The average assumed rate of return for state pension plans in the United States is 6.9%, as of January 2026. The median is 7.0%.

Equable Institute tracks financial reporting for 264 defined benefit plans — e.g. pensions, guaranteed return, and hybrid plans — which are governed by 202 public sector retirement systems. Analyses are limited to 253 of those plans due to incomplete reporting and data availability issues. Of the plans included in analyses, most are state-administered, but our data also include information for 78 of the largest municipally sponsored defined benefit plans in places like New York City, Chicago, Los Angeles, Houston, Orange County, Miami, and more.

Equable Insight

All data as of January 2026.

- Average ARR: 6.9%

- Median ARR: 7.0%

- Average 2025 Return: 9.5%

What is Assumed Rate of Return?

The assumed rate of return is an educated guess about how much a pension can reasonably expect to earn in the long term by investing contributions made to the plan.

A plan’s ARR is calculated by actuaries, who are financial professionals that measure risk and other factors in order to estimate how much a retirement system must bring in from contributions and pay out in the form of benefits each year.

Why is Assumed Rate of Return Important?

Assumed rate of return is the single most important assumption that pension systems make within the overall pension funding formula. Once it’s set by the pension board, the ARR allows actuaries to determine the level of annual contributions that are necessary to pay in advance for all of the benefits earned in that year.

The higher the assumed rate of return, the fewer contributions teachers and employers have to make. The lower the assumed rate of return, the higher contributions need to be in order to pay for the benefits promised.

In short, ARR is important because it ensures pension systems have enough funding to pay their promised benefits.

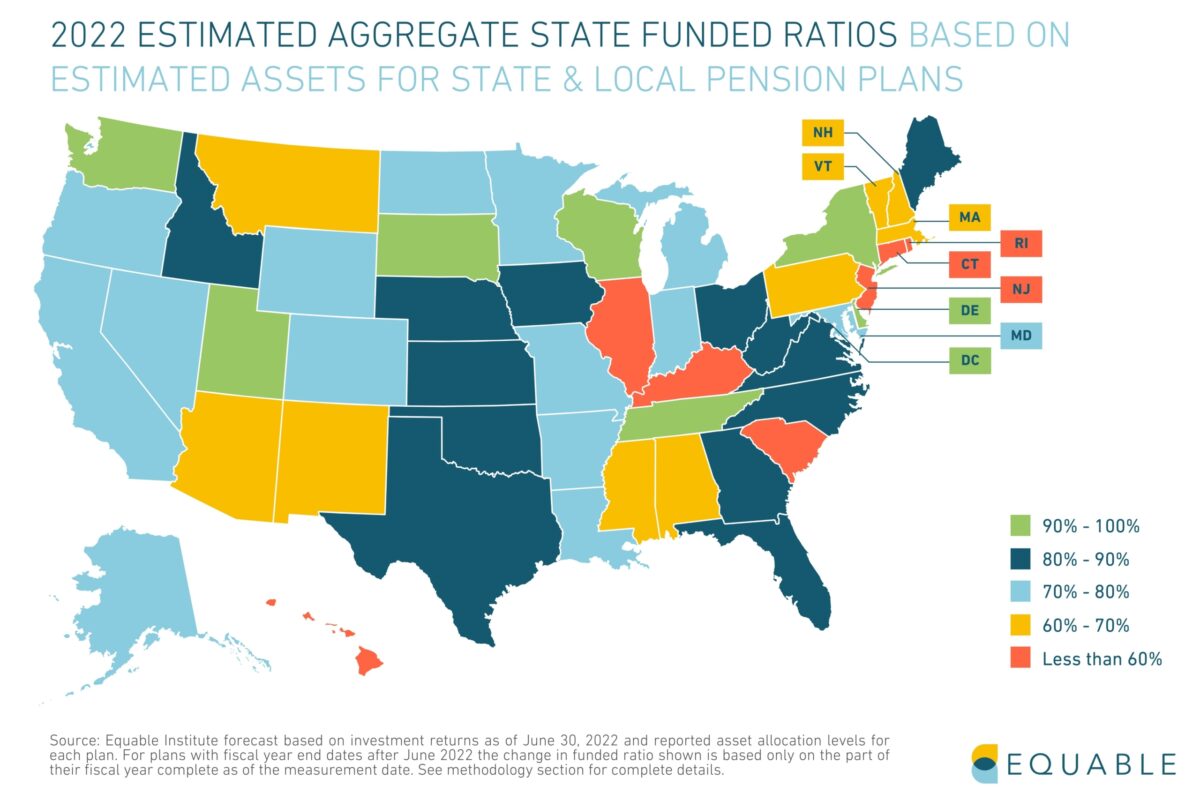

Assumed Rates of Return by State

The graphic below details the median assumed rate of return for each state, as of 2025, using data from those state and local retirement plans.

Assumed Rates of Return by Retirement System

The following table provides a list of plans and their current assumed return. Use the search function or scroll through each page to find figures for your plan.

This table will be updated periodically as state plans announce changes to their assumed return via press release indicating that a board of trustees has voted to make a change, or when such a change is reported in a published actuarial valuation report.

Current Landscape: 2025 Public Pension Investment Assumptions

The latest data analyzed in Equable’s State of Pensions 2025 report show public pensions have progressed toward lower investment assumptions over time, particularly since the financial crisis of 2008-09.

Assumed rates of return averaged 8.1% when the Great Recession hit. As of January 2026, that figure sits at 6.9%.

This is generally good news. The unfunded liabilities that have plagued most public retirement systems since the early 2000s are the result of investments underperforming relative to assumptions during economic downturns like the Dot-Com Recession or the Financial Crisis. That is, states, cities, and counties assumed unrealistic returns on their pension assets and, by extension, weren’t contributing enough to pay for promised benefits.

However, even the current average of 6.9% is still overly optimistic for state and local pension funds, as we estimate that the average fund has less than a 50% chance to earn 7% over the next decade.

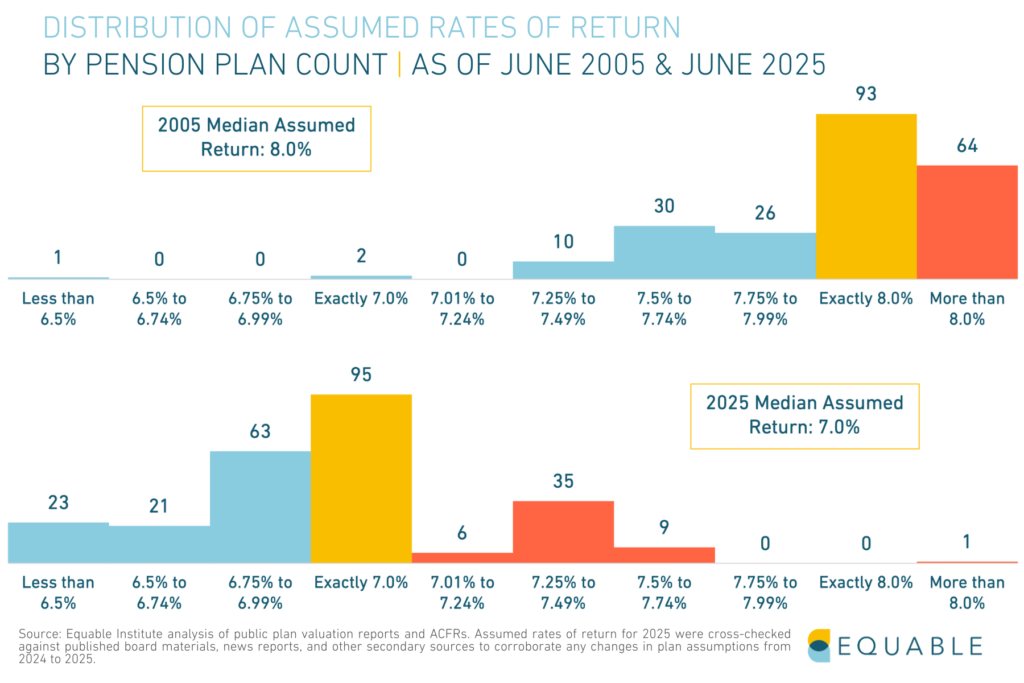

Distribution of Investment Assumptions in 2025

The figure below shows a long-term comparison between the distribution of assumed rates of return for the top state and local defined benefit plans in 2005 and 2025.

In June 2005, there were 223 major public pension plans with ARRs higher than 7%, including 64 with ARRs above 8%. Two plans assumed returns of exactly 7%, and just one plan had an ARR of 6.5% or less.

Since then, the distribution of assumptions has shifted significantly.

As of June 2025, just 51 plans have ARRs higher than 7%, including only one plan with an ARR above 8%. Meanwhile, 95 plans now assume returns of exactly 7%, and 63 plans have ARRs between 6.75% and 6.99%.

While 42 plans now have ARRs of 6.5% or less, a vast improvement since 2005, there are still 18 plans assuming future investment returns greater than 7.25%.

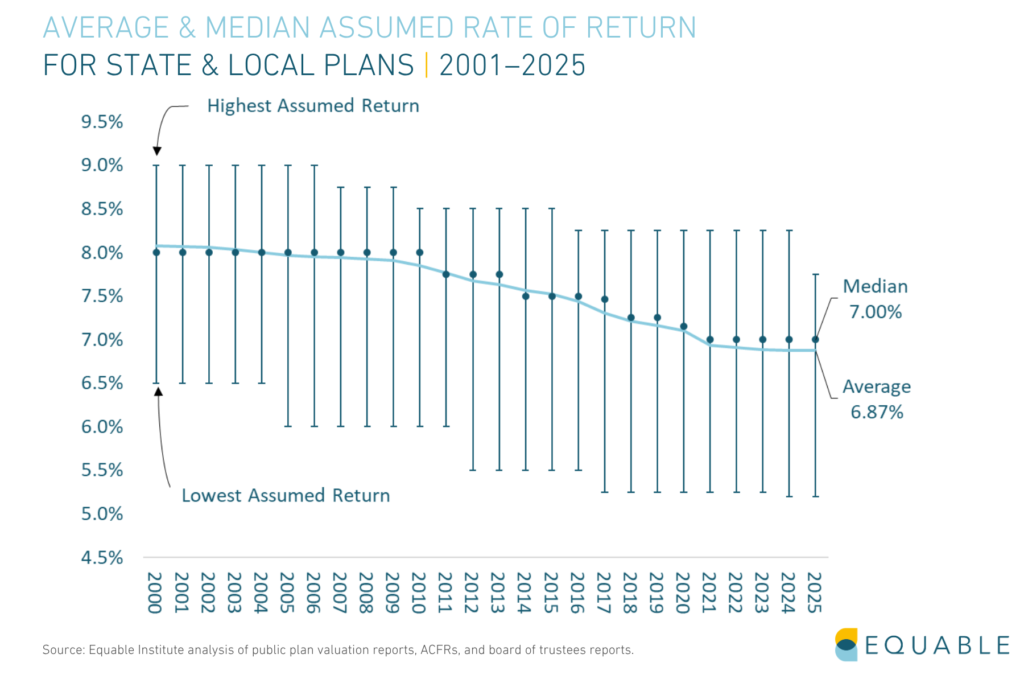

Historic Investment Assumption Trends

As noted, state and local pension plans have adopted a wider range of assumptions over the past two decades. The figure below shows the highest and lowest assumed rates of return in each year since 2000, as well as the median and average trend over time.

The lowest rate adopted by any plan open to new members is 5.25% (Kentucky State Police and Kentucky Employees Non-Hazardous). The highest rate currently used for a municipal plan is 7.75% (Chicago Transit Authority) and for a state plan is 7.5% (used by seven different plans).

As the figure above shows, states and pension boards have been slow to reduce their investment assumptions.

It took retirement systems more than a decade to move away from unrealistic 8% investment return assumptions. Fortunately, it is taking less time to also move past a similarly optimistic 7.5% assumed rate of return. The new target for public plans to leave behind is a 7% assumed return, which is currently the median assumption.

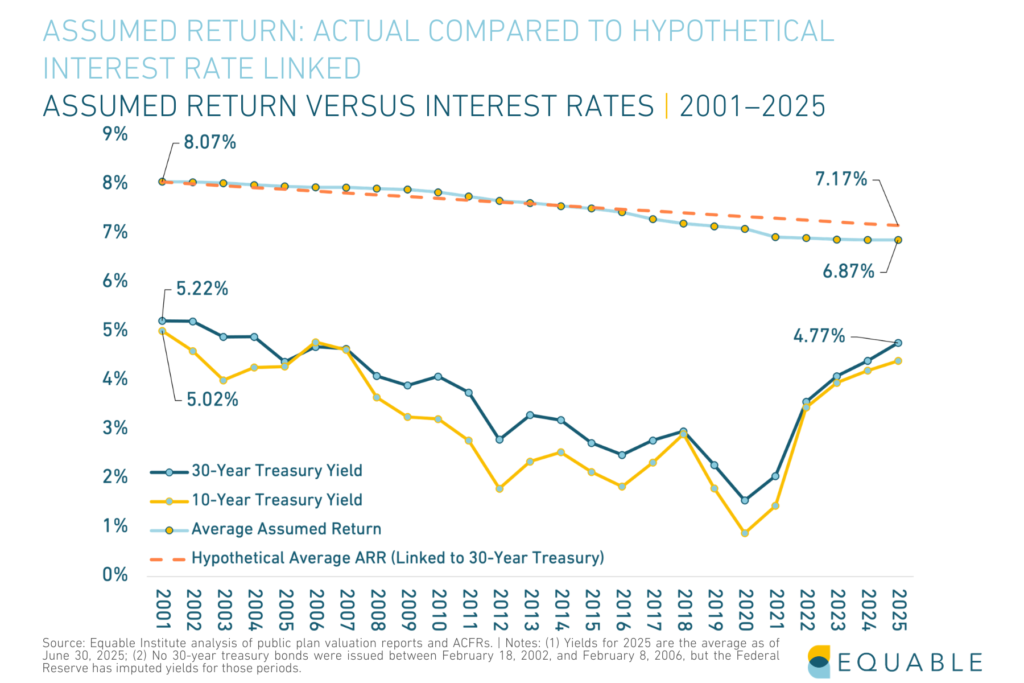

Assumed Rate of Return Versus Interest Rates

The chart below shows the average assumed return since 2001 (light blue line) and the historic change in interest rates, as represented by the 10-year and 30-year Treasury yield (yellow and dark blue lines).

The difference between interest rates and the assumed rate of return reflects how much pension funds think they can get by taking risks with their investments beyond just buying perfectly safe U.S. Treasury bonds.

While the gap between interest rates and assumed rates of return has tightened in recent years, the current spread reflects an ongoing risk that pension funds accept.

Now that Treasury bonds have almost returned to the levels they were in the early 2000s, the current average assumed rate of return of 6.9% is actually lower than the 7.2% (see the dashed orange line) that would have maintained the same risk difference they held back then.

This is a good outcome, but isn’t completely indicative of smart management on the part of pension boards, as for the years between 2001 and 2020, Treasury bonds had considerably lower returns than present day. In those years, pension boards kept their assumptions high despite the declining bond yields, because they were taking on more risk with their investments in order to keep their costs down.