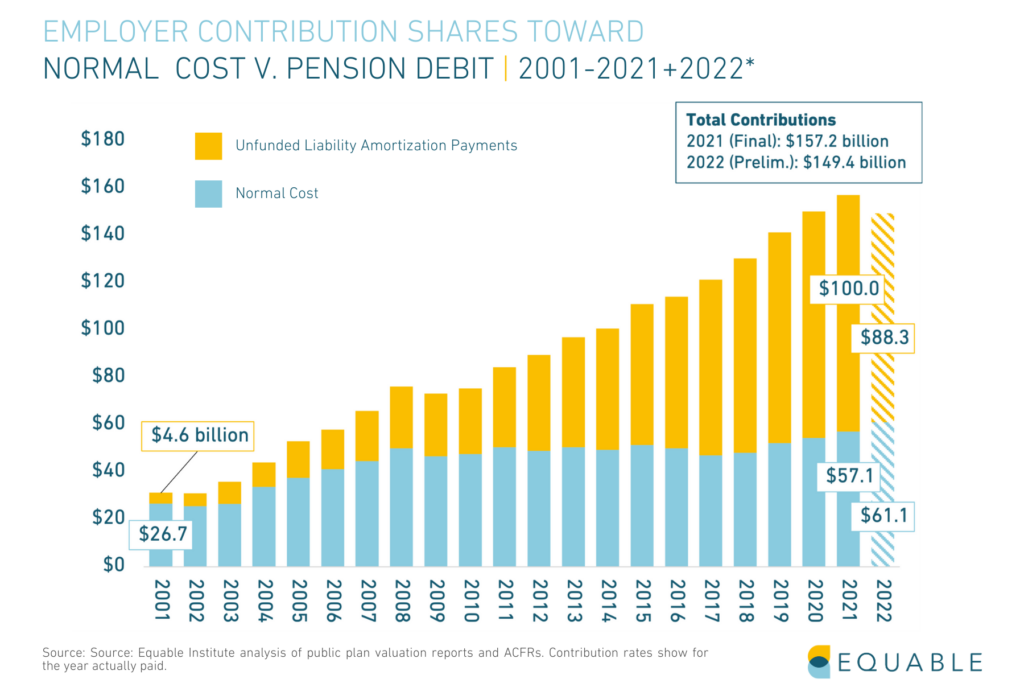

On a dollar basis, Unfunded liability payments however have risen 2,089% during the same two-decade period from under $4.6 billion in 2001 (or $7.6 billion, adjusted for inflation) to over $100 billion annually in 2021.

At the same time, the value of public retirement benefits have been decreasing. Pension debt has meant that both states and employees are paying more for less when it comes to retirement benefits.

How will underfunded pension funds cover promised benefits for workers?

There are three strategies that states might take in seeking to ensure they can pay promised benefits to workers:

- Increase contributions into their pension funds,

- Pursue higher investment returns, or

- Reduce the value of benefits.

Cutting benefits is unconstitutional in almost every state, but some places have still cut or reduced benefits. They do this by cutting back on the inflation change of pension checks.

Pursuing higher investment returns has been the primary strategy of the past decade. While a few state pension plans were able to recover and some years produced good returns, overall investment returns have not been high enough for everyone to recover.

States will continue using this strategy, but it has high risks. And if it doesn’t succeed that leaves only the other two strategies.

The other key strategy is increasing contributions. Usually, when unfunded pension liabilities rise steadily over the years, employer contributions experience an uptick along with required employee paycheck deductions. Throwing more money into state pension funds will not help state funding shortfalls. State's must address the underlying issues to make any meaningful impact. That means pension debt and employee contributions may rise unabated until a change in policy mandates a reversal of problematic practices. Even a boon in investment returns has historically offered no guarantee that state and local governments will make debt payments in a timely fashion.

Click Here to Read the Full State of Pensions 2023 Report

Pension Plan Funded Ratio Rankings 2022

U.S. public pension plan funded ratios at the end of 2022 reflect a challenging year. The 2022 calendar year was not a great time to be managing pension fund assets. A few hedge funds and money managers successfully navigated the choppy and volatile investment waters of 2022. However, most lost money. Some lost a lot of money.

The investment losses in 2022 didn’t wipe out all the funded status gains from 2021. Unfortunately, this year has – yet again – exposed the lack of resilience plaguing many public pension plans.

Once all public pension plans release their 2022 data, we estimate that unfunded liabilities will be $1.45 trillion. The combined funded status for the top state and local retirement systems will be 77.3%, based on available data through December 31, 2022. This is down from the 83.9% funded ratio during fiscal year 2021.

There’s no question that the aggregate funded status for public pension plans is mediocre. But, funded ratios and unfunded liabilities vary widely across states and plans. Below, we look at public pension funded ratios ranked by plan and by state.

State of Pensions 2022 Year End Update | State Funded Status Rankings | Plan Funded Status Details

The Top 10 Plans by Funded Status for 2022

There are some common themes among the best funded pension plans as of fiscal year 2022. Recently designed plans with cost-sharing components, plans with risk-sharing tools, and legacy plans with a multi-decade history of strong funded status all fared well.

| wdt_ID | Rank | Plan Name | Funded Ratio | Unfunded Liabilities | Notes |

|---|---|---|---|---|---|

| 1 | 1 | Washington LEOFF Plans 1 & 2 | 126.60% | 5,586,311,168.00 | These two pension plans have both been around 100% funded or better since the 1990s. |

| 2 | 2 | Michigan PSERS Pension Plus Plans 1 & 2 | 121.70% | 317,528,608.00 | These are risk-sharing hybrid plans. The Pension Plus Plan opened to new members in July 2010. The PPP2 was created for members starting February 2018 with a 6% max assumed return and 50/50 cost-sharing rules. |

| 3 | 3 | Tennessee Teachers Hybrid Plan | 119.50% | 116,868,544.00 | This is the hybrid plan for Tennessee teachers that launched in July 2014. |

| 4 | 4 | Detroit Police & Fire Component 1 | 112.80% | 31,286,768.00 | This is a new hybrid plan created for members hired since July 2014 (about a quarter of members) |

| 5 | 5 | Tennessee Teachers Legacy Plan | 109.50% | 2,639,685,632.00 | This is a legacy pension plan in Tennessee that closed to new members since 2014. |

| 6 | 6 | New York City Board of Education | 108.90% | 540,272,128.00 | This is a pension plan for board of education officials. |

| 7 | 7 | D.C. Police and Fire Plan | 107.70% | 506,743,808.00 | This pension plan has been considered fully funded for the past several decades. |

| 8 | 8 | Nebraska PERS Cash Balance Plan | 107.40% | 149,662,848.00 | This is a guaranteed return plan that has been open to new members since January 2003. |

| 9 | 9 | Arizona PSPRS Tier 3 | 107.20% | 10,855,456.00 | This is a risk-sharing pension plan that was created for new public safety members as of July 2017. |

| 10 | 10 | Washington PERS Plans 2 & 3 | 106.70% | 3,708,780,544.00 | These are a pension and hybrid plan that employees are offered a choice of membership in when joining. |

| Rank | Plan Name | Funded Ratio | Unfunded Liabilities | Notes |

The Bottom 15 Plans by Funded Status for 2022

The worst funded pension plans are largely from Illinois, New Jersey, Connecticut, and Kentucky. Among the worst are a few plans funded on a pay-as-you-go basis. Here are the 15 worst pension plans by funded ratio.

| wdt_ID | Plan Name | Funded Ratio | Unfunded Liabilities | Notes |

|---|---|---|---|---|

| 1 | Illinois JRS | 46.60% | 1,666,196,736.00 | Illinois pension plan. |

| 2 | Connecticut SERS | 45.60% | 22,124,845,056.00 | |

| 3 | Chicago Teachers | 45.30% | 14,190,124,032.00 | Illinois pension plan. |

| 4 | Illinois SERS | 43.50% | 33,301,098,496.00 | Illinois pension plan. |

| 5 | Chicago Laborers** | 42.90% | 1,706,322,304.00 | Illinois pension plan. |

| 6 | Illinois TRS | 42.80% | 83,840,331,776.00 | Illinois pension plan. |

| 7 | Dallas Police and Fire* | 42.20% | 3,041,735,168.00 | |

| 8 | New Jersey Teachers Pension Annuity | 37.40% | 47,929,602,048.00 | |

| 9 | Arizona Elected Officials | 32.00% | 675,132,992.00 | This plan was not fully funded after it was closed to new members. |

| 10 | Indiana Teachers Pre-96 Plan | 28.40% | 10,067,401,216.00 | This plan is using a pay-as-you-go funding model. |

| Plan Name | Funded Ratio | Unfunded Liabilities | Notes |

*Estimate based partially on reported preliminary returns and partially on asset allocation and benchmark returns.

**Estimate based on asset allocation and benchmark returns.

2022 Funded Status by State

A Full List of Plans by 2022 Funded Status

Pension Vesting Periods by State

In the U.S., public pension vesting periods vary widely by state. There are many reasons why states might offer longer or shorter vesting periods. But understanding the vesting terms of a public retirement plan can be a helpful metric for public employees to determine whether or not a retirement plan meets their needs.

In short, A vesting period is the amount of time an employee must work to qualify for retirement benefits. Retirement plan vesting periods are common in both the public and private sector. There are vesting rules for pension plans, defined contribution plans, guaranteed return plans, hybrid plans, and anything in between.

In this article, we will discuss how how vesting periods have changed over time for U.S. public retirement plans and provide a list of the current pension vesting periods by state, along with vesting periods for other types of public retirement plans.

JUMP TO: Vesting Periods by State

What is “Vesting”?

The minimum number of years a state or local employee needs to work in a state in order to be entitled to receive a pension benefit or the money their employer has contributed to their individual retirement account.

Why Government Employers Use Vesting Periods

The primary reason that employers give for having vesting periods is to help them with retaining staff talent. The basic logic is that people will stick around longer if they know they haven’t vested in their retirement benefits. While this logic may work for a small number of individuals who are within a few months of reaching their vesting period, in practice, the value of the retirement benefits available after just a few years are rarely sufficient to be a reason on their own for an employee to stay in civil service.

The political reality is that most state governments use retirement plan vesting periods as a way to save money. By setting vesting periods at 5, 7, or sometimes even 10 years, state governments are reducing the amount of future pensions they will have to distribute (or the employer payments to defined contribution plans they will have to release).

How Public Pension Vesting Periods Changed After the Financial Crisis

One of the ways that states responded to the Great Recession and Financial Crisis of 2007-09 was to look for ways to save money on retirement benefits. A common way that states have done this is to increase the number of years that public employees have to work to qualify for a pension.

For example, in Illinois, teachers and state workers hired before January 1, 2011 have to work four (4) years to order to vest in their pension benefits, whereas those hired from 2011 onward have to work eight (8) years.

Or in New York, public employees hired before January 2010 have a five (5) year vesting period to qualify for pension benefits while those hired after that point were, until recently, required to work 10 years to vest. Notably, in 2022, the New York state legislature reduced this vesting period back to five (5) years after a sustained campaign that demonstrated how problematic of a policy this was from the perspective of providing adequate retirement benefits to public workers.

The chart below shows the average vesting period over time for pension plans that are open to new members.

Public Pension Vesting Periods by State

Vesting periods range by state, hire date, and employee type. Vesting periods for teachers and public school employees average 6.4 years, while public safety officers have 8 year vesting periods on average. Pension plans for general civilian state and local employees average 6.9 year vesting periods.

The table below shows average public pension vesting periods by state, including data for traditional final average salary pensions, defined benefit guaranteed return plans, and hybrid plans that include a pension portion.

Defined Contribution Vesting Periods

The approach to vesting for defined contribution plans can sometimes look different than for pension benefits. In this context, employees are not vesting in the right to draw a pension check, instead they are vesting in the right to claim employer contributions made to individual accounts on their behalf.

A typical vesting period for defined contribution plans might look like this:

- After one year of service, a member has vested in 50% of the employer contributions made to their defined contribution account

- After two years of service, 75% vested

- After three years of service, 100% vested

This would be considered a three-year “graded” vesting period. Different states use a range of graded vesting period approaches. South Carolina immediately vests employees in their defined contribution benefits.

The table below lists the statewide defined contribution plans for public workers and the vesting approach that they use.

Pension Contributions by State 2022

Public pension contribution rates have increased considerably over the last few decades. Some governments have had sharper increases than others. In many places mandatory pension contribution rates for public employees have increased, too. So what is your state paying for public employee pension benefits?

Currently, the average pension contribution rate for state and local employers is 29.82%.

Employees enrolled in social security contribute 5.98% of their paycheck to their pension benefits, on average. While employees who are not offered social security contribute 8.07% on average.

In many states, pension contributions change from year to year and they may increase in 2023 and 2024. (Click here to see a version of this table with 2023 fiscal year data.)

It is important to keep in mind that states and cities do not uniformly participate in Social Security. Most individual government units do also enroll their employees in Social Security, but a few governments never opt-ed into the federal program. In theory, these non-participating locations should offer larger benefits and might have larger contribution rates.

The following charts show the average required contribution rates over time, broken out by state and locally administered plans, and whether or not members participate in Social Security.

Download the contribution rate data yourself from our database, including detailed break outs of what share of state pension contributions go toward normal cost and unfunded liability payments.

Current Assumed Rate of Return for State Pensions

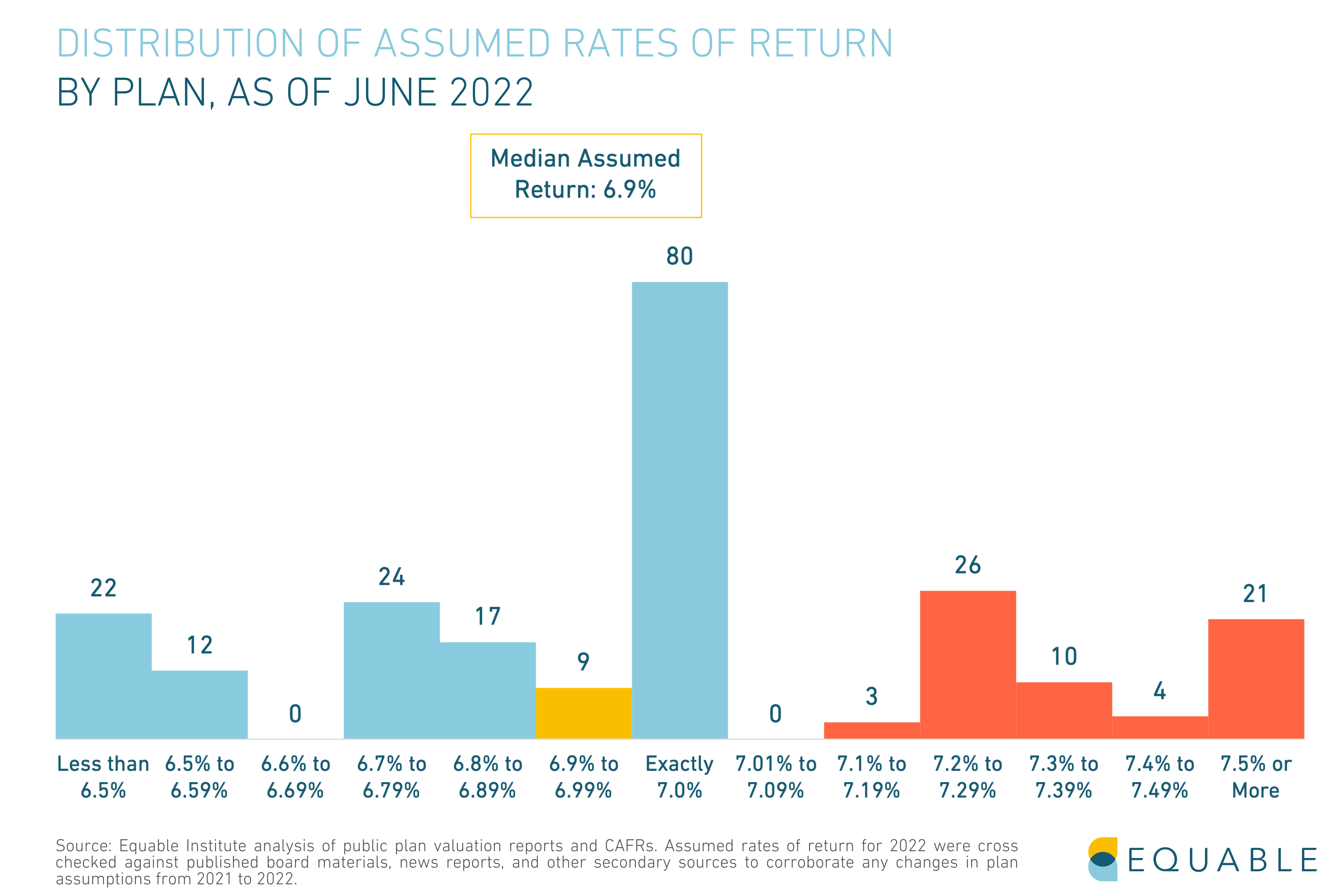

The average assumed rate of return for state pension plans in the United States is 6.9%, as of September 2022. The median is 7.0%.

Equable Institute tracks financial reporting for 231 defined benefit plans — e.g. pensions, guaranteed return, and hybrid plans — which are governed by 178 public sector retirement systems. Most of the plans are state administered, but our data also includes information for the 61 largest municipally-sponsored defined benefit plans in places like New York City, Chicago, Los Angeles, Houston, Orange County, Miami, and more.

Jump to the data | Learn more about the Assumed Rate of Return

*Article updated as of October 28th, 2022

Equable Analysis: Public Pensions Are Progressing Toward Lower Investment Assumptions

There has been a slow trend since the financial crisis of 2008-09 toward lower investment assumptions from public plans. Assumed rates of return were averaging 8% when the Great Recession hit. In the past two years have fallen below 7%.

This is generally good news. Over the last two decades the single largest contributor to the growth in unfunded liabilities has been underperforming investments. That is, states, cities, and counties were assuming unrealistic returns on their pension assets and by extension weren’t contributing enough to pay for promised benefits.

The current average of 6.9% is still overly optimistic for state and local pension funds. However, that average is likely to continue declining in coming years. New York State’s Common Fund — which manages assets for state agency workers, upstate cities, and public safety — is the third largest pension fund in the country, and last year lowered their assumed rate of return to 5.9%. The nation’s largest pension fund CalPERS lowered their investment assumption to 6.8% in 2021, and internal advisors have said they should be targeting 6%.

Distribution of Investment Assumptions, as of June 2022

The figure below shows the current distribution of assumed rates of return for the top state and local defined benefit plans.

Assumed Rates of Return by Retirement System

The following table provides a list of plans and their current assumed return. For an expandable table with data about previous assumed returns, investment management, and notes about known future changes, click here.

This table will be updated periodically as state plans announce changes to their assumed return via press release indicating that a board of trustees has voted to make a change, or when such a change is reported in a published actuarial valuation report.

What are the Historic Investment Assumption Trends?

State pension plans have adopted a wider range in assumptions over the past two decades. The lowest rate adopted by any plan open to new members is 5.25%. The highest rates currently used for a municipal plan is 8.25% (by Chicago Transit Authority) and for a state plan is 7.75% (by Mississippi).

States and pension boards have been slower than they should have to reduce their investment assumptions. The growing gap between interest rates and assumed rates of return reflects as an increased amount of risk that pension funds accept. If assumptions had kept pace with declining interest rates since 2001, the average assumption in 2022 would have been around 5.47%.

Why are Assumed Rates of Return Important?

Assumed rate of return is the single most important assumption that pension systems. This assumption ensures they have enough funding to pay benefits promised. A pension fund and its actuaries make educated guesses about how much they think they can earn by investing contributions. That educated guess is called the assumed rate of return. The higher the assumed rate of return, the fewer contributions teachers and their employers have to make. The lower the assumed rate of return, the higher contributions need to be in order to pay for the benefits promised. Read more about this important investment assumption in our Pension Basics series.

Teacher Pension COLAs in 2022

A key feature of teacher pension plans is that they offer guaranteed income for life. But unless the purchasing power of that pension income keeps up with inflation, the guarantee doesn’t necessary provide ensured financial security. That is why many defined benefit pensions for teachers come with cost-of-living adjustments, or COLAs.

However, just because there are many plans with COLAs doesn’t mean there is widespread protection from inflation.

The average COLA provided by teacher pension plans this year has been 1.8%.[1] This is effectively the same as the average cost-of-living adjustment offered to all public pension plan retirees.

The 1.8% figure is well below most measures of actual price inflation in 2022. That is because many COLA policies do not exactly match inflation. Instead COLA rules have maximum rates (e.g., increasing at the rate of inflation up to 2%) or they are linked to other factors (e.g., a 2% COLA, but only if the pension fund for base benefits has adequate resources).

There are some reasonable financial reasons for these rules. Some years retired teachers get COLAs that are actually larger than inflation. However, the net effect in 2021 and 2022 has been that public pension COLAs frequently are less than inflation.

Teacher pension COLAs vary in how much inflation protection they provide, and in who gets the benefit adjustments. In this article, we explain some of the different kinds of cost-of-living adjustments provided to retirees from public employee pension funds.

First, here is a list of teacher pension plans and classes of benefits and the COLAs they’ve provided in 2022.

Not all teacher pension COLAs are created equal. If you are trying to determine whether or not a COLA is adequate enough to maintain the spending power of your retirement benefits, you should consider the following elements of your plan’s COLA policy:

1. Compounding versus Non-Compounding Benefits

Retirement funds have two ways of adjusting underlying benefits when paying out teacher public pension COLAs.

Compounding Benefits: Retirement funds permanently adjust the base benefit and add any any future changes to benefits on top.

For example, someone with a $40,000 pension that gets a 2% COLA will have their base benefit increased to $40,800. The next year, if inflation means a 1.5% COLA, then the adjustment is calculated based on the new, higher number. So in this case, the benefit would increase to $41,412.

Non-Compounding Benefits: This means that all inflation adjustments are based on the original pension benefit value. Each year benefits increase, you get to keep the adjustment from the previous year. But, the percentage increase is based on your original pension.

For example, a former teacher with a $40,000 pension that got a 2% COLA would see $800 added on top for a total pension of $40,800. The next year, a 1.5% COLA would be calculated on the original $40,000 pension. $600 would then be added on top for a total pension of $41,200.

2. Three Types of Automatic Public Pension COLAs

There are generally three policy frameworks for those teachers who do have automatically granted COLAs that protect public worker pensions from inflation:

- Fixed-Rate COLAs: A pre-fixed specific percentage of benefit increase (or minimum dollar amount).

- COLAs Linked to Inflation: A percentage increase to benefits based on the national consumer price index (CPI), a local CPI, or the Social Security inflation rate. The actual amount is typically “up to” a maximum rate, such as 2% or 3%.

- COLAs Linked to Plan Performance: A percentage increase to benefits that is dependent on the funded ratio and/or investment performance of the underlying pension plan. The actual amount is also typically “up to” a maximum rate, but that maximum rate is determined by the specific provisions around plan performance. For example, the maximum COLA rate may be cut in half or suspended if the pension fund is under 80%.

Some state pension funds have inflation adjustments linked to both inflation and pension plan performance.

3. Ad Hoc Cost-of-Living Adjustments

There are a number of teacher pension plans that do not provide consistent inflation protection. Some of these states have no legal provisions to offer COLAs. Other states only payout COLAs if the legislature authorizes the benefit adjustment. Because COLAs are not legally required in these states, they are called “ad hoc” COLAs. These COLAS are also heavily dependent on local politics and legislative budgets.

Note [1]: This is an average of 158 classes of defined benefits, including actual reported percentage rates adjusting benefits starting in the 2022 calendar year and percentage rates based on published COLA policies.

Teacher Pension COLAs in 2022

A key feature of teacher pension plans is that they offer guaranteed income for life. But unless the purchasing power of that pension income keeps up with inflation, the guarantee doesn’t necessary provide ensured financial security. That is why many defined benefit pensions for teachers come with cost-of-living adjustments, or COLAs.

However, just because there are many plans with COLAs doesn’t mean there is widespread protection from inflation.

The average COLA provided by teacher pension plans this year has been 1.8%.[1] This is effectively the same as the average cost-of-living adjustment offered to all public pension plan retirees.

The 1.8% figure is well below most measures of actual price inflation in 2022. That is because many COLA policies do not exactly match inflation. Instead COLA rules have maximum rates (e.g., increasing at the rate of inflation up to 2%) or they are linked to other factors (e.g., a 2% COLA, but only if the pension fund for base benefits has adequate resources).

There are some reasonable financial reasons for these rules. Some years retired teachers get COLAs that are actually larger than inflation. However, the net effect in 2021 and 2022 has been that public pension COLAs frequently are less than inflation.

Teacher pension COLAs vary in how much inflation protection they provide, and in who gets the benefit adjustments. In this article, we explain some of the different kinds of cost-of-living adjustments provided to retirees from public employee pension funds.

First, here is a list of teacher pension plans and classes of benefits and the COLAs they’ve provided in 2022.

Not all teacher pension COLAs are created equal. If you are trying to determine whether or not a COLA is adequate enough to maintain the spending power of your retirement benefits, you should consider the following elements of your plan’s COLA policy:

1. Compounding versus Non-Compounding Benefits

Retirement funds have two ways of adjusting underlying benefits when paying out teacher public pension COLAs.

Compounding Benefits: Retirement funds permanently adjust the base benefit and add any any future changes to benefits on top.

For example, someone with a $40,000 pension that gets a 2% COLA will have their base benefit increased to $40,800. The next year, if inflation means a 1.5% COLA, then the adjustment is calculated based on the new, higher number. So in this case, the benefit would increase to $41,412.

Non-Compounding Benefits: This means that all inflation adjustments are based on the original pension benefit value. Each year benefits increase, you get to keep the adjustment from the previous year. But, the percentage increase is based on your original pension.

For example, a former teacher with a $40,000 pension that got a 2% COLA would see $800 added on top for a total pension of $40,800. The next year, a 1.5% COLA would be calculated on the original $40,000 pension. $600 would then be added on top for a total pension of $41,200.

2. Three Types of Automatic Public Pension COLAs

There are generally three policy frameworks for those teachers who do have automatically granted COLAs that protect public worker pensions from inflation:

- Fixed-Rate COLAs: A pre-fixed specific percentage of benefit increase (or minimum dollar amount).

- COLAs Linked to Inflation: A percentage increase to benefits based on the national consumer price index (CPI), a local CPI, or the Social Security inflation rate. The actual amount is typically “up to” a maximum rate, such as 2% or 3%.

- COLAs Linked to Plan Performance: A percentage increase to benefits that is dependent on the funded ratio and/or investment performance of the underlying pension plan. The actual amount is also typically “up to” a maximum rate, but that maximum rate is determined by the specific provisions around plan performance. For example, the maximum COLA rate may be cut in half or suspended if the pension fund is under 80%.

Some state pension funds have inflation adjustments linked to both inflation and pension plan performance.

3. Ad Hoc Cost-of-Living Adjustments

There are a number of teacher pension plans that do not provide consistent inflation protection. Some of these states have no legal provisions to offer COLAs. Other states only payout COLAs if the legislature authorizes the benefit adjustment. Because COLAs are not legally required in these states, they are called “ad hoc” COLAs. These COLAS are also heavily dependent on local politics and legislative budgets.

Note [1]: This is an average of 158 classes of defined benefits, including actual reported percentage rates adjusting benefits starting in the 2022 calendar year and percentage rates based on published COLA policies.

Is There a Pension Crisis in the US?

Is there a state pension crisis in the United States?

The short answer is no. Despite headlines claiming that state pension funds are in trouble, there is no widespread crisis of public pension plans facing the prospect of near-term insolvency or bankruptcy.

However, there are many states and pension plans that face dire long-term sustainability challenges. These can come with serious ramifications if they continue to go unaddressed. There are many communities who are suffering today from the effects of unsustainable increases in costs for paying off pension debt.

That being said, a longer and more complete answer must define “crisis” in the context of state or local pension plans.

There is no shortage of commentators arguing that there is currently a US public pension crisis. Though exactly what that crisis might be depends on who you ask.

Some have said pensions will soon go bankrupt. Others have said pensioners (or retirees) are at risk of plunging into poverty. While others have focused on investment mismanagement of pension assets. Often the concept of a “pension crisis” is mixed with a “retirement crisis.” The latter of which is a more general concern about if Americans are saving enough for retirement.

In this article, we break down some of the different metrics we use to measure the health of pension funds. We use actual data to determine whether or not there is a state pension crisis in the United States.

Ultimately, our assessment of the data shows there is no near-term “solvency” crisis for most state pension funds. However, there is a “sustainability” crisis in many states. Specifically, this “crisis” threatens states, cities, and counties where growing contribution rate requirements threaten a range of public services such as school programs, infrastructure programs, defenses against the effects of climate change, public housing programs, and more.

Ways to Define a Public Pension Crisis

There are multiple ways to think about whether a public defined benefit pension plan could be facing a “crisis”:

- Near-term Insolvency Crisis: Is the pension fund at risk of running out of money to pay benefits in the next 2, 5, or 10 years?

- Long-term Insolvency Crisis: Is the pension fund at risk of running out of money at some point in the future? Several decades from now, but still forecast to one day become insolvent/go bankrupt?

- Management Crisis: Are the pension fund’s trustees mismanaging assets? This includes using very risky investment strategies or paying out very high fees without a reasonable return.

- Retirement Crisis: Are retirees in general at risk of falling into poverty because of a lack of adequate pension benefits?

- Budgetary Cost Crisis: Are the costs of paying for the unfunded liabilities of pension plans “crowding out” or threatening other public goods and services?

- Sustainability Crisis: Are the costs of a pension fund growing so large as a share of government budgets or state GDP that future taxpayers are unlikely to be able to adequately provide funding to a pension plan?

What the Data Says: Public Pension Insolvency Concerns

First, let’s look at the financial data on the solvency of pension funds in the United States. In this context, a “solvent” pension fund is one that has enough money on hand to pay out all promised benefits for at least a year.

This isn’t a very high standard to meet. The lower the assets in a pension fund, the more likely it is at some point to become insolvent. But as long as there are assets, in theory, a pension fund can generate investments returns on their money. They can also continue to receive contributions from government employers and members.

So how many pension funds in America today at risk of near-term or long-term insolvency? Somewhere between 10% and 20% of the largest state and local pension plans in the United States are at risk.

That number is based on an estimate from a group of retirement policy experts using data from 2019. This group defined two levels of extreme risk for pension fund solvency:

- “Deep Red”: Projected to become insolvent in 20 years; AND the ratio of inactive to active participants is more than 2 to 1, OR the plan is less than 80 percent funded.

- “Red”: Received less than 100 percent of the actuarially determined contribution (ADC) over the past 5 years; AND the funded ratio is under 65 percent.

Plans Designated as Deep Red Zone or Red Zone

| wdt_ID | Plan Name | Risk Zone | Funded Ratio | Percent of ADC paid over prior 5 years | Ratio of active employees to beneficiaries | Ratio of contributions to normal cost plus UAAL interest | Ratio of Non- Investment Cash Flow to Beginning of Year Assets (%) |

|---|---|---|---|---|---|---|---|

| 1 | Arizona State Corrections Officers | Red | 52 | 84 | 88.00 | 0.77 | 68.00 |

| 2 | Charleston (WV) Firemen's Pension | Red | 13 | 78 | 264.00 | 86.00 | 462.00 |

| 3 | Chicago Fire | Red | 21 | 81 | 114.00 | 92.00 | 410.00 |

| 4 | Chicago Police | Red | 24 | 73 | 116.00 | 83.00 | 21.00 |

| 5 | Chicago Teachers | Red | 48 | 90 | 126.00 | 80.00 | -479.00 |

| 6 | Colorado School | Red | 63 | 81 | 75.00 | 82.00 | -344.00 |

| 7 | Colorado State | Red | 61 | 83 | 93.00 | 83.00 | -434.00 |

| 8 | Denver Employees | Red | 62 | 99 | 155.00 | 101.00 | -305.00 |

| 9 | Hawaii ERS | Red | 58 | 86 | 90.00 | 82.00 | -115.00 |

| 10 | Illinois SERS | Red | 41 | 83 | 127.00 | 89.00 | -65.00 |

| Plan Name | Risk Zone | Funded Ratio | Percent of ADC paid over prior 5 years | Ratio of active employees to beneficiaries | Ratio of contributions to normal cost plus UAAL interest | Ratio of Non- Investment Cash Flow to Beginning of Year Assets (%) |

Source: Urban Institute

What the Data Says: Pension Management Crisis

A common concern for public pension plan is that they pay out too much in fees.

There is no question that this is a real concern. For example, a Pennsylvania state commission issued a report running nearly 400 pages to consider best practices and management of their statewide retirement systems. One of the key focuses of that report was the fees paid by the state’s pension plans. Another example is New York City, whose comptroller once found compelling data revealing that after accounting for fees, city pension plans were underperforming.

A related concern is that investment managers for pension funds adopt “bogus benchmarks” to measure themselves against. Every pension fund wants to measure how well its investments are performing. How they should do that is a subject of debate. However, every pension fund adopts a set of “benchmarks” to grade their performance against. Typically these benchmarks are widely available measurements of how other investors have performed or how financial markets as a whole have performed. For example, if the entire S&P 500 stock market index gained 5% but a specific pension fund gained 4%, then the fund underperformed relative to that benchmark.

The criticism leveled against state and local pension funds is that they choose benchmarks that are too easy to over perform against. This allows pension funds to avoid making important and difficult decisions about ways they could improve their investment strategy.

While there are reasonable concerns about both investment management fees and benchmarking policy, are these creating a “crisis” for pension funds? It depends on how broadly the word “crisis” should be used. In general fees are not the reason that pension funds have a more than $1 trillion funding shortfall, as of 2022 data.

Equable analyzed the sources of unfunded liabilities accumulated between 2000 (when state and local pension plans were last effectively fully funded on average) and 2019 (before the pandemic). We found that 41% of their reported unfunded liabilities were from underperforming investments, after accounting for fees.

Put another way, pension funds over the past two decades assumed that they could earn investment returns between 7% and 8% a year on average. But they didn’t. And the underperformance against this expectation created over $567 billion in pension debt between 2000 and 2019 for the largest state pension plans. So if there is a “management crisis” for pension funds it is the use of unrealistic assumed rates of return.

For example:

The chart below shows the average assumed rate of return for state and local pension funds over the past two decades (the light blue line). For comparison, we also show how interest rates have changed over the same period, whether considering the 10-year treasury yield (yellow line) or 30-year yield (dark blue line).

The difference between interest rates and the assumed rate of return reflects how much pension funds think they can get by taking risks with their investments beyond just buying perfectly safe U.S. Treasury bonds. If pension funds had maintained a consistent attitude toward their risk as they did back in 2001, then the average assumed rate of return in 2022 should be somewhere around 5.5% (see the dashed light blue line). However, the trustees managing state pension funds have taken on more risk with their investments. They have adopted unrealistic assumed rates of return on those investments, all in order to keep their costs down. If there is a “crisis,” it is there.

What the Data Says: Public Retirement Crisis

Are people saving enough for retirement? Recent analysis of retirement savings for private sector individuals who don’t have pensions suggests that they might not be. There are some common counter arguments to this concern that point out Social Security benefits are actually better than many people understand, particularly for retirees on the poverty line. And Social Security benefits are set to receive a very large inflation adjustment in the coming year.

However, the general concerns about a “retirement crisis” that get circulated in the media are almost uniformly about the private sector. There is very little concern about retirement income values for those who have a public sector pension.

There is no “crisis” of retirement income values for public sector retirees. But, that doesn’t mean there are no reasonable concerns. Equable recently analyzed the value of retirement plans for new teachers, and found that since 2005 states have systematically cut the value of pension benefits for new hires.

What the Data Says: State Budget Cost Crisis

If there is any “crisis” for pension plans, it starts with the costs of paying for growing unfunded liabilities. State and local pension funds reported more than $1 trillion in unfunded liabilities in 2020. They reported just under $1 trillion in funding shortfall for 2021. Once 2022 numbers are formally reported, the unfunded liabilities for pension funds will be back over the $1 trillion mark. Reaching this point has meant higher costs for states, cities, and school districts.

The figure below shows the contribution rates paid by government employers.

Note that the driving factor is a growth in payments toward unfunded liabilities.

These growing costs have a real effect. Consider the growth in costs for teacher pension benefits. Equable found that between 2001 and 2018 the share of state education K–12 budgets that were used to pay pension costs increased from 7.5% to 14.4%. This has meant fewer resources for schools and students. In California, school board members reported cutting arts and music programs, taking out loans, delaying school building upgrades or technology purchases, and increasing class sizes. Growing teacher pension costs are explicitly cited as the reason for these cuts.

That means pension costs are influencing education quality, programs, and experiences for students right now. That probably qualifies as a “crisis.”

This isn’t the case in every state. Some states have very low pension costs relative to their K–12 budgets. Other states have managed to increase their education budgets even as pension costs have grown. But nationally, there is a problem with increasing “crowd out” of education funding by teacher pension costs. This is because legislatures failed to ensure students are held harmless as teacher pension unfunded liabilities have increased.

What the Data Says: Sustainability Crisis

Measuring the fiscal health of a retirement system is a complex project. As we’ve written elsewhere: we define financially healthy, sustainable retirement systems as those that are both resilient and affordable.[2] Resilience matters because for governments to thrive and be effective. They need their programs and services to be prepared for negative shocks and tail risk events. Public sector retirement systems should not be prone to significant destabilization due to external factors, mismanagement, or political whims. Further, retirement systems should be able to adapt to changing economic and demographic conditions in both the short- and long-term. They should not be designed in ways that allow threats to build over time, to threaten the retirement security of members, or to impede the fiscal stability of their sponsoring government’s budgets.

Measuring pension plan sustainability means looking at both solvency metrics over time (funded ratios and unfunded liability levels). Costs of providing the retirement plan relative to existing tax revenues should be looked at as well. The larger required pension payments are relative to the size of state budgets, the harder it is for the state to ensure responsible funding policies. This is because of the higher cost burden. If such costs are growing because of consciously made policies that set benefit levels in a known way with clearly allocated resources to pay them, this might not be a problem. When larger payments are required because unfunded liabilities are growing, that represents a funding threat.

Here is a multi-factor framework for determining which the status of a retirement system.

There are five factors that we consider in setting this measurement:

- Funded Ratio (Funded Status)

- Unfunded Liability as a % of GDP (Ability to Pay)

- Assumed Rate of Return (Underperformance Risk)

- Share of Required Contributions Received (Willingness to Pay)

- Risk-Sharing Tools (Future Flexibility)

In Equable’s most recent State of Pensions 2022 report, we look at each of these metrics.

The following figure shows the number of retirement systems with “resilient,” “fragile,” or “distressed” funded ratios . We also show different states stack up on their unfunded liabilities as a percentage of state GDP in the next chart.

The good news is there are not many distressed pension plans relative to the rest of the country’s large state and local pension plans.

States with unfunded liabilities over 10% of GDP should be concerned. But, most are not in a place on this metric to be concerned about a “crisis.”

However, these charts do show that there are considerable unfunded liabilities to be addressed. Most pension funds are fragile and could fall into a distressed category if there is a particularly bad set of financial shocks that hit their balance sheets hard. Even if pension funds stay fragile, they have large costs for maintaining those unfunded liabilities, which we just discussed in section 5 of this article.